Archive

My Views on Kevin Warsh as Fed Chairman

I promised last week that I would give you my views about Kevin Warsh. I did so while clearly forgetting that I already have. Having heard more from him, though, I can put more meat on that bone.

I must first tell you that I have a natural tendency to want to believe that our monetary policy institutions can be saved, and so I want to believe that each new Chairperson has a chance. I was optimistic, for example, about Powell (and to be fair he was a definite improvement over Bernanke and Yellen!) even though in the end he turned out to be a fairly normal Fed Chair. I do give him credit for responding to the COVID spike a lot faster and further than I thought he would, especially since he claimed to believe the inflation was transitory. He didn’t do it right, but at least he wanted to.

My hopes, though, have generally proved to be unrequited. In my opinion, the Fed has been in a downward spiral since 1987 when Alan Greenspan took over. I once wrote a book called Maestro, My Ass! and I do not apologize for it. Although we look wistfully on the Greenspan days now, he started several trends in central banking that have been very destructive – the main one being his mission to make the institution’s deliberations and thought process very transparent. But at least he viewed inflation as the primary policy target.

This introduction is meant to point out that while I really want to believe that monetary policymakers eventually learn lessons and course-correct to doing things the right way, I’m no apologist for the Fed. You’ll want to remember this when my enthusiasm for Kevin Warsh comes out, below. Here is my framework – my basic views, expressed ad nauseum on this blog over the years, about central banking and the conduct of monetary policy:

- Monetary policy is best conducted with as little transparency as possible. It is not the Fed’s job to make the water always warm and inviting for investors so that they can lever up their returns without fear. Transparency breeds complacency and causes excess leverage in markets. As I said in ‘Maestro’: make people dig their own foxholes, and they will dig them deep enough.

- The Fed has a truly terrible forecasting record when it comes to inflation, especially. I do have to say that there are some signs of improvement on that score, so maybe the reason it has been so bad for so long is that for 25 years there was nothing to forecast since inflation was fairly low and fairly stable; now that it’s worth researching, maybe they’re learning. Some. But the fact remains that the forecasts are not even remotely good enough to base monetary policy on.

- Because economic data has huge error bars, and gets revised a lot, and forecasts have even larger error bars, it is nearly impossible to reject the null hypothesis that ‘nothing has changed’ with any given data point. It takes a long time and a lot of data to truly overcome the confidence hurdle. Since monetary policy is such an overpowering tool, it generally should be used very sparingly. The Fed should only rarely move rates away from neutral, and only when the cause to do so is undeniable. Yes, this means they will be late. But that’s okay – see point #1 – if people know that they can’t rely on the central bank to save them.

- One of the wisest things Greenspan ever said was that with respect to the dual mandate of price stability and long-term economic growth, the condition of “low and stable inflation” is the environment most apt to produce high long-term economic growth. In other words, the inflation-fighting mandate is primary, and the economic growth goal is secondary – and best achieved by means of achieving the first goal.

- Interest rates have no identifiable causal (lead) effect on inflation.

- Inflation expectations are a result of, not the cause of, inflation.

- The stock of money per unit of GDP is pretty much the only thing that matters for the price level in the long term. (Here is an article with a few of my favorite charts.)

- The implication of 4, 5, 6, and 7 is that the Fed should focus almost exclusively on maintaining money growth at a low, steady pace. This job is hard enough with the proliferation of alternate forms of money!

Now, let’s compare this to what Hopefully-Future-Chairman Warsh said in his confirmation testimony last week.

- Inflation is primary: “Congress tasked the Fed with the mission to ensure price stability, without excuse or equivocation, argument or anguish. Inflation is a choice, and the Fed must take responsibility for it.”

- The Fed should reduce forward guidance. I personally would say eliminate. I’m not entirely clear if Warsh’s desire to reduce forward guidance is because he doesn’t believe the Fed is good enough at forecasting to provide good guidance, because he thinks that too much transparency leads to overleveraged personal, corporate, and financial balance sheets, or because he doesn’t think that the Fed gains anything by trying to restrain inflation expectations. It doesn’t really matter. All three reasons are good. Any one of them is sufficient. If Warsh wants to reduce forward guidance, he’s on the right track.

- He thinks the FOMC should meet less frequently! I love that – again, I’m not sure if his instinct to do it is because he doesn’t think the Fed should be so active, or because he doesn’t think the data changes enough in a month and a half between meetings, or because he wants to be less transparent. Again, all three reasons are good.

- Warsh seems to be a believer in the notion that the rise of AI will pressure inflation downward. I do not share this view (see my article here and by podcast here), although I am a wild fan about Claude. I may be wrong. Warsh may be wrong. The important point here is that Warsh seems willing to wait for evidence, rather than conducting policy as if the Fed’s models about what could happen was in fact evidence. This is wisdom. I am absolutely content to be optimistic about the effect of AI right along with Warsh… as long as we don’t adjust policy on the basis of a guess.

- In general, Warsh seems to believe that the Fed should be less-active with respect to interest rates; he has also expressed an opinion that the Fed’s balance sheet should be smaller and is a general skeptic about relying on the balance sheet to adjust monetary policy. Unlike many at the Fed, he thinks the size of the balance sheet is related to the level of inflation and interest rates. He is absolutely correct about this and it may be fair to say that this is one of monetarists’ core objections to how monetary policy has been conducted since Bernanke. Warsh dissented on QE and LSAP (large-scale asset purchases) back during the Bernanke days. Shrink the balance sheet, and that will let you lower interest rates a little bit as inflation recedes. Absolutely. When the Fed shrinks its balance sheet – which was first expanded in an effort to stave off deflation; remember Bernanke’s helicopters? – it will reduce upward pressure on money growth and that will directly slacken upward pressure on inflation.

I don’t know if Warsh can pull off such a monumental pivot. Institutions resist change, and the Federal Reserve is a big institution. But it is a pivot worth making! If Warsh succeeds (and if I’ve correctly laid out his views), it will restore the Fed to at least its mid-1980s glory. Well, maybe “glory” is a bit strong…but this is one case in which going backwards would be a drastic improvement.

The USDi Return for May is Not an Estimate!

This is just a brief note to clarify something about the construction of USDi, about which I’ve gotten a number of calls. Before I do, let me also tell you to be on the lookout for my blog next week, when I’ll tell you what I think about Probable-Next-Fed-Chairman Kevin Warsh. (In the behavioral economics world we call that a ‘precommitment’ strategy that has the effect of forcing me into doing it. It’s overdue anyway.)

In May, the USDi token (freely mintable at https://usdicoin.com/coin/ ) will return 12.59% annualized. That’s not an estimate, and it isn’t a typo. As I type this, USDi is in the midst of a month wherein its price is increasing at a 5.65% annualized pace. Its current price at the moment when I am writing this is 1.034237. At the end of April, its price will be 1.035424. At the end of May, its price will be 1.046286. The movement from the end-of-April price to the end-of-May price is 1.049% for the month, which annualizes to 12.59%.

Note that I am not saying its price ‘may be’ or ‘will be approximately.’ While the price you see if you buy USDi on Uniswap or another liquidity pool may not be exactly that, those are precisely the prices you can buy or sell at on our website if you do it at exactly the end/beginning of the months in question. (To be fair, I’ll also note there is a small fee to mint or burn. These are listed on the minting page under the header ‘What are the transaction fees,’ and they range from a low of 0% if you mint over $5mm, to a high of 0.05% – but at least a dollar – if you mint less than $100,000. So, your return will more likely be 0.99% for the month, or 11.88% annualized. Still pretty good).

This is an important nuance. USDi is not a tokenized money market fund, or some other tokenized fund, where the buyer gets a small share of the fund’s performance. If it was, then USDi would be a security and you couldn’t buy it at all in the U.S. unless we filed a Form D and performed AML and KYC on you. That wouldn’t be a very useful crypto tool. So we made USDi an indexed currency, similar to the Unidad de Fomento in Chile, that depends only on the value of the Non-Seasonally-Adjusted CPI index, mechanically. It accretes just like a TIPS bond, except that it does it every block, not just every day. I walked through the particulars last year in How to Calculate USDi’s Current Value.

Now, a TIPS bond – even a short-dated TIPS bond – also experiences changes in price. So while the principal of the October 2026 TIPS, and every other TIPS, will accrete 1.049% for the month of May…those bonds will also experience price changes. In particular, it is extremely likely that they (at least the short-dated ones) will decline in price over the course of the month since each successive buyer will have the right to less and less of that sweet accretion. Either way, you don’t know what you’ll have in a month if you buy a TIPS bond. But USDi has no maturity date. It is not a bond whose price declines when interest rates rise. It is inflation-indexed cash, or (if you prefer) analogous to an inflation-linked CD where the bank is paying you 12.59% for the month, but which you can cash out at any time with no penalty.

This remarkable return – which is likely to remain pretty attractive in June if the inflation swaps market is right about where NSA CPI will print when we get that data next month – is due to the spike in gasoline prices last month, which passed through fairly directly to the CPI.

The next logical question is ‘where does that return come from?’ I am going to skip that answer for now because when I talk about the underlying investment dynamics people tend to get confused and think that the underlying investment dynamics determines how USDi behaves. It doesn’t. Furthermore, the answer to that question does involve a fund that is a privately-placed security and which (therefore) it’s awkward to discuss on a public forum.

But mainly, I don’t want to confuse you. USDi this month is earning 5.65% annualized, and it will earn 12.59% annualized next month. The first estimate concerns June, and an estimate based on the inflation swap market suggests USDi will earn around 9% annualized in June. When we get the CPI in a few weeks, that return will crystallize and we will know June’s return absolutely.

I repeated this point about five times because it seems to me people are being very cautious about buying USDi at the very time that people should be agog over the known future returns and grabbing it. I understand why a big hedge fund might not want to buy $50mm of USDi without ever having experimented before. It is more confusing to me why folks aren’t buying $5k or $10k to try it out and see how it works. Don’t get me wrong, the flows are positive. They’re just…very timid. So just in case the concern is that ‘maybe this return won’t really happen after all,’ I wanted to be clear (here comes #6) that May’s return is baked in the cake. Go get some cake.

Inflation Guy’s CPI Summary (March 2026)

Today we get the CPI data that will finally unleash Trump’s critics and cause them to criticize the war effort to rein in Iran. (Just kidding – obviously Trump’s critics need no excuses!) We see the direct effects of the war on consumer energy prices, which the consensus expects to produce a headline m/m, seasonally adjusted CPI figure of +0.96% (consensus on core is +0.28%). The range of estimates is 0.6% to 1.5%, which is sort of crazy…it is hard to imagine how you get a +0.6% out of this. (Most of us are around 0.9%-1.1% though.) A couple of notes before we look at the actual number.

First, note that at this time of year the seasonally-adjusted number is lower than the NSA number is. NSA, the Bloomberg consensus is for about +1.15%!

Second, it is important to remember that before the Iran war, we were still unwinding the data artifacts that resulted from the 1-month gap in the CPI produced by the government shutdown last fall. Next month’s core inflation numbers were already going to be a bit higher than trend because of the payback in rents at the 6-month point after the October gap. The war doesn’t make the unraveling any easier, though we were getting to the end of that process. Key point though is that we don’t yet have a read on where trend core or median CPI is settling.

Which brings us to the main point looking forward to today’s figure, and thinking about the effect the war is having. The impact on energy prices is pretty transparent, and while important it is also ‘transitory.’ Energy prices mean-revert, and eventually gasoline prices will either decline back to some semblance of where they were – or they will at least flatten out and no longer contribute plusses to the monthly figure. There is almost no trend component to energy, which is why policymakers want to look at core and median. So that is the real item of importance today, and for the next couple of months: we want to look at signs of pass-through beyond energy, not just into core commodities (higher energy prices pass through via things like shipping and packaging, for example, pretty quickly) but more importantly into supercore (core services ex rents). So next month, we may or may not see lower gasoline prices…but we will also see the rents payback (higher), pass-through into core commodities (higher), and possibly growing signs of an inflation uptick beyond that – not just from the war, but from any trend that was developing pre-war. I take administrative notice of the Atlanta Fed’s Wage Growth Tracker, which in February and March rose from 3.6% y/y to 3.9% y/y. There isn’t a war effect in that, and while this doesn’t exactly break the downtrend in nominal wages (see chart below, source Bloomberg)…it also wasn’t entirely unexpected that wage growth would be bottoming near here.

Finally one last pre-number observation: I want to reprise my chart from last month showing 5-year inflation swaps on the Continent compared to 5-year inflation swaps in the US. The US swaps curve is still not showing any effect at all from the war.

Now, as I said energy prices are mean-reverting so the forwards shouldn’t show a lot of impact…but it almost always does because no one ever treats inflation as unit root. That is, when spot inflation goes up the curve almost always shifts up a bit along its length because every swap on the curve starts with a 1-year swap. If energy mean reverts, the 1y, 1y forward should shift lower to reflect that…but it almost never does. This is unusual, and curious. And it sort of implies a strengthening dollar, since if global inflation is higher because of aftereffects from the war, then weaker currencies will end up owning more of that inflation than stronger currencies. That happens to fit my thesis of dollar strength, but it’s still weird.

And now for the number…

Headline CPI came in at +0.865% seasonally-adjusted m/m, raising the y/y to 3.3% from 2.4%. The year/year number will rise further over the next few months to approach 4% before hopefully receding some. The NSA number for headline (which matters for USDi accretion in May – get it while it’s hot!) was +1.049% m/m. Seasonally-adjusted Core CPI was very tame +0.196%.

Among the major categories, Apparel was +1% while Medical Care, Recreation, and Other goods and services were all negative m/m.

Now, core goods rose to +1.18% y/y. This is interesting, because one thing that pundits were saying that that there was ‘some evidence that the invalidation of Trump tariffs led to lower goods prices.’ Not really. Apparel as I said was +1%, and core goods rose y/y even with surprising softness in Used Cars (where surveys suggested an increase). Core Services also ticked up, which is very interesting given what we saw in rents.

Primary rents were +0.19% m/m, and by my calculation will be the median category (spoiler alert: my estimate of median CPI is +0.19%). Owners’ Equivalent Rent was +0.28% m/m. Both were higher than last month’s surprises but y/y is still sagging.

Airfares were up +2.67% m/m, which is one core service that actually has a lot of energy in it. We’ll see a further rise from Airfares going forward. But here is supercore, and as I said this is the part we want to watch closely. We knew energy would be higher, but it mean-reverts. Rents will jump higher next month to re-pay the October zero, but rents already look like they’re leveling off after a long decline. We need to watch core commodities for energy pass through over the next few months. But the key is Core Services less Rent of Shelter. It has a small hook higher over the last couple of months, which is consonant with the Median Wages chart I showed earlier.

Wages, potentially pushed higher a little bit because of the shrinking workforce due to ex-migration, feed into supercore and that’s the feedback loop that I think will end up keeping us in the mid-to-high 3%s for median over the medium term.

Core ex-shelter rose to 2.27% from 2.09%. That’s not a big thing, but it’s something to watch. Rents are now definitely holding down overall inflation slightly. Rents are tracking below my model right now, but within the error band. They may just be running ahead of my model by a few months. Or, the ex-migration may be weighing on rents at the same time it is helping wages. Certainly, that will be true in some areas seeing larger ex-migration effects.

There was a significant fall in Medicinal Drugs this month, -1.05% m/m. It brought the whole Medical Care subindex down on the month, even though Doctors’ Services (+0.67%) and Hospital Services (+0.41%) both rose.

I noted before that my expectation for Median CPI is +0.19% m/m, which is not alarming. But here is the list of core categories below and above a 10% annualized m/m change:

Below: Miscellaneous Personal Services (-14% annualized) and Medical Care Commodities (-11%, mostly the aforementioned pharmaceuticals).

Above: Women/Girls’ Apparel (+23%), Misc Personal Goods (+21%), Public Transportation (+20%), Car/Truck Rental (+16%), Motor Vehicle Maintenance and Repair (+16%), Jewelry and Watches (+12%), Tenants’ and Household Insurance (+11%), and Footwear (+11%).

You can see in that, and in what I’m about to show, what the Fed’s study (https://www.federalreserve.gov/econres/notes/feds-notes/is-the-inflation-process-in-advanced-economies-different-after-the-pandemic-20260330.html) recently suggested, and that is a distribution that is shifted to the right even though it has tails on both sides and a median which, thanks to soggy rents, is scootching (technical term) to the left a little.

Median y/y should be roughly 2.7% after today’s figure, which I think ought to be about the low. One reason is that with median wages now 1.2% above median inflation, the upward feedback loop will help support prices.

Two final charts. The first one is the distribution of y/y changes. The big middle finger is rents, and that dominates the median calculation. But if you remove the middle finger, you can see there is a very broad middle, from 2% to nearly 6%.

And the final chart, BOOM, is the Enduring Investments Inflation Diffusion Index, which measures the distribution in a single number. Overall, there isn’t a lot in today’s report that is immediately alarming. But this captures the subtle piece that is alarming, and that is the broadening of inflation pressures.

The underlying message is that as the October surprise is resolving, and the war volatility is passing through, we are seeing beneficial moves in rents (lower) and wages (higher) thanks mostly to the shrinking of the pool of available labor. But outside of rents, which flatters the data, there are upward pressures. They don’t look disturbing, because it isn’t one thing (“oh, Used Cars was higher this month and that did it”) but small accelerations in a lot of things. That’s what we need to be watching over the next few months, as energy prices revert. Longer-term pass-through dynamics will matter and will show at asynchronous intervals. But there’s also a signature here of a turn back higher in inflation.

What does it mean for policy? It doesn’t really matter right now because there’s no way that Powell, due to his animus with Trump, is going to lower rates in the near term absent a financial accident and there’s nothing in the raw numbers that will make the Fed reach for the ‘tightening’ button. It’s not a lovely setup for the summer, though. I actually still think the next move will be an ease, but right now it looks to me like short rates aren’t due to move far in either direction for a while.

Time to Choose Your Inflation Adventure with Velocity and Money

We have CPI coming up in a few days, but M2 came out recently and it is worth commenting about, so let me drop some thoughts about the state of money and velocity right now and the context we are operating in.

M2 grew 0.88% in February, causing the y/y change to rise to 4.88% (quarterly, however, it is 6.65% annualized). I saw somebody recently observe that money growth was about 6ish back before COVID, so this level is not very worrisome to that pundit. I think that’s wrong – not that this level is worrisome in the big picture, but the trend is bad and the current level is actually not consistent with low and stable inflation as it was prior to the late twenty-‘teens.

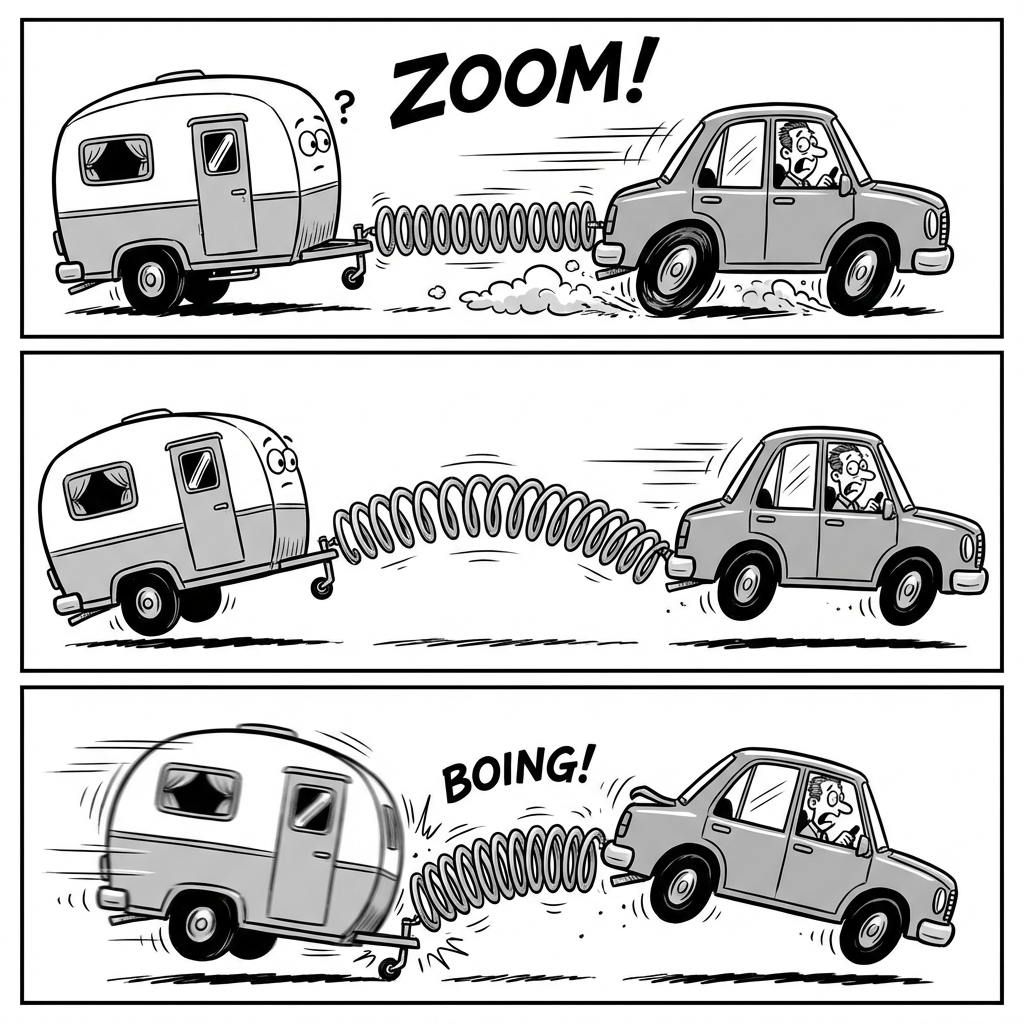

Before we get to that, let’s review the state of play for money velocity. Remember when velocity plunged early in COVID, and people said inflation wouldn’t happen because the transmission mechanism was broken? That comment was so funny it made me blow milk out of my nose, even though I wasn’t drinking milk. It was entirely an artifact of the different time frames over which the money supply was changing, compared to the time frames required for prices and output to change. MV=PQ, and M was changing suddenly. Since GDP can’t suddenly change 20%, money velocity became the capacitor that held the excess charge which slowly bled into prices. In my podcast, and occasionally in this blog, the image I shared was of a car rapidly accelerating away from a trailer hitched to it by a spring. At first, inertia keeps the trailer from traveling as fast as the car, and the spring stretches. Once the car stops accelerating, though, the spring compresses and the trailer catches up. The illustration below is courtesy of Lovart.ai.

So where are we? Here is the US monetary system over the 2019-2025 period showing total growth from December 2019. The x-axis shows the total percentage growth in money as a percentage of real output (M/Q). The y-axis shows the total change in the price level. Now, I have to point out that when I was talking about this, in 2021 or 2022, we were very far away from the diagonal line showing where the two changes are equal. And I said we would be going back to the line, and we went back to the line. People really ought to listen to me more.

The other way to look at this is that velocity is back almost to where it was prior to COVID.

So is there any problem here? Velocity is back to where it was, but if it’s stable and money is growing at 4.9% y/y, then P+Q grows at 4.9%, so 2% inflation with 3% growth…sounds pretty good.

This is where we review the “but 6% worked!” argument.

You can see from the chart that yes, since the late 1990s M2 grew at 5-10% and we never had much of an inflation problem. Why now? Well, during that period velocity was steadily declining – and that is the only way that you can sustain 6% money growth with 3% real economic growth and get 2% inflation. The question, then, was why velocity was declining. Remember, some people think this is a trend, because they don’t really understand what drives velocity. During that period, interest rates steadily declined. This was also a period of increasing globalization and a demographic dividend (more workers relative to the aged). Now, whether the interest rates declined because of those trends because both trends were disinflationary, or if interest rates declined because of a dovish Fed and they only got lucky because of those trends…I don’t know. But the point is that the largest driver of lower money velocity during that period was lower interest rates.

And interest rates are now approximately fair. Some people think they’re too low with inflation too hot, some people think they’re too high with economic growth seeming to slow, but let’s just say they’re not 300bps wrong at this point. Here is our velocity model. With lots of crazy volatility, it has velocity pretty close to on-target. Here’s the problem: the last time prior to COVID were as high as they are now (I’m looking at 5y Treasuries), it was also prior to the Global Financial Crisis and the regime of interest rate repression. Back in 2007, 5y rates were this high, and money velocity was about 2.0, some 40% higher than here. What is holding velocity down right now in our model is a very high level of economic policy uncertainty, which causes people to hold more cash than they otherwise would given the level of interest rates. Thanks to the war between the President and his allies on one side, and the minority party on the other side, not to mention the Iran war, there is a lot of uncertainty right now and that is causing people to conserve cash.

It won’t always be that way, but with M2 growing near 5%…it really needs to be that way. By the way, the money growth situation is a bit worse than it looks, too: there has in the last couple years been a fairly dramatic rise in the amount of non-M2 money that is growing in defi/crypto space. Bitcoin isn’t money, but stablecoins are very much like money. The scale of the Stablecoin money supply is small compared to the ‘off-chain’ money supply, but it is starting to get large enough to matter. Anyway, we know the sign of that growth, and it’s a big fat plus.

So no, 6% is not a stable rate of money growth going forward from here. This is not the early 2000s. It is not the 1990s. If we could manage to just have 6% growth, then we’re probably going to end up being in the mid-to-high-3s on inflation, and that’s tolerable. But if that’s the midpoint of money growth, then mid-to-high-3s is the midpoint on inflation with some periods a little below that and some periods a little above that.

Economies adapt, and an economy can work fine at 4-5% inflation or even higher as long as it is stable. But 4% inflation feels different than 2% inflation, and the economy will work differently in that sort of regime. Businesses will be more likely to pass through cost increases rather than absorb what they think are short-term variations (see “How Expecting Inflation Un-anchors Manufacturers’ Pricing Strategy”). Equilibrium equity prices are lower. Menu costs and search costs go up. And so on. We may already be seeing some of these long-term structural changes. The Fed just published a FEDS Notes entitled “Is the Inflation Process in Advanced Economies Different After the Pandemic?” The short answer? Yes it is. The question is, are we on track to get the inflation process back to the way it used to be? And the answer there appears at this juncture to be: no.