Archive

Time to Choose Your Inflation Adventure with Velocity and Money

We have CPI coming up in a few days, but M2 came out recently and it is worth commenting about, so let me drop some thoughts about the state of money and velocity right now and the context we are operating in.

M2 grew 0.88% in February, causing the y/y change to rise to 4.88% (quarterly, however, it is 6.65% annualized). I saw somebody recently observe that money growth was about 6ish back before COVID, so this level is not very worrisome to that pundit. I think that’s wrong – not that this level is worrisome in the big picture, but the trend is bad and the current level is actually not consistent with low and stable inflation as it was prior to the late twenty-‘teens.

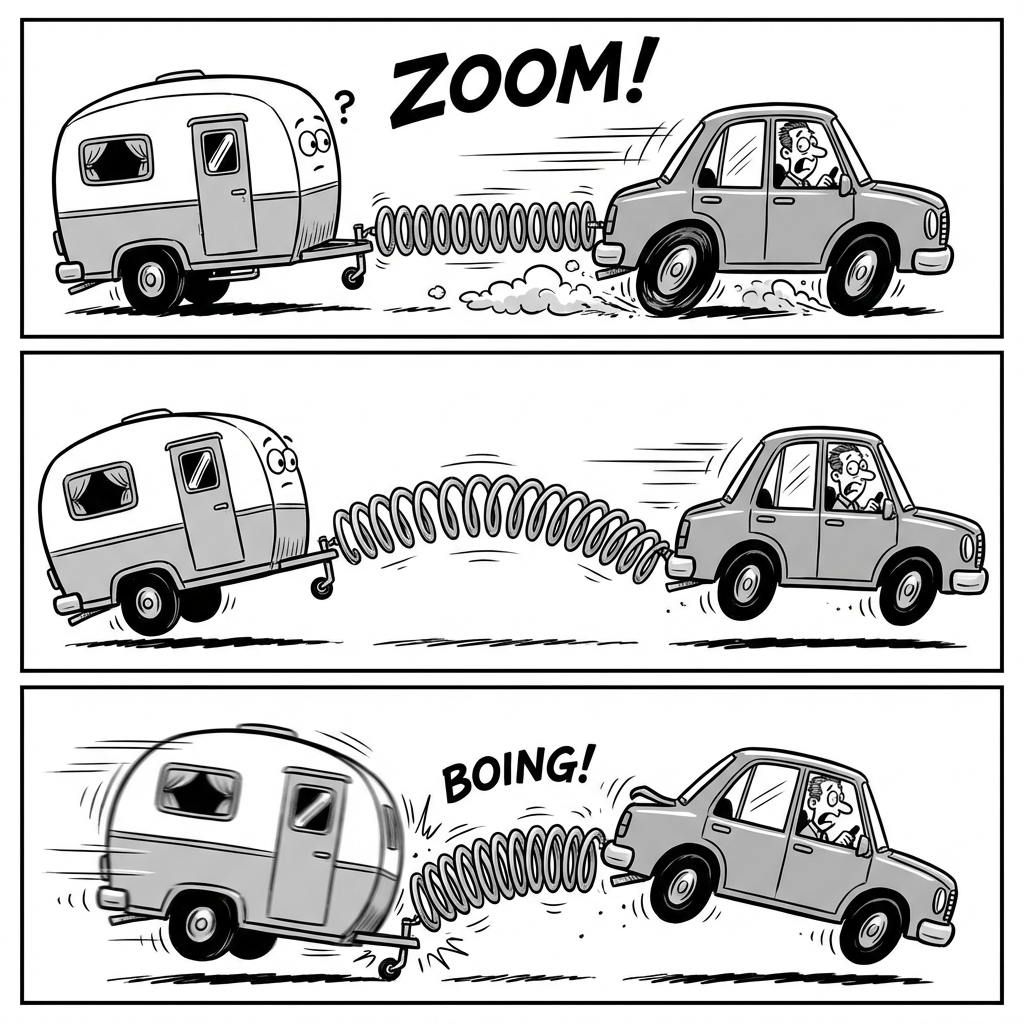

Before we get to that, let’s review the state of play for money velocity. Remember when velocity plunged early in COVID, and people said inflation wouldn’t happen because the transmission mechanism was broken? That comment was so funny it made me blow milk out of my nose, even though I wasn’t drinking milk. It was entirely an artifact of the different time frames over which the money supply was changing, compared to the time frames required for prices and output to change. MV=PQ, and M was changing suddenly. Since GDP can’t suddenly change 20%, money velocity became the capacitor that held the excess charge which slowly bled into prices. In my podcast, and occasionally in this blog, the image I shared was of a car rapidly accelerating away from a trailer hitched to it by a spring. At first, inertia keeps the trailer from traveling as fast as the car, and the spring stretches. Once the car stops accelerating, though, the spring compresses and the trailer catches up. The illustration below is courtesy of Lovart.ai.

So where are we? Here is the US monetary system over the 2019-2025 period showing total growth from December 2019. The x-axis shows the total percentage growth in money as a percentage of real output (M/Q). The y-axis shows the total change in the price level. Now, I have to point out that when I was talking about this, in 2021 or 2022, we were very far away from the diagonal line showing where the two changes are equal. And I said we would be going back to the line, and we went back to the line. People really ought to listen to me more.

The other way to look at this is that velocity is back almost to where it was prior to COVID.

So is there any problem here? Velocity is back to where it was, but if it’s stable and money is growing at 4.9% y/y, then P+Q grows at 4.9%, so 2% inflation with 3% growth…sounds pretty good.

This is where we review the “but 6% worked!” argument.

You can see from the chart that yes, since the late 1990s M2 grew at 5-10% and we never had much of an inflation problem. Why now? Well, during that period velocity was steadily declining – and that is the only way that you can sustain 6% money growth with 3% real economic growth and get 2% inflation. The question, then, was why velocity was declining. Remember, some people think this is a trend, because they don’t really understand what drives velocity. During that period, interest rates steadily declined. This was also a period of increasing globalization and a demographic dividend (more workers relative to the aged). Now, whether the interest rates declined because of those trends because both trends were disinflationary, or if interest rates declined because of a dovish Fed and they only got lucky because of those trends…I don’t know. But the point is that the largest driver of lower money velocity during that period was lower interest rates.

And interest rates are now approximately fair. Some people think they’re too low with inflation too hot, some people think they’re too high with economic growth seeming to slow, but let’s just say they’re not 300bps wrong at this point. Here is our velocity model. With lots of crazy volatility, it has velocity pretty close to on-target. Here’s the problem: the last time prior to COVID were as high as they are now (I’m looking at 5y Treasuries), it was also prior to the Global Financial Crisis and the regime of interest rate repression. Back in 2007, 5y rates were this high, and money velocity was about 2.0, some 40% higher than here. What is holding velocity down right now in our model is a very high level of economic policy uncertainty, which causes people to hold more cash than they otherwise would given the level of interest rates. Thanks to the war between the President and his allies on one side, and the minority party on the other side, not to mention the Iran war, there is a lot of uncertainty right now and that is causing people to conserve cash.

It won’t always be that way, but with M2 growing near 5%…it really needs to be that way. By the way, the money growth situation is a bit worse than it looks, too: there has in the last couple years been a fairly dramatic rise in the amount of non-M2 money that is growing in defi/crypto space. Bitcoin isn’t money, but stablecoins are very much like money. The scale of the Stablecoin money supply is small compared to the ‘off-chain’ money supply, but it is starting to get large enough to matter. Anyway, we know the sign of that growth, and it’s a big fat plus.

So no, 6% is not a stable rate of money growth going forward from here. This is not the early 2000s. It is not the 1990s. If we could manage to just have 6% growth, then we’re probably going to end up being in the mid-to-high-3s on inflation, and that’s tolerable. But if that’s the midpoint of money growth, then mid-to-high-3s is the midpoint on inflation with some periods a little below that and some periods a little above that.

Economies adapt, and an economy can work fine at 4-5% inflation or even higher as long as it is stable. But 4% inflation feels different than 2% inflation, and the economy will work differently in that sort of regime. Businesses will be more likely to pass through cost increases rather than absorb what they think are short-term variations (see “How Expecting Inflation Un-anchors Manufacturers’ Pricing Strategy”). Equilibrium equity prices are lower. Menu costs and search costs go up. And so on. We may already be seeing some of these long-term structural changes. The Fed just published a FEDS Notes entitled “Is the Inflation Process in Advanced Economies Different After the Pandemic?” The short answer? Yes it is. The question is, are we on track to get the inflation process back to the way it used to be? And the answer there appears at this juncture to be: no.

Bounce in Money Growth is Good News and Bad News

The monthly money supply numbers are out. I have bad news and good news.

The bad news is that the contraction in the money supply appears to be over. That’s not bad news per se (see below), but it’s bad in that the anti-inflationary work that was happening is coming to an end before it’s quite finished. Although I would be reluctant to annualize any one month’s change in M2, the $92bln increase in M2 in March was the largest increase since 2021. It only annualizes to 5.5%, so it isn’t exactly running away from us – but it’s positive. The 3-month and 6-month changes are also positive, and the highest since early 2022 in each case. Again, we’re only 0.72% above the ding-dong lows of last October, but the sign is now positive.

With the money supply figures now in, and with the advance Q1 GDP report due this week, we can revisit our chart of “how much more inflation ‘potential energy’ remains.” (see “Where Inflation Stands in the Cycle,” November 2023). As that article (and this chart) illustrates, if M2 doesn’t go down then this gets more difficult. M2 in Q1 rose at a 1.24% annualized rate over Q4. GDP is expected to rise 2.5% annualized. So M/Q…barely moves, as the chart shows.

We will eventually get back to the line, unless velocity is permanently impaired. Despite all of the crazy people who told you it was, there’s no evidence of that. M2 velocity will rise about 1% (not annualized), if the GDP forecasts are on point. That will be the smallest q/q change in several years, and velocity will be getting very close to the 2020Q1 dropping-off point. But there frankly is no reason for velocity to stop there; higher interest rates imply higher money velocity. However, we are getting close.

(Incidentally, if you’re curious how we can be almost back to the dropping-off point of velocity and yet still be 5% below the line in the first chart above, it’s because I’m using core inflation. With food and energy, we’re a little closer to the line and have used up more of the ‘potential energy.’ But food and energy are of course volatile and so while a good spike in energy prices would look like we’ve used up all of the potential energy, that could just be a one-off effect.)

Either way, we aren’t too far away from getting back to home base and that’s good news. Yes, prices by the time we are done will have risen 25% since the end of 2019, and that can’t really be characterized as a ‘win.’ Let’s go Brandon. But we are getting closer.

The good news about the new rise in M2 is that it’s timely. Markets and the economy were starting to show signs of money getting a little tight; losing a little lubrication in the machinery. An economy does need money to run, and while the only way we can get back to the old price level is to have money supply continue to decrease, that’s also a painful process. In the long run, we would have price stability if the change in M was approximately equal to the change in GDP. If we want 2% inflation, then we need M to grow about 2% faster than GDP. Vacillating velocity means that it isn’t purely mechanical like that – the steady decline in velocity since 1997 is the only reason that inflation stayed tame despite too-fast money growth over that period – but the long downtrend in velocity is likely finished since the long decline in rates is finished. Thus, if we get money supply growth back to the neighborhood of 4%, we can get our 2-2.5% growth with restrained inflation over time.

I am not super optimistic that all of that will work out so nice and cleanly like we draw it up on the chalkboard, but I am more optimistic about it than I was two years ago. We still have some sticky inflation ahead of us, but if the Fed keeps reducing its balance sheet then eventually we will get inflation below the sticky zone and back towards ‘target’ (even though there isn’t a target per se any more).

Rising Mortgage Origination Hints at M2 Turn

One of the successes the Federal Reserve can tout from the last couple of years (and the list of them is pretty short, to be fair) is that after the unprecedented policy actions during COVID caused never-before-seen rates of money supply expansion, subsequent policy avoided normalizing that explosion.

Year over year growth in M2 reached 26.9%. But in 2022, as the Fed started hiking rates and shrinking its balance sheet, the rate of growth slowed until M2 reached its absolute peak in July 2022 and began to slowly decline. As of today’s H6 release, year-over-year M2 has been negative for 13 months in a row.

To be sure, after a massive explosion the level of M2 has not declined all that far as the chart below shows. I also documented this fact back in November in “Where Inflation Stands in the Cycle,” which was really a good piece. You should read it.

So the success of the Fed here can be summarized by saying, ‘at least they didn’t keep blowing up the money supply.’ Since the rise in prices is clearly and closely related to the explosion in the quantity of money we have seen (anyone who still resists this obvious truism after the mountain of recent evidence is added to the prior mountain of evidence), this was a sine qua non for getting inflation back down. It isn’t sufficient, unless it’s continued for a very long time, but it’s necessary. As I illustrated in that article linked to above (which, really, you should read), there are several ways that inflation could evolve from here as the shock to the system gradually unwinds. I’ve talked before about how velocity in the policy crisis behaved as a spring or a capacitor, absorbing a lot of ‘monetary energy’ that is doomed to be released back into the system. Velocity is still rebounding (in Q4, if forecasts for Thursday’s Advance GDP report are accurate, it will rise something like 4% annualized), but if money growth remains negative then that’s really the least-painful way this can resolve. In the last chart from that prior article (have I mentioned it’s worth reading?), slack money growth with decent growth and rebounding velocity is reflected in a movement mostly to the left, with the price level not rising much. Good outcome.

However, that outcome is predicated on the notion that the money supply remains slack. If M2 starts to rise again, then the curve drifts upward and the potential set of outcomes almost certainly involve higher prices. Naturally, I’m mentioning this because of developments that make me concerned on this score.

One thing that I seriously missed in 2022 was the fact that the increase in interest rates helped bring down money supply growth. That’s not at all intuitive, because in general changing the price of a loan tends not to change the demand for a loan by very much – especially when higher inflation is making the spot real interest rate paid by the borrower lower and lower. In other words, I assert with some decent evidence that consumer and industrial loan demand is somewhat inelastic for modest changes in interest rates. Ergo, my belief was that merely raising interest rates would not necessarily cause money growth to decelerate. As it happened, I was saved from my own mistake by the fact that the Fed was also shrinking the balance sheet, which (despite the fact that reserve balances aren’t binding on banks in the current environment, so they are essentially unconstrained in lending) I thought might help money growth to decelerate. Not that I thought we’d keep getting 20% growth, but I didn’t think we would have naturally seen money growth fall below, say, 5%. Fortunately, because the Fed was also shrinking the balance sheet my forecasts were not drastically inaccurate despite being wrongly inspired, and so I forecast 5.1% median inflation for 2023 and we got 5.06%. It’s nice when the ball actually bounces your way.

As it happens, though, for the most part higher interest rates seem to have not affected loan growth very much. C&I loan growth remained strong throughout 2022 and didn’t start to level off until the Fed was just about through tightening, and consumer loans as I expected really only started to level off when the Unemployment Rate started to rise…credit cards, not at all. And that’s because, as I said, most borrowers are not borrowing because they made a NPV calculation that said borrowing makes sense; they’re borrowing because they need to and 1% or 2% or 3% doesn’t really change that calculus very much.

But you know where it did change the calculus a lot? In mortgages. And that’s because a buyer might be reluctant to pay 1% more on a mortgage, but what the buyer also needs is someone who is willing to abandon their awesome loan. As has been noted elsewhere by lots of people, home sales absolutely cratered not because people weren’t wanting to buy but because there weren’t enough people who wanted to sell. So mortgage origination volumes also dried up, as a direct consequence of higher rates. The one large market where interest rates did have a big impact, although not for the reason you’d think, was in mortgages!

You know I wouldn’t say this unless I had a neat chart to show you. Here is the Mortgage Bankers’ Association Purchase index, tracking the volume of new loans for purchasing a home (in black), set against y/y money supply growth, in blue.

Let’s tie this up with a bow:

- Higher rates didn’t affect every kind of loan, but had a big impact on turnover, and thus origination, in one very large loan market: mortgages.

- Lower mortgage origination turns out to have been uncannily correlated with money supply growth. This may or may not be causal, but it at least means that mortgage origination merits consideration as a leading indicator of money supply growth.

- As interest rates have leveled off and even declined some, the housing market is gradually adjusting. We are seeing higher home prices, and mortgage origination has been showing signs of recovering as the chart shows (mortgage origination numbers are released before sales numbers, so expect a rise in home sales coming).

- It is going to be difficult for the Fed to keep the money supply shrinking, if origination of new mortgages rises even a little bit. This doesn’t mean M2 is going to skyrocket, just that it is going to stop shrinking (in fact, it has risen each of the last two months).

- If M2 rises at even a sober 5% pace, combined with money velocity that still has some normalization left, it will be extremely difficult for the Fed to hit its inflation target on a sustainable basis for some time.

And what should you do about it, just in case? For starters, read “Inflation Sherpa.”

Transcript: “What the Money Velocity Comeback Means for Inflation, and Investors”

Episode #50 of the Inflation Guy Podcast was well-received. In particular, my analogy of the car-trailer-spring system to explain why velocity is doing what it is doing garnered some strong positive feedback. Several people suggested that I publish a transcript, for those people who would prefer to read it (or who don’t know I do a podcast). What follows is a somewhat-edited version of the podcast. I took out a lot of “um” and repeat words, and the usual sorts of things that you’re embarrassed to see when you read a transcript of what you said. I tightened it up a little bit in some places and added a clarifying word here and there in brackets. But for the most part, it’s true to the original.

If you have any questions, ping me. And subscribe to the podcast, follow me on Twitter @inflation_guy (or subscribe to the private Twitter feed), or hmu to talk about how we manage money at Enduring Investments for individuals and small institutions.

Hello and welcome to Cents and Sensibility, the Inflation Guy Podcast.

I am Michael Ashton, I’m the Inflation Guy, and I’m your host. And today we have Episode 50 of The Inflation Guy Podcast and I’m going to return to money velocity because we had data out today for the fourth quarter of 2022 and there was a significant move higher in money velocity. I’ll get to that in a bit and talk about the implications that we should take away – the practical implications for what this means.

But I want to talk about this because it’s sort of become de rigueur among certain bond bulls to point at the massive drop that we had in money velocity that coincided with the massive increase in M2 during the COVID-crisis response. And those bond bulls say that velocity is permanently impaired and so the velocity plunged and it’s never gonna come back. And so it successfully blunted the importance of the massive rise in money. But we don’t have to worry about about that ever coming back. We don’t have to worry about it from now on.

This is obviously crucial to the case for lower inflation because that case basically boils down to: money growth has rapidly decelerated – it’s been negative over the last…I think it’s negative over the last 12 months now. But for a while it’s been flat to negative and so “therefore inflation will fall.”

That’s only true, though, if the sharp fall that we had in velocity is not reflected in now having a sharp rise in velocity at the same time that the sharp rise in money is being mirrored by insufficient money growth or money supply decline.

So if money…that spike now comes back and velocity plunged but doesn’t come back, then that’s the case for why we had some inflation, but not as much as the money supply spike would suggest, and now we’re going to have disinflation (or some people even say deflation – hard to believe that though).

To believe that money velocity plunged and then isn’t gonna come back, you have to believe that velocity declined for a permanent reason. But it didn’t, and that’s the bottom line here: that’s not how velocity works.

[This podcast] Episode 10 was about money velocity…and Episode 30. [Periodically in] this podcast [I have] also talked about how money velocity had turned higher last summer; at the time it was just sort of a the beginning of a turn higher. But in this quarter, the quarter just completed – the fourth quarter of 2022 – the velocity of M2 rose at an 11.4% annualized rate (which means it went up 7.3% for the whole year).

That happened, naturally, because we had money supply down while we had fourth quarter growth – real growth “Q” – that was positive, and obviously an increase in prices as well. So your PQ side of things was quite positive for the fourth quarter and M declined. And since velocity is essentially a plug number, it means velocity had to go up a lot to balance the left side of that equation, the MV=PQ equation.

Essentially, what’s really happening with velocity and the reason that velocity sort of had to come back – obviously it’s a plug number, but here’s the bottom line story of why velocity plunged. It wasn’t any permanent impairment. You should think about it this way:

You have a rapid-moving variable in in the money supply which spiked all of a sudden and you have a slower-moving variable, which is prices (because it takes time for people to change prices and for that price change to be picked up in the survey measures at the BLS and so on). And so that’s sort of like you have an automobile attached to a trailer, but instead of having a sort of a fixed rig that is attached to the trailer, you have a spring. So as the car moves away…the car goes into gear and starts to pull away. It’s moving faster than the trailer and so the spring stretches and eventually the trailer starts to move and eventually comes along. And as long as the car doesn’t continue to accelerate forever, eventually that spring will compress again and the trailer will catch up.

In fact, actually that analogy is so apt in this case, I wonder if you can’t model the whole situation with a k constant, like you would with spring physics. Because the analogy is very good. Essentially what’s happening is that, you know, money supply went zooming away and prices came along, but they came along more slowly. And so now the car is sort of sort of decelerating and the trailer (prices) is catching up to the spring, which is money velocity is starting to go back the other direction.

It’s best to think about this…and I mentioned this in the other times that I’ve talked about velocity…it’s best to think about this as being caused by (if you have to think about in terms of a cause: obviously it’s mainly a quantitative thing that sort of has to happen because we have two variables that are moving in two different paces)…it’s best to sort of think about that as being caused by precautionary demand for cash. Which is kind of what happened, right?

So, during the crisis, the government dumped tons and tons of cash into everybody’s accounts and it wasn’t spent immediately. It took some time to spend it.

So why wasn’t it spent immediately? Well, part of it was people had to figure out what to spend it on, but part of it was it was a scary time and so people figured, “well, maybe I’ll hang on to this a little while or maybe I’ll use it to pay off some debts or whatever.” It took a while for it to actually be spent until people’s financial situation got stressed enough that they had to go dip into the money that they swore they were gonna save…or what have you.

That’s the way I have modeled this is as a precautionary demand or a demand [for liquid cash] based on fear and concern about things. But the real reason is that this happened so fast, the money was flushed so fast into the system that there just was no way that prices could really respond that quickly.

Now the bottom line here is that velocity is not permanently impaired. In fact, it should rise with interest rates, as interest rates go up. And that is in fact kind of what’s happening…although I think most of what we’re seeing is this decline in the precautionary demand, but some of it is that with higher interest rates, there are more opportunities to do something other than hold cash earning zero. There’s some opportunities to take that away from true cash balances and checking balances and stuff and put it into term deposits and stuff like that.

And that means that velocity is going to come back (and it is), and that means that prices will eventually have to catch up with the car, right? The trailer eventually has to catch up with the car.

Money supply has risen since the beginning of this crisis, something around 40%, which means that prices are going to have to go up something in that neighborhood.

Actually, if velocity was unchanged over the entire length of this period and money supply only went up 40%…if you want to know how much prices are gonna go up, you have to divide the increase in money supply (that’s 40%) by the increase in GDP, whatever that turns out to be. So if GDP is up 10% then we need to see prices up an aggregate of 30%-ish or so. And so that’s sort of where I think we’re eventually going to go.

So what’s the takeaway? What does that mean, and what should you do about it?

The important takeaway is that while we are past peak inflation for now, there’s no sign that we’re going to crash back to 2% anytime soon. If in fact money velocity had not initially plunged – if velocity had been flat through this whole period – then I would be looking at the [recent] decline in the money supply growth going down to zero, and even negative, and I would say, “look, inflation should be coming down hard here; it should be going negative.” The problem is that we still haven’t had the rise in prices that you would have expected from the initial rise in money. Where that shows up is [in] that velocity plunge and [it] hasn’t come all the way back over the long haul.

The level of prices, as I said, is closely related to the level of M2 over GDP. And that’s just a consequence of the algebra of MV=PQ. So since 1990 that…well, let’s just go back further.

If you go from like 1959 to 1991, about 32 years, that relationship was super tight. M2 over that time period roughly tripled: it was up 286%. Sorry, roughly quadrupled. I’m sorry: M two divided by GDP was up 286% And the GDP deflator was up 303%. So they both roughly quadrupled over that time frame. Since 1990, that tight relationship has been less tight, which has shown up as a lot of velocity volatility.

Now, this is not irrelevant, volatility. Some of it is because there’s a changing definition of money; M2 and M1 have kind of become blurred over time. Some of that volatility is an error in measuring nominal GDP. Some of it, and maybe most of it, is excessive Fed activism on interest rate management…you know, pushing interest rates for example artificially too low since the Global Financial Crisis, which artificially depressed money velocity and so on.

But the basic relationship over a long period of time is still there. There are people out there who sort of adjust money supply in certain ways to get a better fit and I’m just I’m just not super comfortable that I know exactly the right way to do that.

I’m looking at the big picture here and I know if M2 divided by GDP goes up a lot, then we should have prices go up a lot.

Anyway, the bottom line is that inflation is not going to crash back down. We still have a lot of potential energy in the system that is pushing prices higher. And that means that market expectations of inflation are too low right now. The inflation swaps market is pricing that by June we’ll have year-on-year inflation back to 2.16%, which would just be an amazing crash back down without gasoline plunging back down. That would be truly, truly amazing. And 10 year inflation expectations, as measured by breakevens (the difference between 10 year nominal treasuries and 10 year TIPS, the difference in those yields), is 2.3% right now. That’s just crazy. Tthose expectations are just too low unless velocity’s permanently impaired.

And what that means practically for you, the investor, is that if anything you should be overweight (still) inflation hedges even though inflation is coming down from its recent peak. At the very least you should be no worse than flat – you shouldn’t be short inflation here.

You probably should be in inflation-linked bonds still rather than nominal bonds. [There are] a couple of different reasons for that, but one of them is that right now inflation-linked bonds, or [rather] the nominal bond market, is pricing inflation way too cheaply. Inflation-linked bonds will give you actual inflation and it’s likely to be higher than what’s being priced in the nominal bond market.

Real estate, commodities…all these things which are classic inflation hedges are probably still good here,even though inflation is coming down. In general, equities are not good in that kind of circumstance, but if you’re going to be in equities – and everyone tends to hold some equities – you should look for firms with pricing power. What does that mean? Hell if I know what “firms with pricing power” means exactly. Everyone thinks they have pricing power until they don’t, and they think they don’t have it until they try it and discover that they do, right?

Right now, all kinds of firms do have power to raise prices and many of them are raising prices. So it’s hard to tell which ones are the ones that will be able to keep raising prices to keep up with the input cost pressure (largely wages) that they’re going to continue to have here going forward.

Which companies have the ability to sort of stay ahead of that? I’d say in general, you’re gonna look at firms that have a lower labor content, because commodity prices have come down…or they’re going up less fast, I guess. But labor rates continue to rise rapidly and probably will for some time.

I think firms with domestic supply chains are probably better off, or at least North American supply chains, are probably better off than the ones with long international supply chains.

I think that maybe something like apartment REITS could be interesting, especially because everybody was so convinced that that real estate was going to collapse – and it’s clearly not collapsing. Rents is something that tends to keep up with wages over time. Maybe rents have gotten a little bit ahead of themselves, but I think that the decline or the deceleration in rents is probably already kind of priced into those markets.

As always, by the way, podcast musings should not be construed as recommendations.

You know, I try to avoid mentioning specific tickers all the time because I’m an advisor and that gets sticky because if you recommend, say, Tesla, [then] you have to then give all the reasons why Tesla might go down and, you know, there’s all kinds of rules about that. So I try to not spend a lot of time recommending specific securities. But you know, you can always become a client! And we can talk all about it. Or you can send me email at inflationguy@enduringinvestments.com and we can have some conversations about that, but the bottom line is that you shouldn’t be letting your guard down.

Money velocity has been coming back for a while; it’s starting to come back more seriously. Even though money supply is declining, or flat to declining, it does not mean that inflation is going to plunge back to 2% because we have this potential energy that’s still working its way through the system. There’s no sign that velocity is permanently impaired.

So, don’t let your guard down. Defend Your Money! …and if inflation is coming for you, remember: you know a guy.