Summary of My Post-CPI Tweets (May 2019)

Below is a summary of my post-CPI tweets. You can (and should!) follow me @inflation_guy. Or, sign up for email updates to my occasional articles here. Investors with interests in this area be sure to stop by Enduring Investments or Enduring Intellectual Properties. Plus…buy my book about money and inflation. The title of the book is What’s Wrong with Money? The Biggest Bubble of All; order from Amazon here.

- Happy(?) tariff day! With new tariffs imposed overnight, important to remember that the IMPORTANT effect on prices is not the near-term bump (which is small), but the fact that the disinflation of last 25y was possible because of trade liberalization.

- Also of course happy CPI day. We get the number in a few minutes. Here are a few pre-thoughts.

- Last month, core CPI was +0.148% m/m and 2.042% y/y, which both rounded down and looked like big misses.

- They weren’t really big misses, and at least some of that was due to a plunge in Apparel prices that was probably methodology-related (at least, that’s what the econs had anticipated so let’s take as an initial guess that they were right).

- Rents, the biggest and most important (and slow-moving) piece, were firm – firmer than I’ve been expecting in fact.

- But used cars was weak, along with Doctor’s services…along with Apparel, in general there was a lot of “left-tail stuff.”

- The left-tail nature of last month’s figure was illustrated by the fact that MEDIAN, the measure I focus on, was +0.27% to 2.85% y/y…another post-crisis high.

- Today, the consensus is for 0.2%/2.1% on core inflation. We would have to get something below 0.12% m/m to keep core from bumping to 2.1%, and any kind of firm number (>0.21%) could pop us back to a rounded 2.2%.

- That’s because last April was pretty weak. In fact four of the next 5 months were under 0.2% a year ago, so the comps will be easier for core.

- Core CPI +0.14%, slightly weaker than expected but rounding down to 0.1% again. Y/Y was 2.07%, so it did round up.

- Soft-looking but as noted earlier, base effects made it hard to maintain a 2.0% on core.

- Last 12 m/m core cpis.

- OK, the number is stronger than it looks. Used Cars very weak, -1.31% m/m which is crazy. Doesn’t look anything like the private surveys. Apparel -0.76% m/m again, -2.9% y/y. That’s not an accurate depiction of what’s happening.

- Because mainly of those two pieces, core goods went to -0.2% from flat. With tariffs rising, that doesn’t pass the sniff test. Core services, though, rose to 2.8% y/y. Primary rents were +0.45% m/m, 3.76% y/y, and OER +0.33%.

- Rent of primary residence. This is surprising, but important.

- Here is OER. With the Shiller index softening, many had expected rents to follow. But chippy wages are helping to keep a bid here, for now at least.

- There’s a real problem using home price indicators to forecast rents, because your model for that was built over a qtr-century in which wages & inflation were low and stable. If wages rise, then maybe home prices will lag rents – but we don’t know because we haven’t seen it.

- OK on to other things. Medical Care rose to 1.92% y/y vs 1.72% last mo. Every month it’s something different m/m tho. It was Pharma. Then Doctors’ Services last month. This month Dr Svcs bounced a little but Hospital Svcs -0.46% m/m. And Hosp Svcs is lgst part of Med Care.

- Core ex-housing was unchanged at 1.1% y/y. That’s actually surprising considering the drag from apparel and used cars.

- I may have been wrong on Used Cars being very surprising though. Guess there must be some uncaptured seasonal issue because y/y actually rose (meaning last April was also awful). And this is right on model. So I retract my concern about Used Cars.

- Biggest category drops on the month: Men’s and Boy’s Apparel (again), Footwear, Processed Fruits and Veggies, and Used Cars and Trucks. Biggest rises: Motor Fuel, Lodging Away from Home, Jewelry and Watches, and Medical Care Commodities (pharma)

- I skipped ahead to look at my guess for Median. It’s going to be a solid 0.2%, although that will cause the y/y to drop to “only” 2.80%. At least, that’s my estimate…won’t be reported for hours.

- College Tuition and Fees at 3.86% y/y compared with 3.84% y/y.

- Health Insurance doing its health insurance thing again.

- I mean, on housing it’s not ALARMING how fast it’s growing. It isn’t way above our model or anything. It just looks bad compared to what people were expecting given the S&P Corelogic Case/Shiller index.

- In green is the case/shiller y/y. So you can see people why were expecting a slowdown in rents. But you can also see that…it’s not a very good fit.

- That’s not quite fair b/c there’s no lag incorporated…home prices lead rents by ~21 months, so really we shouldn’t even see that impact for a while. Here it is lagged. Still not a good fit though and at times (2011, 2014) the direction of shiller didn’t match even lagged.

- Just a quick market comment…here’s the median CPI vs 10y inflation swaps. It’s going to be very hard to get much more bearish on long-term inflation swaps unless we see SOME signs that inflation is ebbing. So far, no signs at all.

- Four pieces. First Food & energy:

- Next, core goods. Our model has this headed higher, although not huge – maybe 0.5% or 1.0%. Recent deceleration is unsustainable especially in a fractious-trade world.

- Core Services less Rent of Shelter. No real change this month. If this is going to go up, it is going to be because medical care rises. To this end, it’s interesting that the previous spikes in Health Care Insurance (shown earlier) preceded spikes in other Medical Care.

- I wonder if the fact that Insurance is a residual means that when it is spiking, it means we’re just capturing prices in the wrong place until the survey catches up. Worth investigation.

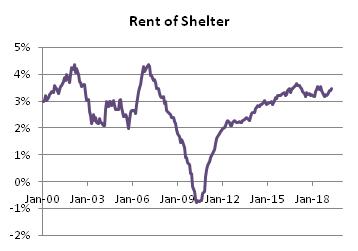

- Finally, Rent of Shelter. Clearly no disinflation here, yet.

- I think that’s good for today. Don’t forget to stop by my blog (http://mikeashton.wordpress.com ), though I must admit I’ve been slack recently in writing – but that’s because business is very exciting right now. A little tariff, a little MMT talk, and the phone rings.

The upshot of all of this is that core CPI continues to give a bad read on where inflation has been. Core tells us that inflation is ebbing. But the median category in fact has been steadily rising for several years. That doesn’t mean the inflation dynamic won’t roll over, but merely that so far it has not. The Fed’s concern that inflation isn’t getting to its target is misplaced, although ironically if they are able to restrain interest rates then the velocity dynamic means inflation is probably not far from peaking. But I don’t think we know that yet.