Summary of My Post-CPI Tweets (August 2017)

Below is a summary of my post-CPI tweets. You can (and should!) follow me @inflation_guy or sign up for email updates to my occasional articles here. Investors with interests in this area be sure to stop by Enduring Investments. Plus…buy my book about money and inflation. The title of the book is What’s Wrong with Money? The Biggest Bubble of All; order from Amazon here.

- about 15 mins to CPI. Consensus on core is 0.15% or 0.16% m/m, which would see y/y rise to ~1.74% vs 1.71%.

- Few see upside risks to that forecast. Indeed, most pundits are braced for a lower print. 0.15% on core would have beaten last 4 mo.

- Last 4 core CPI: -0.12%, 0.07%, 0.06%, 0.12%. But the 4 before that were 0.18%, 0.22%, 0.31%, and 0.21% so it’s a fair bet.

- Though the NKor situation dominates market concerns, today’s CPI garnering more than normal interest. Potential for some volatility.

- We’ve heard dovish Fed govs floating idea of pausing rate hikes (though continuing balance sheet reduction). That’s what doves do, but…

- …but another weak CPI will be seen as “sealing the deal” for removing rate hikes from the calendar.

- STRONG core CPI print is a much bigger surprise to most. Might be less mkt risk though – want to sell Tsys with NKor situation hot?

- Core CPI 0.11%, y/y: 1.70%. Actually slightly down v 1.71% last mo. Think we can take rate hikes off table but will look @ breakdn.

- Core goods steady at -0.6%, no dollar effect pushing it higher yet. Core services 2.4%, lowest in 2yrs.

- Just quick glance I see new cars -1.1% y/y down from -0.3%. If this is autos I’d not be as worried.

- Core ex-Shelter rose slightly, actually, to 0.63% from 0.60% y/y. But that’s obviously not alarming.

- Dropping the full data set at the moment. Please hold.

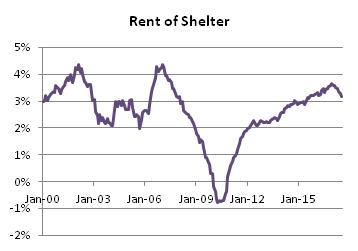

- In Housing, Primary Rents decelerated to 3.81% from 3.86%. OER slipped to 3.21% vs 3.23%. Small moved but big categories.

- Lodging Away from Home -2.36% vs -0.07%. Big move, small category. But that category often has big moves.

- Apparel went to -0.44% vs -0.67%. Again, not really seeing the dollar effect – apparel is one of the first places it would show up.

- New cars -0.63% vs 0.01%, weight of 3.68% of CPI. Not only the lowest in 8 years but…recession leader? See chart.

- Used cars -4.08% vs -4.30%, so the effect is in new.

- That new cars decel is worth 3bps on core, so if was still at 0.01% we’d have had core right at expectations even w/ shelter slowdn.

- Medical Care 2.58% vs 2.66% y/y. Pharma rose (3.84% vs 3.31%) but Prof Svcs dropped to 0.21% vs 0.58%

- Medical – Professional Services starting to look like Telecommunications. What’s the one-off here?

- Again with rents…decelerating but right about back on schedule.

- For those playing at home: wireless telephone services -13.25% vs -13.19%. After the huge drop a few months ago, not much add’l.

- Incidentally, Land Line Phone Services is 0.73% weight in CPI while Wireless is 1.74%. Gone is the ubiquitous creamcicle on the wall.

- A little hard to guess at Median b/c median category looks like Midwest Urban OER, which gets a 2nd seasonal adj, but my est is 0.18%.

- Here’s the inflation story over the last year, in two important chunks.

- US #Inflation mkt pricing: 2017 1.3%;2018 1.8%;then 2.1%, 2.1%, 2.1%, 2.2%, 2.1%, 2.1%, 2.3%, 2.4%, & 2027:2.4%.

- Here’s a little teaser from our quarterly. These are not forecasts, but entirely derived from mkt data.

- Inflation in four pieces: Food & Energy

- Piece 2: Core Goods, nothing to see here.

- Core Services Less RoS – this is the core CPI story.

- …though don’t forget piece 4. As noted earlier, this is just going back to model but some will forecast collapse.

- This might be the bigger story – declining core CPI is all about the weight in the left tail, which is why median is still at 2.2%.

- Despite core CPI slowdown, 44% of components are still inflating faster than 3%.

- …this makes it more likely the recent CPI slowdown reverses, b/c it’s being caused by left-tail outcomes that probly mean-revert.

Coming into today the market thought the probability of a December rate hike was only 38%, which seemed very low to me. But there is nothing here that suggests the doves are going to lose the fight to slow down the already-timid pace of rate hikes. It isn’t surprising to see markets rally on this data.

However, it is also easy to get carried away with the story that inflation is decelerating. Those left-tail categories are what is driving core inflation lower (and it’s the reason I focus on median CPI, because it ignores the outliers). Shelter has come off the boil a bit, and if that rolled over I would be more concerned about seeing much lower CPI. But there is no sign of that happening, and it seems unlikely to given that home prices themselves continue to rise at a better-than-5% clip (see chart, source Bloomberg).

So, if shelter isn’t going to continue to decelerate much more, then the risk going forward is mean-reversion of those left-tail categories. I don’t think Physician Services are going to go into deflation. (To be sure, some of that is probably a measurement issue as the mode of hiring and paying for doctors is changing, and it is hard to predict mean reversion from measurement issues). Thus, if the market starts to price a near-zero chance of higher rates come December, I’d be interested in buying that option on the chance that one or two of these next four CPI prints (the December CPI report is out the day of the December FOMC meeting) is tilted the other way.