Summary of My Post-CPI Tweets (July 2019)

Below is a summary of my post-CPI tweets. You can (and should!) follow me @inflation_guy. Or, sign up for email updates to my occasional articles here. Investors with interests in this area be sure to stop by Enduring Investments or Enduring Intellectual Properties. Plus…buy my book about money and inflation. The title of the book is What’s Wrong with Money? The Biggest Bubble of All; order from Amazon here.

- Big, big CPI day today. After four straight 0.1s (rounded down to that, in each case) on core CPI, the importance here is hard to overstate.

- With the Fed gearing up to ease, partly because of low inflation, these prints all matter more.

- (…although the Fed minutes suggested the Fed is taking a “risk management” approach, which makes the hurdle for NOT easing a lot higher since they can always say they’re addressing future risks, not current data.)

- The problem is that better measures of inflation, like Median or Trimmed Mean, are not really showing the same slowdown as core. That is, these are still one-offs, or “transitory” in Fed-speak.

- But that’s one way that inflation involves – as one-offs that become more frequent until those one-offs are the median. Still, while I expect inflation to peak later this year I don’t think that’s happening yet.

- There is an underlying mystery in all of this and that is: where is the tariff effect?! The markets have moved on from worrying about it because it hasn’t shown up yet.

- But the short-term bump from the actual tariffs was never the real threat with de-globalization. The important effects are long-term, not short term. Still, it makes investors more confident that China tariffs don’t really matter much.

- OK, just a few minutes until the number. After the number and my reactions to it, tune in to @TDANetwork where I will be talking with @OJRenick at about 9:15ET. The consensus is for 0.2% on core CPI, keeping y/y at 2.0%. Good luck out there.

- Well, that’s more like it. Core CPI +0.29%, pushing y/y from 2.00 to 2.13%.

- Breakdown in a moment but first thing it’s really important to remember: this does not mean the Fed won’t ease this month. Almost surely, they still will. Remember, this is “risk management” to them. They’ve set it up to ease anyway.

- Last 12 core CPI.

- OK, big m/m jump in Primary Rents and Owners’ Equivalent are the obvious culprits. Rents went to 3.87% y/y from 3.73% y/y on a +0.424% m/m jump. OER rose from 3.34% y/y to 3.41% y/y.

- Used Cars and Trucks also finally caught up a bit…they’d been way below where private surveys had them, but this month +1.59% m/m, vs -1.37% last month. y/y goes from +0.28% to 1.25%.

- Apparel +1.13% m/m. Y/y it’s still in deflation at -1.3%, but last month that was -3.1%. Tariff effect or just the new method adjustment starting to smooth out? I expect the new method will show more volatility, FWIW.

- You can see the main trend in apparel hasn’t really changed; this month’s bump just moves it back towards the prior flat-to-slightly-down trend.

- CPI-Used cars and trucks vs Blackbook. Had been a bit below, now spot on.

- Core ex-shelter rises to 1.16% from 1.04%. That’s still well below the highs from late last year but underscores that this is not JUST housing (although…housing is a big part of it).

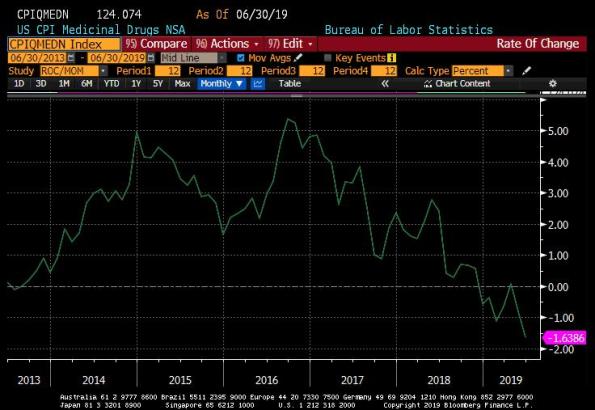

- This is interesting. Hospital Services (part of Medical Care) continues to plunge. -0.1% m/m and down to +0.50% y/y.

- also medicinal drugs continues to decline. And Doctor’s services was stable. But Medical Care as a whole drooped to 1.96% from 2.08% y/y. Those are the three big pieces, but…

- …Medical Care CPI didn’t decline further because Dental Services (0.79% weight, about half of doctors’ services) had a big jump, y/y to 1.94% from 1.15%. Get those teeth taken care of, people.

- College tuition and fees ebbed to 3.45% from 3.81% y/y.

- Back to Transportation…while Used Cars jumped (mostly just getting back to trend), New vehicles continued to droop. 0.58% y/y from 0.90% y/y. And leased cars got cheaper.

- My early estimate of Median CPI is +0.27%, bringing y/y back up slightly to 2.81%. Note the monthly series is much more stable than core, which is one reason to like Median.

- The largest negative changes this month were in Motor Fuel, Fuel Oil, Miscellaneous Personal Goods, Infants’ and Toddlers’ Apparel, and Public Transportation. All -10% or more on an annualized basis, but mostly small too.

- Largest increases were Jewelry and Watches, Car and Truck Rental (both of those over 60% annualized), Footwear, Used Cars and Trucks, and Men’s and Boys’ Apparel.

- I think that’s enough for today as I have to go get on air for @TDANetwork in 15 minutes. Tune in! Bottom line here is: keep focusing on Median, inflation isn’t headed down YET, but…Fed is still going to ease this month.

- Totally forgot to do the four-pieces charts. Will have to skip this month.

- OK, the four-pieces charts – I’ll have them in my tweet summary so might as well post them here. As a reminder these are four pieces that add up to CPI, each 1/5 to 1/3 of the total.

- First up, Food and Energy.

- Core goods. Now, this is interesting because it shows the reversal of some of the ‘transitory’ effects. Our model has this going to 1%, but recent outturns had been discouraging. Now back on track.

- Core services, though, continues to be drippy. A lot of the sogginess is medical care. I wonder what happens if the Administration wins and Obamacare is repealed? Short term, probably higher, but in the long-term less government involvement is also less inflationary.

- Finally, rent of shelter. Running a bit hotter than I expected it to be, and due to start fading a little. But no sign of a sharp deceleration in core while this is stable.

(I had to end this earlier this month because of the TD Ameritrade Network appearance, but went back and added the four-pieces charts later.)

The bottom line here is that nothing has changed in terms of what we should expect from central banks. They’re willing to let inflation run hot anyway because they thing low inflation was the problem. So they will ease this month, and probably will continue to ease as growth wanes. They will feel like they are ahead of the curve, and when inflation ebbs as I expect it to, they will say “see? We were right and we were even pre-emptive!”

Indeed, this is really the biggest risk in the longer-term. The Fed is going to be “right” but for all the wrong reasons. Inflation is not going to be declining because growth is slowing; these are merely coincident at the moment. Lower interest rates causing lower money velocity (since the opportunity cost of holding cash is going to go back towards zero) is the cause of the coming ebb in inflation which, by the way, won’t be as severe as in the last recession. But the risk is that the Fed becomes more confident in their models because they “worked,” and rely on them later.

Here’s an analogy. I just tossed a coin and the Fed went off, and ran complicated models factoring in gravity, wind resistance, the magnetism of the metals in the coin, biometric analyses about the strength of my thumb, and they concluded and called “heads.” It turned out to be heads, and the Fed is very happy about how well their models worked. Now, I know that it was “heads” because I tossed a two-headed coin.

So later, when I toss the coin again, the Fed runs the same model and calls “tails.” But this time, they are much more confident in their call, because of the model’s past success. Of course, since they didn’t actually get the right answer for the right reason the first time, there’s no more chance of being right than there was before…they’re just going to rely on it much more. And that’s the risk here. When the next inflation upturn happens, which I think will happen in the next cycle, the Fed will be very confident that their ‘expectations-augmented Phillips curve’ and Keynesian models will work…and they’ll be very, very late when inflation goes up.

But a really important point is: that’s not today’s trade. I doubt it’s even this year’s trade, although if I’m wrong and the peak isn’t happening yet it may be. The market realities remain:

- The Fed is going to ease this month, almost certainly 25bps.

- The Fed and other central banks are likely to keep easing preemptively, and then keep easing when the recession begins, and keep policy rates too low once the next expansion starts (although market rates will signal when that’s happening).

- Equities are too high for this growth regime; TIPS are way, way too cheap for any reasonably likely inflation regime…at least, relative to nominal bonds. But equities will probably take a while to figure that out.