Archive

Multiple Poppycock Warning on Warsh Fed Meeting #1

People are worried about rising interest rates at the long end of the curve. “The Fed should raise interest rates,” they say, “to bring interest rates down.”

Just a quick rationality check there: read the sentence a couple of times.

I know you’ve been told that long interest rates go down when the Fed has ‘credibility,’ and they can only have credibility if they raise rates. That’s double-poppycock. First, because when the Fed raises interest rates, interest rates go up even at the long end of the curve. Don’t believe me? Here’s the 30-year bond yield, plotted against the Fed funds rate. I want you to find for me the place where the Fed tightened and yields fell. Go ahead, I’ll wait.

Now, I’m not saying that yields never go down when the Fed is hiking, or vice versa. It’s just very rare. And yields move around for lots of reasons, so sometimes Fed funds and long yields move in the opposite direction for spurious reasons. But it is super clear that the main driver of long interest rates is short interest rates.

I said it’s double-poppycock. The second way is because the notion that the Fed (or new Fed Chairman Warsh) will only have credibility if it raises rates is actually an embedded double-poppycock. First, because the Fed doesn’t have any credibility and hasn’t for years…unless you meant in the macro (but important) sense that people believe the Fed will ride to the rescue during a calamity. They don’t have any credibility as inflation fighters, because (a) until recently they hadn’t had to fight inflation for 35 years, so there was little opportunity to build inflation-fighting credibility and (b) the one time they did, they screwed it up so bad that they’re still fighting the inflation they created, five years later. The second of the embedded double-poppycocks is that raising rates is just the wrong thing to do, because raising rates without reducing money growth causes velocity to rise and inflation to accelerate.

Warsh has been pretty clear that to fight inflation, the Fed needs to shrink the balance sheet and slow money growth, and they can do that while lowering interest rates. I have no idea why people think that means he wants to raise interest rates, or needs to. But these are the same people who are seeing headline inflation jump because of rising gasoline prices and then tell you it makes it more likely the Fed is going to tighten.

Poppycock. Actually, double-poppycock. First, because rising gasoline prices affect mainly headline inflation and the Fed doesn’t even focus on headline inflation; second, because rising energy prices tend to slow growth, and historically the Fed has erred when they didn’t ease into a growth shock.

Now, having said all of that…there are currently some bad signs for inflation that the Fed should address by shrinking the balance sheet as quickly as they can. It was disheartening to head Chairman Warsh utter the poppycock (just one) about the system needing ‘ample reserves.’ The system did just fine for generations when the Fed had an extremely skinny balance sheet. The bigger problem now is that interest rates have risen enough that even if the Fed sold all of the bonds in the portfolio, it couldn’t drain nearly as much as they added by buying those bonds back when they were goosing things in 2020.

But here is the thing that I don’t hear people talking about, at least in the context of inflation and monetary policy:

The economy is just not slowing down very much…maybe it is just beginning to?…despite tighter financial conditions from higher interest rates and a supply shock from higher energy prices. Yeah, the 30y bond is at 5.2%. Where is that having an impact on growth? Higher rates mean less cash-out refinancing to help sustain consumption, a greater propensity to save (which is after all why market interest rates rise, to induce savings because other sources of dollars aren’t keeping up with the demand for dollars), and a stronger dollar which weakens foreign demand for our goods. Higher energy prices are, to be sure, a zero-sum game financially when we are mostly self-sufficient in energy, but historically higher energy prices have slowed ex-energy growth.

The fact that this isn’t happening, and that equities are not appreciably declining despite higher interest rates, is concerning because it suggests – to me at least – that there is too much liquidity in the system. M2 is rising at 5.5% y/y, and that’s too fast in the current environment (as I’ve pointed out before). It’s rising at a 7.2% annualized rate over the last 6 months.

And that’s happening partly because the Fed has been growing the balance sheet, not shrinking it.

It doesn’t feel like that is enough to explain the bulletproof economy, so it may be that there’s shadow liquidity from (for example) the growth of stablecoins. Now, economic growth is not a bad thing in itself, and growth doesn’t cause inflation. But if the amount of money growth is accelerating, and the benefit from holding non-cash balances is increasing (tending to raise velocity), and that’s enough to keep the economy pushing right through an energy shock and the higher cost of money…then to me that says it’s going to be hard to keep it from leaking into prices. The Fed does not need to hike rates – that would only make things worse. The Fed needs to take stern action on the balance sheet, though, and soon.

Inflation Guy’s CPI Summary (May 2026)

While the worst is probably over for the monthly CPI prints, the real question going forward is ‘how much better does it get?’ We know that energy prices will eventually retreat, but even if they merely flatline they will stop flattering headline CPI. But where does core and more importantly median CPI settle in? That’s the real question. For now, we just have one more month of data so let’s dig in.

The economist surveys had CPI at +0.51% headline and +0.27% core. The inflation swaps market was in roughly the same place, with +0.66% NSA the last trade.

The last month has seen a lot of volatility in markets (duh), but in particular a significant increase in real yields.

Nominal yields have risen a bit, and get all the ink when 30-year yields peek above 5%. That actually masks the real problem, which is that nominal yields have risen so little only due to the sharp decline in inflation expectations. In the front of the curve, that decline in breakevens is significantly a carry phenomenon (as we roll through months with solid NSA accretion) and so, therefore, is some of the rise in real yields. But a 40bps increase in real yields at the 5-year point gets one’s attention. And at 2.17%, 10-year real yields are near the absolute highs they’ve seen since the Lehman-related spike over 3% in 2008.

(Oh, and if any technician tells me this is a ‘flag’ formation projecting to 5%, I’m going to smack you. Real yields don’t go to 5%.)

The uptrend in real yields, as an aside, has also been bad for gold. Gold behaves like a long duration TIPS bond and as TIPS have sold off, gold has been a whipping boy. That won’t last forever. I like buying 10-year TIPS anywhere north of 2%, and if real yields get above 3% some day – back up the truck. Let’s hope that isn’t soon though.

The actual data comes in today at +0.473% m/m on headline CPI and +0.208% on core CPI. Both of those are below expectations, with core a meaningful miss. Here are the last 12 core CPI figures (keep in mind that last month’s jump was a payback for the 6-months-ago quirk in rents due to the government shutdown).

And here are the m/m, y/y, and prior y/y for 8 major subgroups. It’s striking that Apparel is +4.8% and “Other” is +4.9%. Those are not usually exciting categories! I’ll return to this a little later.

Here is the coarse breakdown of core goods (+1.06% y/y) and core services (+3.42%).

It isn’t surprising that core goods is decelerating. It’s actually somewhat concerning that it isn’t decelerating faster. The hook higher in core services bears some further investigation. Even though the overall numbers looked good this month, this breakdown isn’t all sunshine and roses.

Primary rents were +0.36% m/m, and 2.92% y/y versus 2.79% last month. OER was +0.3% m/m, 3.32% y/y. The jump in Rent of Primary Residence is a little concerning (although I will note that it puts the actual y/y number exactly on our model, which goes pretty flat near this level for the next year). Last month’s hook higher made sense because of that make-up month due to the shutdown/6-month lag effect. But that isn’t the issue here. Lodging Away from Home was alto +0.4% m/m, 5.2% y/y. Some people will say this is a World Cup effect, and possibly we are seeing a little bit of that in Lodging Away from Home. But this isn’t France. The US is a pretty huge country and there is no way that World Cup tourism is enough to move rents for the entire country.

But landlords are seeing higher direct and indirect costs. This is why rents are not going to go into broad deflation any time soon.

What might also be flagged as a World Cup effect, but more likely is just jet fuel pass-through, is the 2.69% m/m rise in Airfares after a 2.82% rise last month. I have airfares just slightly above the model given jet fuel prices, and within the error bars, so if there’s an impact there it’s pretty small. I think this is worse in Europe. Airfares are indeed part of the story in the core-services move higher that I noted above. Rents are too, but the airfares increase is easier to figure out.

The median category this month looks like Recreation at 3.51% annualized m/m. I may be slightly low, depending on where the regional rent indices get adjusted, but my guess for Median CPI is +0.287% m/m for a small acceleration y/y to 2.83%.

I have to say – if you shovel some of April’s jump back into October and November where it belongs – it still doesn’t look like deceleration to me.

Okay, here are the four pieces charts. Food & Energy +9.81% y/y. Core Commodities +1.06% y/y. Supercore +3.55% y/y. Rent of Shelter +3.33% y/y

The Core Services less Rent-of-Shelter (Supercore) is the one I don’t like, but again part of that is the Airfares/energy thing. None of this looks like super good news, though.

By the way, there were only 3 categories that declined at a faster annualized rate than 10% this month: Car and Truck Rental (weird) at -40% annualized, Motor Vehicle Insurance (very weird) -18%, and Misc Personal Goods -11%. Above 10%, and ignoring food and energy, we have Jewelry/Watches (41%), Misc Personal Services (28%), Communication (17%), Tobacco and Smoking Products (+13%), Infants/Toddlers Apparel (+12%). Motor Vehicle Maintenance and Repair just missed the cut at +9.95% annualized.

Here are a couple of interesting things I’m watching. This chart is Computer Software and Accessories, and it’s where AI tools land. Now, it’s a tiny, tiny part of the basket at the moment but I’ll bet it’s larger when they reweight next year. This is the NSA price index, not the rate of change – so prices for computer software and accessories are higher than they’ve been for years.

Like I said, this is a tiny category but it actually matters more for PCE. That fact annoys the Fed, who just published a research piece (https://www.federalreserve.gov/econres/notes/feds-notes/measurement-of-computer-software-and-accessories-inflation-20260522.html) explaining that this is partly ‘measurement error.’ Uh-huh. Boy are we getting picky.

Also, I happened to notice that computer prices are actually increasing, due to upward pressure on DRAM and other component prices thanks to AI demand. This sort of annoys me because I need a new laptop and the prices aren’t going down like they usually do if you wait. And yes, that’s the main reason I noticed.

This is one of those categories that animates conspiracy theorists because the BLS hedonically adjusts it…so since computers are always improving, there’s a general decline in the quality-adjusted-price over time. Well, not just a general decline, but a pretty large decline. “But computer prices haven’t actually fallen! Yes I get more computer but I don’t have the option to get the old one! I want my Windows 95!”

So prices going up, at least if it continues, is interesting. It’s a symptom of AI demand. It’s still not a large part of CPI, but I think AI is going to start showing up more here and there. Like here:

This is obviously not all AI – the upswing happened in the aftermath of COVID, possibly partly because work from home means power needs are broader throughout the day. But the continuation recently…I am pretty sure AI data center demand, if it isn’t yet affecting this, is going to!

And that is emblematic of the long-term story here. Not this month’s story per se. But these upstream pressures on petroleum and electricity are passing through more and more downstream. And that’s a hard dynamic to arrest. It is difficult to put that genie back in the bottle.

Now, this isn’t to say there is no good news.

This is Medicinal Drugs, aka pharmaceuticals, in core goods. It was -0.8% this month after -0.3% last month, and is -2.2% y/y. This looks like a real TrumpRX effect. On the other hand, Hospital Services is still rising at about 6% y/y, so while overall Medical Care in the CPI is +2.6% y/y, that’s being flattered because of the TrumpRX effect which won’t last forever.

Now, earlier I pointed out Apparel’s interesting y/y increase. The absolute price of apparel basically peaked in 1993 or so. This is a wonderful picture of the power of offshoring, as we went from producing a lot of apparel domestically to producing basically nothing, and saw apparel prices decline in real terms and even in outright terms for nearly 30 years. There was a sharp dip and recovery due to COVID, but in the last year or so the Apparel index has actually gone to new all-time highs.

Some of that is re-onshoring. Some right now is actually petroleum since many types of fibers are downstream petroleum byproducts. Think polyester, but it’s broader than that. But prices prior to the energy spike were already at 20-year highs.

The bottom line here is that the rise in the headline CPI is causing some people to shrilly declare that the Fed needs to raise rates. That’s ridiculous – the Fed looks through energy price increases. Although as I said before, those energy price increases, if they are sustained long enough, start to percolate through, and they appear to be…core and median and trimmed mean CPI won’t be heading back to target (not that there is a target any more) any time soon. As long as the economy stays pretty strong, the Fed has actually stumbled into what should be a comfortable spot for a while. Warsh will work on trimming the balance sheet, hopefully, but I wouldn’t expect rate changes for a while and that’s a change in my view from before when I thought the Fed would be easing (I thought growth would be weaker and I continue to be confounded on that). I’m saying that while the headline inflation data look ugly, that will pass as energy prices decline. But I do think it will be difficult for the Fed to get comfortable with Median CPI going back up, or just not going back down, while growth is strong.

“Mike, Mike, Mike…you’re making too much of these little things! Core doesn’t look too bad. Median is not alarming.”

Yes. But electricity, petroleum, the demographic pivot, re-onshoring, and let’s not forget money growth. These are not small things and they affect how difficult the future looks with respect to inflation. The tree’s leaves are pretty but the trunk is rotten. I am not optimistic about future shade.

Time to Choose Your Inflation Adventure with Velocity and Money

We have CPI coming up in a few days, but M2 came out recently and it is worth commenting about, so let me drop some thoughts about the state of money and velocity right now and the context we are operating in.

M2 grew 0.88% in February, causing the y/y change to rise to 4.88% (quarterly, however, it is 6.65% annualized). I saw somebody recently observe that money growth was about 6ish back before COVID, so this level is not very worrisome to that pundit. I think that’s wrong – not that this level is worrisome in the big picture, but the trend is bad and the current level is actually not consistent with low and stable inflation as it was prior to the late twenty-‘teens.

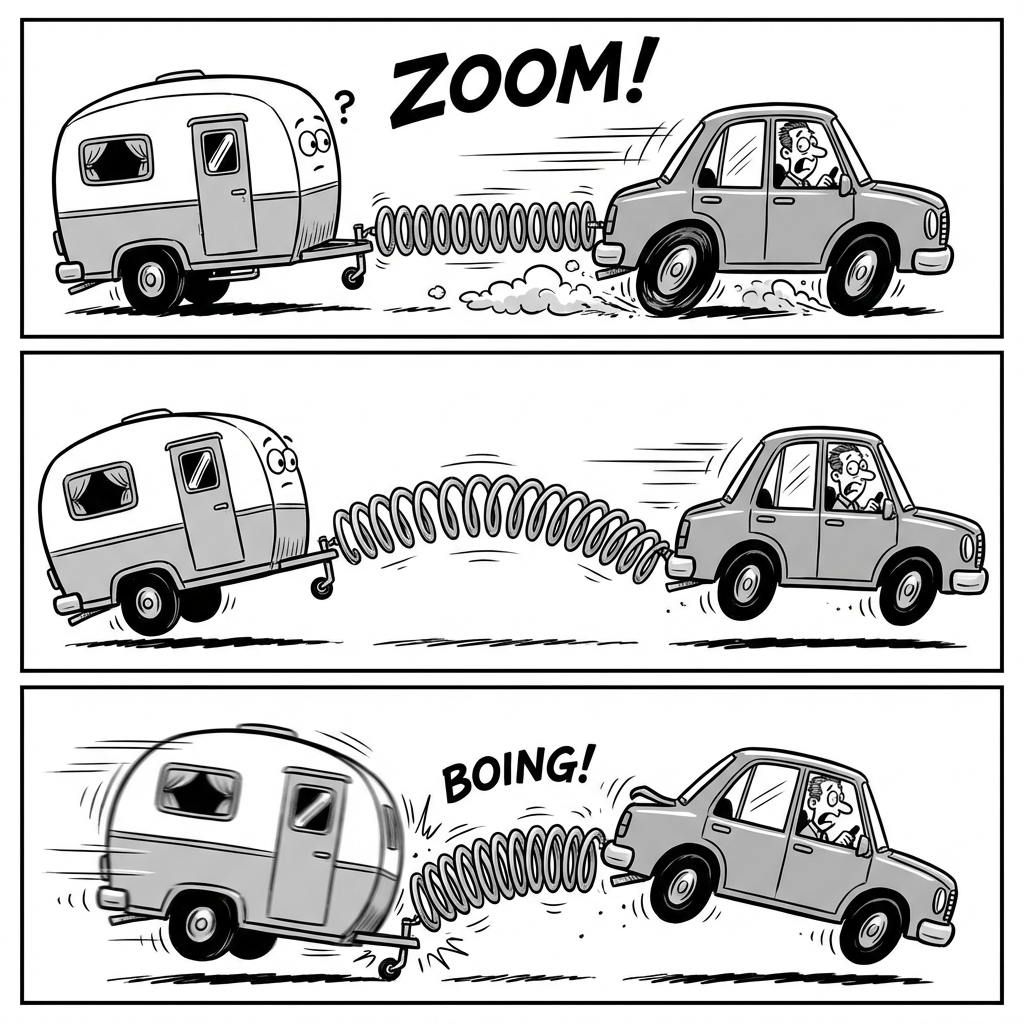

Before we get to that, let’s review the state of play for money velocity. Remember when velocity plunged early in COVID, and people said inflation wouldn’t happen because the transmission mechanism was broken? That comment was so funny it made me blow milk out of my nose, even though I wasn’t drinking milk. It was entirely an artifact of the different time frames over which the money supply was changing, compared to the time frames required for prices and output to change. MV=PQ, and M was changing suddenly. Since GDP can’t suddenly change 20%, money velocity became the capacitor that held the excess charge which slowly bled into prices. In my podcast, and occasionally in this blog, the image I shared was of a car rapidly accelerating away from a trailer hitched to it by a spring. At first, inertia keeps the trailer from traveling as fast as the car, and the spring stretches. Once the car stops accelerating, though, the spring compresses and the trailer catches up. The illustration below is courtesy of Lovart.ai.

So where are we? Here is the US monetary system over the 2019-2025 period showing total growth from December 2019. The x-axis shows the total percentage growth in money as a percentage of real output (M/Q). The y-axis shows the total change in the price level. Now, I have to point out that when I was talking about this, in 2021 or 2022, we were very far away from the diagonal line showing where the two changes are equal. And I said we would be going back to the line, and we went back to the line. People really ought to listen to me more.

The other way to look at this is that velocity is back almost to where it was prior to COVID.

So is there any problem here? Velocity is back to where it was, but if it’s stable and money is growing at 4.9% y/y, then P+Q grows at 4.9%, so 2% inflation with 3% growth…sounds pretty good.

This is where we review the “but 6% worked!” argument.

You can see from the chart that yes, since the late 1990s M2 grew at 5-10% and we never had much of an inflation problem. Why now? Well, during that period velocity was steadily declining – and that is the only way that you can sustain 6% money growth with 3% real economic growth and get 2% inflation. The question, then, was why velocity was declining. Remember, some people think this is a trend, because they don’t really understand what drives velocity. During that period, interest rates steadily declined. This was also a period of increasing globalization and a demographic dividend (more workers relative to the aged). Now, whether the interest rates declined because of those trends because both trends were disinflationary, or if interest rates declined because of a dovish Fed and they only got lucky because of those trends…I don’t know. But the point is that the largest driver of lower money velocity during that period was lower interest rates.

And interest rates are now approximately fair. Some people think they’re too low with inflation too hot, some people think they’re too high with economic growth seeming to slow, but let’s just say they’re not 300bps wrong at this point. Here is our velocity model. With lots of crazy volatility, it has velocity pretty close to on-target. Here’s the problem: the last time prior to COVID were as high as they are now (I’m looking at 5y Treasuries), it was also prior to the Global Financial Crisis and the regime of interest rate repression. Back in 2007, 5y rates were this high, and money velocity was about 2.0, some 40% higher than here. What is holding velocity down right now in our model is a very high level of economic policy uncertainty, which causes people to hold more cash than they otherwise would given the level of interest rates. Thanks to the war between the President and his allies on one side, and the minority party on the other side, not to mention the Iran war, there is a lot of uncertainty right now and that is causing people to conserve cash.

It won’t always be that way, but with M2 growing near 5%…it really needs to be that way. By the way, the money growth situation is a bit worse than it looks, too: there has in the last couple years been a fairly dramatic rise in the amount of non-M2 money that is growing in defi/crypto space. Bitcoin isn’t money, but stablecoins are very much like money. The scale of the Stablecoin money supply is small compared to the ‘off-chain’ money supply, but it is starting to get large enough to matter. Anyway, we know the sign of that growth, and it’s a big fat plus.

So no, 6% is not a stable rate of money growth going forward from here. This is not the early 2000s. It is not the 1990s. If we could manage to just have 6% growth, then we’re probably going to end up being in the mid-to-high-3s on inflation, and that’s tolerable. But if that’s the midpoint of money growth, then mid-to-high-3s is the midpoint on inflation with some periods a little below that and some periods a little above that.

Economies adapt, and an economy can work fine at 4-5% inflation or even higher as long as it is stable. But 4% inflation feels different than 2% inflation, and the economy will work differently in that sort of regime. Businesses will be more likely to pass through cost increases rather than absorb what they think are short-term variations (see “How Expecting Inflation Un-anchors Manufacturers’ Pricing Strategy”). Equilibrium equity prices are lower. Menu costs and search costs go up. And so on. We may already be seeing some of these long-term structural changes. The Fed just published a FEDS Notes entitled “Is the Inflation Process in Advanced Economies Different After the Pandemic?” The short answer? Yes it is. The question is, are we on track to get the inflation process back to the way it used to be? And the answer there appears at this juncture to be: no.

Inflation Guy’s CPI Summary (January 2026)

Let’s start by setting the context for today’s CPI number.

A couple of months ago, we missed a CPI because of the shutdown. The BLS simply didn’t have any data to calculate the October 2025 CPI. That wasn’t the real problem. The real problem was that the BLS’s handbook of methods more or less forced it, in calculating the November CPI index, to assume unchanged prices for October for some large categories – in particular, rents. This caused a large, illusory decline in y/y inflation figures. Importantly, this was also temporary – there has been some catch-up but the big one comes in a few months when the OER rent survey rotation will cause a large offsetting jump in that category, exactly six months after the illusory dip. Until then, inflation numbers will be more difficult to interpret and the year-over-year numbers will be simply wrong. So when you read that today’s figure resulted in the “smallest y/y change in core inflation since 2021, and consistent with the Fed reaching its target” – that’s just wrong. The true core y/y number is roughly 0.25%-0.3% higher than what printed today. The CPI ‘fixings’ market is currently pricing headline CPI y/y to rise to 2.82% four months from now, and that isn’t because of a coming rebound in energy prices.

I guess what I am saying is this:

Ladies and gentlemen, please take your seats. We will be experiencing some mild turbulence.

January, in general, is already a difficult month in CPI land because of the tendency for vendors of products and services to offer discounts in December and then implement annual price increases in January. But those price increases are not systematic, which means they are difficult to seasonally-adjust for. Ergo, January misses are rather the norm.

So with that context, the consensus estimates for today’s number were for +0.27% m/m on the headline CPI, and +0.31% on core. Some prognosticators were quite a bit higher than that – I think Barclays expected +0.39% on core CPI. The question was basically whether there is still any tariff increase that needs to be passed through; if so then January is a good time to do it. That didn’t really happen. The actual print was +0.17% on headline and +0.30% on core.

The miss on headline happened because while gasoline prices actually rose in January, the average price in January was lower than the average price in December – because in December, gasoline prices dropped sharply. While Jan 31 gas versus Dec 31 gas was $2.87 vs $2.833 (source AAA), January 1 vs December 1 was $2.83 vs $2.998. So, even though gasoline prices rose over the course of January compared to the end of December, that’s now how the BLS samples prices.

Be that as it may, core inflation was pretty close to target. One way to look at it is that y/y Core CPI, at 2.5%, is the lowest since March 2021. Another way to look at it is that the m/m Core was the third highest in the last year, and annualizes to 3.6%. So is it ‘mission accomplished’ for the Fed? Erm, nothing in the chart below tells me inflation is trending gently back to 2%. You?

The core number was actually flattered by a large drop in used car prices, -1.84% m/m. Used car prices actually rose in January, but less than the seasonal norm so that resulted in the large drop and that caused a meaningful drag. (Let’s not get in the habit of just dropping everything that doesn’t fit the narrative, though.) Anyway, core goods as a whole dropped to 1.1% y/y from 1.4%, while core services eased to 2.9% y/y from 3.0%.

While core goods fell more than expected because of that Used Cars number, it’s not surprising that it is moderating some. The question isn’t whether core goods prices will keep accelerating to 3% or 4%; the question is whether it stays positive, or slips back to the negative range it inhabited for many years. That’s an important story even though core goods is only 20% of the CPI. Until now it has been a ‘tariffs’ story, but going forward it’s an ‘onshoring’ story. My contention is that we should not expect a return to the persistent goods deflation that flattered CPI for a generation thanks to offshoring of manufacturing to low-labor-cost countries, because the flow is reversing. That is the story to watch, but it isn’t January 2026’s story.

While we are talking about autos, I’ll note that New Cars showed a small increase. I wonder (and I don’t have a strong forecast here) what the changes in car sales composition now that electric vehicles are no longer being pushed by the executive branch. Obviously non-electric cars are cheaper, so if we had a real-time measure of the average sales price of a car it would probably fall as consumers go back to buying cars they want instead of cars that look cheaper because of tax breaks. I don’t know though how much actual sales will change (auto production will certainly change as carmakers no longer have to check the box by making a certain number of cars that were hard to sell), and I don’t know how detailed the BLS survey is and whether it takes into account fleet composition. I guess we know that if there’s any effect, the sign should be negative. I suspect it is a small effect.

Turning to rents, as we do: Owners Equivalent Rent was +0.22% versus +0.31% last month. Rent of Primary Residence was +0.25% vs +0.27% last month. The chart below shows the m/m changes in OER… except that it does not show the 0 for October. There’s clearly a deceleration here, but my model says it should be flattening out right about at this level. Also not January 2026’s story, but it will be 2026’s story.

There was a small decline, -0.15% m/m, in Medicinal Drugs. Some folks had been eagerly waiting for that to show a large drop, thanks partly to the Trump Administration’s efforts to force drug manufacturers to align prices in the US market with prices in the ex-US market. There is not yet any discernable trend. Potentially more impactful is the Trump RX initiative, which by bringing transparency and cutting out the middleman in the really-effed-up consumer pharmaceuticals pipeline (dominated by three big wholesalers and three big pharmacy benefit managers, each of which is highly opaque about pricing) could well cause a significant decline in consumer-paid drug prices. But…remember that when those drugs are paid for by the insurance company, it isn’t a consumer expense and only shows up indirectly in the CPI. Yeah, that makes my head spin also. Bottom line: pharmaceutical prices are likely to decline some for consumers, but we just aren’t really sure where that will show up in the CPI and how soon it will happen.

The best news in the report today is the continued deceleration in core-services-ex-rents (‘Supercore’), which decelerated even with Airfares being +6.5% m/m.

Psych! You fell victim to one of the classic blunders! This is again a y/y figure that is flattered by the lack of October data. On a m/m basis, supercore had the biggest jump in a year, +0.59% (SA). Still, I think this is decelerating along with median wages deceleration. Of course, all of that data is messy right now as well, but the spread of median wages over median inflation remains right around 1%.

There is some early evidence that the downward slide in wages might be leveling off; if it does, that will limit how fast supercore can moderate. There are also some cost pressures in insurance markets that are probably going to show up in the next 6 months or so. But that’s not January 2026’s story.

The story in January 2026 is that the waters remain muddied by the government-shutdown-induced gap. The current y/y figures are all flattered by that event, and exaggerate how good the inflation picture is. That’s how the Administration can trumpet victory while the reality on the ground is that inflation is not converging to trend.

I’m working on the assumption that the Fed knows this, and the combination of core inflation that seems steady around 3.5% (abstracting from the shutdown gap), better-than-expected labor market indicators, and a distinct animus among current Fed leadership towards the President means that there’s no reason to expect an adjustment in overnight rates any time soon. Frankly, I think the argument is better for a rate increase than a rate decrease. On the other hand, rents do appear to be continuing to decelerate even if we ignore the October gap. My model says that isn’t going to continue, and even if I’m wrong I’m likely to be closer than the folks calling for deflation in housing. And moderation in Supercore is encouraging, even if – again – I don’t think that continues to the point the Fed needs it to be. Core goods inflation appears to have peaked, and the question is whether we go back to core goods deflation or not.

In each of these cases, my modeling suggests that the current level of median inflation of around 3.5% (ex-gap) is likely to end up being an equilibrium-ish level. But it isn’t ridiculous to look at the current trends and see good news on inflation. Either way, there’s not a Fed ease coming imminently. But if those trends continue until Warsh is confirmed and becomes Fed Chairman, there could be a rate cut later in the year.

But that’s not January 2026’s story.

What Makes a Stable Coin Stable?

The early growth of Bitcoin and the cryptocurrency space was originally stimulated by the mistrust of centralized control of monetary policy and financial institutions. While Bitcoin is a fiat currency, in the sense that it is not ‘backed’ by anything and has value only because other people believe it has value, the rules for the expansion of the total float of Bitcoin are mechanical and so the unit benefits from being isolated from the whim of flesh-and-blood central bankers. Milton Friedman once said in an interview with the Cato Institute that “We don’t need a Fed…I have, for many years, been in favor of replacing the Fed with a computer [which would, each year] print out a specified number of paper dollars…Same number, month after month, week after week, year after year.”[1] And, with Bitcoin, that is exactly what you have. Management of Bitcoin is decentralized, automatic, and the rules are stable.

Unfortunately, ‘fiat’ cryptocurrencies are anything but stable. Moreover, since their value depends entirely on the trust[2] of other actors in the economic system that these currencies will have value, it is entirely possible that any of them could crash just like any fiat currency sometimes crashes when confidence in the currency issuer vanishes. There is no intrinsic value to a fiat currency – digital, or analog – which means that they are stable only when looked at in a self-referential frame. A US Dollar has a stable value of $1 but is volatile from the viewpoint of a Mexican-peso-based observer. I will return to this observation presently.

Because these fiat cryptos are unstable when looked at by a participant in the analog world, the concept of ‘stablecoin’ was developed. In Coinbase’s summary ‘What is a stablecoin?’, the first two bullet points are:

- Stablecoins are a type of cryptocurrency whose value is pegged to another asset, such as a fiat currency or gold, to maintain a stable price.

- They strive to provide an alternative to the high volatility of popular cryptocurrencies, making them potentially more suitable for common transactions.[3]

Why is a stable price important? The answer goes back to the question of whether Bitcoin and similar cryptos are money, or assets. In the conventional definition of money, such a label only applies to units that provide a medium of exchange, store of value, and unit of account. First-generation cryptos certainly serve as a medium of exchange but are sketchy on the ‘store of value’ and ‘unit of account’ dimensions. Nothing natively is priced in BTC, so it is not a good unit of account, and the high volatility creates a high barrier to any argument about being a store of value. Cryptos are most assuredly financial assets. It is hard to argue that they are money.

Enter the stablecoin. By pegging the value to an existing currency, a stablecoin ‘borrows’ the characteristics of that currency as a store of value and unit of account. It’s true by mathematical association: if USDC is equal to one US dollar, and the US dollar is money, then (as long as it’s accepted a medium of exchange) USDC is money because it has equal ‘store of value’ and ‘unit of account’ dimensions.[4] A stablecoin maintains its stability by means of holding reserves and being fully convertible on demand into the underlying currency.[5]

But Stable with Respect to What?

Stability, though, depends on the frame of reference. Consider a stablecoin linked to the US Dollar, which always can be minted or burned at $1 (ignoring fees). Consider a second stablecoin linked to the Japanese Yen, which always can be minted or burned at ¥1. Which one is stable?

Figure 1 – US Dollar Frame – US Dollar is stable

Figure 2 – Japanese Yen Frame – Japanese Yen is stable

The answer, of course, depends on your frame of reference. From the standpoint of someone in Japan, who is buying goods and services with Yen, a stablecoin like USDC that is linked to the dollar is most assuredly not stable in any useful sense of the word. Conversely, a US dollar investor would not find a Yen stablecoin to be stable. This, then, is an important element of defining a stablecoin: something which matches the volatility and behavior of the basis of the frame you are in, is stable with respect to you. This raises an interesting question when it comes to stablecoin regulation. A coin could very easily be regulated as a stablecoin in one jurisdiction, and not be regulated as such in a different jurisdiction – even between regulatory jurisdictions that are congruent in their treatment of most assets.

What passes for stability, in short, depends on the transactional frame – literally, the underlying currency in which transactions happen – of the observer.

Stable with Respect to When?

The meaning of stability also fluctuates with the time horizon of the observer. Fixed-income investors are very familiar with the concept of Macaulay duration, which is the future horizon at which the value of a bond holding is completely insensitive to parallel shifts in the yield curve, because the change in the value of reinvested coupons (which goes up with higher interest rates) exactly offsets the change in the value of the remaining cash flows (which go down with higher interest rates). What is the riskiness of a bond with a 7-year duration? Or more to the point of this discussion – which is riskier, a 1-month Treasury bill, or a 7-year zero coupon bond?[6]

As it turns out, it depends on the applicable horizon of the observer.

Suppose an investor pursues one of two strategies: in the first strategy, he or she buys a 1-month Treasury bill, initially at 5%, and then rolls the proceeds every month for 7 years. Alternatively, he or she could buy a 7-year zero coupon bond yielding 5%. Using a simple two-factor model with no drift, I generated 250 iterations of T-bill paths and yield curve shapes, to produce hypothetical monthly time series of returns for the two strategies. For example, here is one such random path (Figure 3):

Figure 3 – Illustrative single random path of cumulative returns for two strategies

The a priori expected return is approximately the same for both strategies; sometimes the T-bill roll strategy ends up ahead and sometimes the buy-and-hold strategy wins. With similar expected returns, a rational investor would therefore choose the one which has the lowest risk. But the riskiness or stability of the returns depends very much on the observer’s time horizon. Each of the following three charts is drawn from the same 250 Monte Carlo iterations, but the cumulative return is sampled at a different horizon. In Figure 4, the cumulative returns are sampled at the 1-month horizon. In Figure 5, the sampling is at the 3-year horizon. In Figure 6, the sampling is at the 7-year horizon. For each figure, the cumulative return for the T-bill strategy is shown on the x-axis and the cumulative return for the zero-coupon-bond buy-and-hold strategy is on the y-axis.

Figure 4 – 1-month T-Bill strategy is riskless at a 1-month horizon

Figure 5 – Both strategies are relatively risky at a 3-year horizon

Figure 6 – The 7-year zero-coupon-bond is riskless (in nominal terms) at a 7-year horizon

Although this conclusion is trivial and inevitable to fixed-income investors, the reason for our observation here is to point out that what is considered ‘stable’ not only depends on one’s functional currency but also on one’s holding period horizon.

Is the Nominal Frame the Most Important Frame?

The prior points are likely obvious to most investors. If you are investing with the intention of spending the proceeds in US Dollars, then a USD frame is most relevant. If you are investing for a known future nominal payout (for example, a life insurance company hedging scheduled annuity flows), then an investment that matures to a given value at the time when the money is needed is the most-relevant frame. However, investors sometimes lose track of one of the most important frames, and that is the “real” frame where values track the price level.

While a $1 bill is ‘stable’ in nominal terms – it will always be worth $1 – it is very unstable in purchasing-power terms.

Figure 7 – A dollar is inherently unstable in the main consumer frame

The framework where we ignore the value of the dollar, in preference for the fixed price of the dollar at $1, is the “nominal” framework. When inflation is low and stable, this frame is a useful shorthand in much the same way that when traveling abroad a tourist in the year 2000 might translate Mexican Peso prices into US Dollar prices by dividing by 10 even though the exact exchange rate differs from 10:1. In the short term, such a shortcut framework makes up for in convenience what it surrenders in precision. But in the long term, what starts out as mild imprecision becomes wildly inaccurate as the Peso exchange rate has gone from 10:1 to 20:1.

Similarly, while the nominal frame is the default for short-term comparisons it is clearly not the most important one to a consumer. Someone who is negotiating a salary at a new job, who knows he or she made $40,000 per year in 2004, would be ill-suited to use that figure as the starting point. The frame that matters over time is the real, or inflation-adjusted, frame. In the chart above, if we plotted the purchasing power of an inflation-adjusted 1983 dollar, it would be a flat line at $1.[7] On the other hand, if we plotted the nominal value of that same inflation-adjusted 1983 dollar, it would show a mostly steady increase from $1 to $3.15 over the same time period.

As before, the frame matters. A dollar that is stable in nominal space is very unstable in purchasing-power space. A unit that is stable in purchasing-power space looks unstable in nominal space.

If an investor or consumer had to choose one frame to care about, it would surely be the one in which his or her money represents not just a medium of exchange and a unit of account, but also a store of value. What this means is that a coin that is native currency and inflation-adjusted in the local price level is the most stable of stablecoins. And what that further implies is that what we currently call ‘stablecoins’ are stable only in the narrow context of being fixed at a certain nominal value of domestic currency…and that is suboptimal since all investors and consumers live in a world where prices change.

Tying Frames Together

What is interesting is that each of these frames describes “stability” in a different context. People in one frame see their own side as stable and the other side as volatile – and the exact same thing is true, in reverse, for the other side.

The various frames do traffic with each other. A holder of US Dollars (in the nominal-USD-short-term-stable frame) exchanges those dollars with a person who holds Euros (in the nominal-Euro-short-term-stable frame). We call that an exchange rate. And what ties together the nominal dollar and the inflation-linked dollar is the price index.

Figure 8 – Exchanging dollars with different purchasing power is functionally the same as exchanging currencies with different purchasing power.

In fact, the relationship between the Dollar and the Euro is so much like the relationship between the nominal dollar and the inflation-linked dollar that in 2004 Robert Jarrow and Yildiray Yildirim wrote a paper describing how to value inflation-protected securities and derivatives using a model designed for foreign exchange.[8] And that highlights the fact that an inflation-linked stablecoin isn’t some strange construct but rather an important new product to be added to the cryptocurrency universe. It is just another currency – one that is fixed in time, rather in nominal dollars, that is exchangeable to today’s dollars at the ‘inflation exchange rate’. If a 1983 dollar existed today, it could be exchanged for $3.15 current dollars because the dollar that was frozen in time in 1983 buys more than today’s dollars. That’s just an exchange rate!

Conclusion

It seems that ‘stability’ is not a stable term. Perhaps a more accurate description of the current crop of ‘stablecoins,’ which are exchangeable 1:1 with the base currency, is “fixed coins.” Only an inflation-linked coin would be a “stablecoin” in the true sense of the word, and only because being stable in purchasing-power space is the most important frame.

[1] http://www.cato.org/publications/commentary/milton-rose-friedman-offer-radical-ideas-21st-century

[2] This is not to be confused with the trustless nature of the transaction verification process of the blockchain, where the peer-to-peer nature of the process allows transactors to be certain their counterparty has the amount of bitcoin in question before completing a transaction. Rather, this is a comment on the entire system itself.

[3] https://www.coinbase.com/learn/crypto-basics/what-is-a-stablecoin

[4] Arguing that a coin pegged to gold or other commodities is a stablecoin is a bit of a stretch. Such a coin may be granted intrinsic value by such backing, and it may even be a better store of value in the long run because of such backing, but it is lacking as a unit of account (nothing is priced in gold units) and as a short-term store of value it leaves a lot to be desired.

[5] So-called ‘algorithmic stablecoins’ are mostly stable because of fiat reasons. That is, only because people believe the algorithm can guarantee that the coin is fully backed, will they behave as if they are. My usage of ‘stablecoins’ leaves out algorithmic stablecoins.

[6] I made this a zero-coupon bond to make it easier. A zero-coupon bond has a Macaulay duration equal to its maturity. However, at the 7-year horizon, any bond with a 7-year Macaulay duration has the same risk to a parallel shift of the yield curve: none. The point of this paper, though, is not fixed-income mathematics so take my word for it for the sake of this argument.

[7] Naturally, whether it is truly precisely flat depends on whether the price index we are adjusting with is an accurate representation of changes in purchasing power. Of course, such an index would look different for every person based on his or her consumption patterns so the line would not be truly flat for any person. But it would be much more stable than the non-inflation-adjusted dollar.

[8] Jarrow, Robert A. and Yildirim, Yildiray, Pricing Treasury Inflation Protected Securities and Related Derivatives Using an Hjm Model (February 1, 2011). Journal of Financial and Quantitative Analysis (JFQA), Vol. 38, No. 2, pp. 337-359, June 2003, Available at SSRN: https://ssrn.com/abstract=585828

Inflation Guy’s CPI Summary (June 2024)

Let’s set the stage. Last month (May’s data), core CPI printed at +0.16% and +0.25% on Median. But a lot of that, most of it, was core goods and the question was whether that month was a one-off due to be reversed at some point, or if shelter and other slower-moving things would come along. Coming into this month, the economists’ consensus was for +0.21% on core; the inflation swap market trades headline inflation but actually implied something a tiny bit softer than the economists were expecting. We knew Used Cars was going to be weak again, but it seemed like people were all-in on the idea that the worm has turned and now inflation is going to head sharply lower.

Whether this turns out to be true or not, it’s important to realize that the reason economists think that is because unemployment is rising, indicating that we are either in or very near a recession, and economists think (against logic and data) that wages lead prices so this should herald a disinflationary pulse. Now, I also think inflation is headed lower, but it’s because shelter is coming off the boil and not because the Fed successfully cracked the backs of labor.

So what happened this month?

We saw a very weak headline number of -0.06%, which was mainly the fault of a very weak core inflation number of +0.06%. That’s the second quite weak core figure in a row, and when median CPI comes out later today it should be even weaker than last month, at +0.195% or so. If we could repeat that median every month, it would be tantamount to inflation being at the Fed’s target because median normally tracks a little higher than core except when we are in an inflationary upswing.

But whereas last month’s inflation figure was all about core goods, this month we finally saw a bit of a deceleration in shelter. Okay, yes – core goods slipped further into deflation, because that category exists mainly to make me look stupid by going lower and lower when I keep thinking the disinflation must be nearly wrung out. Core Services dropped to 5.1% y/y from 5.3% y/y.

We had known Used Cars would be weak, and it was at -1.5% m/m. New cars also dragged. But I will say it again because I want to have the chance to appear stupid again next month: goods deflation is running its course. Global shipping costs are rising again, the dollar will be vulnerable if the Fed begins to ease, and while used cars should continue to show large y/y declines for the next few months that’s mostly base effects. On an index level, the used cars price index is almost all the way back to the overall price level. Since COVID, the general price level – what has happened to the average price of goods and services – is up 22.3%. Used Car prices are now only up 27.7%. Not all goods and services will move up exactly 22.3%; the point is that the dislocation in used cars is pretty much over and therefore we should expect at some point that used car inflation will start to look more like overall inflation.

But again, goods aren’t the story we really care about. The question is, what about services? The news here is all non-bad. (Some of it is good, some is just not bad.) This month, the story is that rents abruptly weakened on a m/m basis. Primary Rents were +0.26% m/m (was +0.39% last month), and Owners’ Equivalent Rent was +0.28% (was +0.43% last month). This dropped the y/y rates to 5.07% and 5.45%, respectively.

That’s good news, but it is not unexpected news. The conundrum over the last 3-6 months has been why this wasn’t already happening. On a m/m basis, the rent numbers probably won’t get a lot better, but if they print around this level consistently then the y/y rent numbers will decelerate gradually. Unfortunately, there is no sign of deflation in rents and they are likely to begin to reaccelerate later this year, or early next year. That is an out-of-consensus view, though, and you should keep in mind that the Fed believes we have imminent deflation in rents.

In addition to the softer rents numbers, Lodging Away from Home showed -2% m/m. However, like airfares (-5% m/m), LAFH is not something that is going to be a persistent large drag. It’s volatile. On airfares, this decline in prices matches nicely with the energy figures we saw yesterday that showed a surprising fall in jet fuel inventories. Prices dropped and people flew!

Moving on to “Supercore.” People made a lot last month of the m/m decline in core services ex-shelter, and they’ll make a lot of the fact that it declined m/m again this month. But that looks like a seasonal issue: last year the two softest months were also May and June. On a y/y basis, supercore showed another slight decline. Medical Care Services is 3.3% y/y, with Physicians’ and Hospital Services both holding pretty steady at a high level. I don’t see any major improvement in supercore yet.

Overall, there’s no doubting that this number is soothing for the Fed. It’s soothing for me too. Inflation is decelerating, and as I said last month I think the Fed will almost certainly deliver a token ease in the next couple of months.

The potential issue is that inflation isn’t slowing for the reason the Fed thinks it is. The economy is slowing, and unemployment is rising. I don’t know when Sahm first said it, but for decades I’ve been noting that when the Unemployment Rate rises at least 0.5% from its low, it always rises at least 1% more (here’s a time when I said it in 2011: https://inflationguy.blog/2011/07/10/no-mister-bond-i-expect-you-to-die/ ). Not that I’m bitter that it’s called the “Sahm Rule” now.

So yes, the economy is weakening and the labor market is softening. And that presages a deceleration in wage growth – or, really, a continuation in that deceleration. But the connection between wages and prices is loose at best, and that’s not why inflation will stay low, if it does. In fact, I continue to believe that median inflation will end up settling in the high 3s, low 4s. There has always been an ‘unless’ clause to that belief, but it isn’t ‘unless we enter recession.’ We will enter into one, and probably already are, but recessions and decelerations in core inflation are also only a loose relationship at best. It isn’t the recession which is causing disinflation (after all, the disinflation started long before now). What may is the slow growth in the money supply, combined with the rebound in velocity eventually running its course. We are closer to the end of the velocity rebound than to the beginning, and while M2 is accelerating it isn’t problematic yet. Those are the nascent trends to watch closely.

In the meantime – the Fed has what it wants for now. Soft employment and softening inflation. An ease will follow shortly. Whether that is followed by further eases remains to be seen, but…for now…the trends are favorable for the central bank.

Inflation Guy’s CPI Summary (Apr 2024)

The CPI for April came in pretty close to expectations. CPI came in at 0.31% m/m, and 0.29% on core, versus a priori expectations for 0.37% and 0.30%. This relative accuracy does not necessarily mean that economists now know exactly what is going on in this index, only that all of the misses canceled out. But the misses are interesting, and worth looking at, and we will do that here. Ultimately, reports like this mostly create an opportunity for framing the debate on whichever side you are on. But to my mind, this report does not meaningfully move the ball towards ‘price stability’ and leaves the Fed – if they’re being honest – still in a bind between slowing growth and sticky inflation.

Not all parts of the CPI were sticky, and that’s the point here. Actually, that has been the point for quite a while, but it was very stark in today’s report. Here’s the distribution of y/y changes in bottom-level components in the CPI. Today, the left hand stuff got lefter, the right-hand stuff got a little righter, and the middle stuff stayed about the same.

I don’t usually lead with the distribution, but it is important to keep this in mind. Inflation is not, especially at lowish levels (say, less than 5-8%), a smooth process. I used to liken this to the process of popcorn popping in a bag; the bag inflates but not because all of the kernels popped at once. The good news is that the popping is slowing, as the Fed has removed some of the heat from the bag, but the pops are still happening.

Now, here’s the good news. Thanks to core CPI being on target, the 3-month, 6-month, 9-month (well, never mind that one), and 12-month averages all decelerated.

Median inflation won’t be out for a couple of hours, but my estimate this month is 0.348% m/m, essentially unchanged from last month. That’s sort of the bad news – the y/y median CPI should be stable this month at 4.5%.

So, I think the bold type for the top line is this: inflation is decelerating, but slowly, and in a sticky fashion. The markets loved that answer and stocks and bonds leapt on the report. But that’s all framing. The debate coming into today was never about whether inflation was declining – it has been, for a while, and is expected to (even by me, and I’m on the high side of Street expectations by a fair amount) until at least Q3 and probably into Q4. That wasn’t the question – we have known since the middle of last year that 2024 would see decelerating inflation. The question is whether the deceleration will continue after that, and whether it is decelerating to 3.75%-4.25% or 1.75%-2.25%. There is as yet no sign of the latter and all signs still point to the former, because the sticky stuff is not yet unstuck.

And that continues to boil down to this: deceleration is still being driven by core goods, and resistance to that deceleration by core services.

Core goods fell to -1.3% y/y this month. I have been saying that we’ve squeezed about all we can out of core goods, and then it drops from -0.7% to -1.3%, the lowest y/y figure in 20 years! This happened even though Apparel rose 1.2% m/m. As usual, the main culprits were autos with Used Cars -1.38% m/m after -1.11% last month, and New Cars -0.45% m/m. Ironically, I think the continued softness in autos is due partly to the continued rise in motor vehicle insurance costs (which were +1.4% m/m again). We hear a lot about the affordability of housing, but you gotta have housing. You don’t gotta update your car.

The softness in core goods is welcome, naturally, but that’s the volatile part of CPI. And such low levels are only sustainable if the dollar continues to strengthen.

On the other hand, core services only softened to 5.3% y/y from 5.4%. A lot of that is housing, with OER +0.42% m/m (was +0.44% last month) and Primary Rents slowing to 0.35% from 0.41%. But outside that, ‘super core’ (core services less rent of shelter) is actually still bouncing higher. It’s 4.91% y/y – below the 6.5% it got to in late 2022, but well above the lows from October (3.75%).

Some people will like the fact that the m/m Supercore was “only” 0.42% or so, which is down from recent months. But that’s a little deceiving. Airfares were -0.81% m/m, car/truck rental -4.6%, and the monthly health insurance bump has run its course and is back to a more normal m/m change (positive, but at a 3.5% annualized rate). Longer-term, we still have to worry about the continued acceleration in, say, hospital services, which is +7.7% y/y. I pointed this out last month, and the picture is no prettier this month.

One other comment/update on rents. It is proceeding according to expectations, although I expect a slightly faster rate of deceleration for the next quarter or so. But then, all the signs are that rents are going to re-accelerate. Even those terrible indicators that inflation dummies (this includes Yellen and most of the Fed) relied on to forecast that rents would be in deflation this year…even those indicators are showing a bounce to come. Home prices are accelerating again. And none of this is surprising given that landlords are facing higher costs and increasing demand (6 million immigrants need roofs). And this is why the inflation dummies are inflation dummies – there was never, never, a good argument for why rents should be in free fall, if you just spent 10 minutes talking to an actual landlord. Get your heads out of your models and look around occasionally, dummies.

Okay, so that was a little strident but I am getting a little tired of asking potential clients how they are addressing inflation and hearing them tell me about their economist. Inflation hedging ≠ economists. Come on, people.

Let’s take this around to what we care about, and that’s policy. The Administration is trying to help the inflation figures by delaying the refilling of the Strategic Petroleum Reserve if prices go up, but is also implementing new tariffs on Chinese goods. That answers the first WWJD question (what will Joe do) – in an election year, actions which cause inflation next year are fine…just not anything which causes inflation this year. The other WWJD question (what will Jerome do) is still interesting. Growth is indeed slowing, and has been slowing for some time. Consumers are looking a bit tired, and unemployment is rising slowly. But inflation is not behaving. Median inflation won’t get below 4% until September at the earliest, and even optimistically won’t get to 3% before it starts to bounce. Before, the Fed could pretend that the new rent indicators showing widespread deflation gave it some latitude to move before the rent decreases actually arrived, but that isn’t a plausible argument any more.

However, the FOMC has started to lean more dovish. The significant decrease in the rate of taper that was announced at the last meeting clearly shows which way they are leaning. The case for a rate cut later in the summer (absent some financial crack-up that needs to be addressed) would be based on the Committee members’ sense that the current policy rate is above neutral and can be moved back towards neutral as the risks become ‘more balanced.’ Additionally, doves could argue that they don’t want to be seen easing right before the election so an ease at the end of July is a ‘down payment’ on looser policy later. The inflation data don’t support that, but the Fed doesn’t care only about inflation data. If I was on the Committee, I would not vote to loosen the taper or lower rates, but I would not be surprised to see a token ease at the end-of-July meeting. It would be cavalier, and possibly political, and not supported by the data we currently have in hand…but it wouldn’t surprise me.

One final administrative notice to those of you who subscribe to the Quarterly Inflation Outlook. The Q2 issue is expected to be published this Sunday, so look for it! (And subscribe, if you haven’t).

Rising Mortgage Origination Hints at M2 Turn

One of the successes the Federal Reserve can tout from the last couple of years (and the list of them is pretty short, to be fair) is that after the unprecedented policy actions during COVID caused never-before-seen rates of money supply expansion, subsequent policy avoided normalizing that explosion.

Year over year growth in M2 reached 26.9%. But in 2022, as the Fed started hiking rates and shrinking its balance sheet, the rate of growth slowed until M2 reached its absolute peak in July 2022 and began to slowly decline. As of today’s H6 release, year-over-year M2 has been negative for 13 months in a row.

To be sure, after a massive explosion the level of M2 has not declined all that far as the chart below shows. I also documented this fact back in November in “Where Inflation Stands in the Cycle,” which was really a good piece. You should read it.

So the success of the Fed here can be summarized by saying, ‘at least they didn’t keep blowing up the money supply.’ Since the rise in prices is clearly and closely related to the explosion in the quantity of money we have seen (anyone who still resists this obvious truism after the mountain of recent evidence is added to the prior mountain of evidence), this was a sine qua non for getting inflation back down. It isn’t sufficient, unless it’s continued for a very long time, but it’s necessary. As I illustrated in that article linked to above (which, really, you should read), there are several ways that inflation could evolve from here as the shock to the system gradually unwinds. I’ve talked before about how velocity in the policy crisis behaved as a spring or a capacitor, absorbing a lot of ‘monetary energy’ that is doomed to be released back into the system. Velocity is still rebounding (in Q4, if forecasts for Thursday’s Advance GDP report are accurate, it will rise something like 4% annualized), but if money growth remains negative then that’s really the least-painful way this can resolve. In the last chart from that prior article (have I mentioned it’s worth reading?), slack money growth with decent growth and rebounding velocity is reflected in a movement mostly to the left, with the price level not rising much. Good outcome.

However, that outcome is predicated on the notion that the money supply remains slack. If M2 starts to rise again, then the curve drifts upward and the potential set of outcomes almost certainly involve higher prices. Naturally, I’m mentioning this because of developments that make me concerned on this score.

One thing that I seriously missed in 2022 was the fact that the increase in interest rates helped bring down money supply growth. That’s not at all intuitive, because in general changing the price of a loan tends not to change the demand for a loan by very much – especially when higher inflation is making the spot real interest rate paid by the borrower lower and lower. In other words, I assert with some decent evidence that consumer and industrial loan demand is somewhat inelastic for modest changes in interest rates. Ergo, my belief was that merely raising interest rates would not necessarily cause money growth to decelerate. As it happened, I was saved from my own mistake by the fact that the Fed was also shrinking the balance sheet, which (despite the fact that reserve balances aren’t binding on banks in the current environment, so they are essentially unconstrained in lending) I thought might help money growth to decelerate. Not that I thought we’d keep getting 20% growth, but I didn’t think we would have naturally seen money growth fall below, say, 5%. Fortunately, because the Fed was also shrinking the balance sheet my forecasts were not drastically inaccurate despite being wrongly inspired, and so I forecast 5.1% median inflation for 2023 and we got 5.06%. It’s nice when the ball actually bounces your way.

As it happens, though, for the most part higher interest rates seem to have not affected loan growth very much. C&I loan growth remained strong throughout 2022 and didn’t start to level off until the Fed was just about through tightening, and consumer loans as I expected really only started to level off when the Unemployment Rate started to rise…credit cards, not at all. And that’s because, as I said, most borrowers are not borrowing because they made a NPV calculation that said borrowing makes sense; they’re borrowing because they need to and 1% or 2% or 3% doesn’t really change that calculus very much.

But you know where it did change the calculus a lot? In mortgages. And that’s because a buyer might be reluctant to pay 1% more on a mortgage, but what the buyer also needs is someone who is willing to abandon their awesome loan. As has been noted elsewhere by lots of people, home sales absolutely cratered not because people weren’t wanting to buy but because there weren’t enough people who wanted to sell. So mortgage origination volumes also dried up, as a direct consequence of higher rates. The one large market where interest rates did have a big impact, although not for the reason you’d think, was in mortgages!

You know I wouldn’t say this unless I had a neat chart to show you. Here is the Mortgage Bankers’ Association Purchase index, tracking the volume of new loans for purchasing a home (in black), set against y/y money supply growth, in blue.

Let’s tie this up with a bow:

- Higher rates didn’t affect every kind of loan, but had a big impact on turnover, and thus origination, in one very large loan market: mortgages.

- Lower mortgage origination turns out to have been uncannily correlated with money supply growth. This may or may not be causal, but it at least means that mortgage origination merits consideration as a leading indicator of money supply growth.

- As interest rates have leveled off and even declined some, the housing market is gradually adjusting. We are seeing higher home prices, and mortgage origination has been showing signs of recovering as the chart shows (mortgage origination numbers are released before sales numbers, so expect a rise in home sales coming).

- It is going to be difficult for the Fed to keep the money supply shrinking, if origination of new mortgages rises even a little bit. This doesn’t mean M2 is going to skyrocket, just that it is going to stop shrinking (in fact, it has risen each of the last two months).

- If M2 rises at even a sober 5% pace, combined with money velocity that still has some normalization left, it will be extremely difficult for the Fed to hit its inflation target on a sustainable basis for some time.

And what should you do about it, just in case? For starters, read “Inflation Sherpa.”

Summary of My Post-CPI Tweets (Oct 2023)

Below is a summary of my post-CPI tweets. You can follow me on X at @inflation_guy. Sign up for email updates to my occasional articles here. Individual and institutional investors, issuers and risk managers with interests in this area be sure to stop by Enduring Investments! Check out the Inflation Guy podcast!

- Welcome to the #CPI #inflation walkup for November (October’s figure). This is the next-to-last month I will be doing this!

- If you miss the live tweets, you can find a summary later at https://inflationguy.blog and I will podcast a summary at inflationguy.podbean.com . Those will continue in 2024 after the live tweeting stops.

- Well, this report ought to be interesting. My forecasts are very different from the other forecasts out there. The Bloomberg consensus has +0.09% on SA headline, and 0.30% on core. The swap market, Kalshi, and Cleveland Fed are all in the same ballpark.

- I have 0.14% NSA, roughly 0.22% on headline, and 0.38% on core.

- It is a little wild to me that everyone else is so low, and it makes me concerned that I’m missing something. But I think it comes down to the fact that everyone must be expecting a big give-back on OER this month.

- Used car prices should add this month. Health care insurance pivots from an 0.04% drag to an 0.02% add. Even airfares could rise, despite sliding jet fuel, because fares are too low given the level of fuel.

- All of those are in my forecast (well, I conceded flat on airfares but it could go either way). I assume they’re in everyone’s forecast. So that leads me to believe that the assumption is a correction in OER is in store.

- OK, I see the chart too. It sure LOOKS like OER did something weird last month. If OER prints 0.45% m/m instead of 0.55%, then that takes 2.5bps off my forecast. That still doesn’t get there. You need an 0.35% or something.

- And oh by the way, I’d argue that the jump might just be payback for a too-rapid fall that happened earlier this year. There was no reason to expect monthlies to drop from 0.7% m/m in Feb to 0.48% in March. Rents are not collapsing and home prices are now going back up.

- I know that’s inconvenient to the deflation story but it’s right on par with where my model says it should be. (Our model is Primary Rents but OER is based on rents).

- So okay, I’ll drop my forecast 2.5bps on the assumption we go back to 0.45% m/m for OER. Now ya happy?!? But I’m not assuming any ‘payback’.

- Meanwhile, I haven’t even talked about the fact that I have +1% on Used Cars, but that might be too conservative given how strong auctions were in the latter part of September (not picked up in the last number).

- And I don’t have anything for New Cars – but thanks to the new wage agreement, car prices both New and Used are going to go up again.

- I’ve already spoken plenty about the reversal in Health Insurance; it shouldn’t take anyone by surprise this year.

- The change in method means that the shift from -0.04% to +0.02% per month should only last six months – it shortens the lag but this transition period increases the effect to synchronize.

- With all this, Core CPI should stay at 4.1% y/y, or rise (if my forecast is on point). As I said last month, getting it below 4% is going to be more of a challenge. And Median inflation will fall to probably around 5.25% this month, but again we’re in the hard part now.

- Breakevens have net slumped a bit this month, but that hides the fact that after last month’s CPI they spiked for a week or so. 10y breaks got to 2.50% in the bond market selloff before settling back.

- If the bond bear market continues (and the balance of large government budget deficits, smaller trade deficits, and a Fed in run-off means more pressure on rates to attract domestic savers), breakevens will go back up.

- Not sure that’s a good play in Q4, since this tends to be a good seasonal time for bonds, but a bad CPI could change that. And, naturally, with a recession coming (we think?) it’ll be harder to get higher rates immediately.

- However…the secular bull market in bonds is over so the real question is whether interest rates are aimless for a decade, or in a secular bear market. Too long a topic for a tweet storm!

- So that’s it for the walkup. Pretty simple task today: 1. check OER, 2. check core ex-housing, 3. check core services ex-housing (“supercore” for a finer read on the Fed (?))

- Keep checking the improving distribution of inflation – core below median means the tails are moving to the downside, in a disinflationary signature, but not sure that will outlast 2024.

- Good luck!

- Very soft number! Let’s see how much of this is ‘payback.’

- If it’s CPI day there must be I.T. issues. It’s a law. Headline was +0.045%, Core +0.227%. Used cars was a DRAG, which is completely at odds with surveys. OER dropped to 0.41% m/m, but that by itself wouldn’t be enough for the downside surprise.

- Airfares fell, Lodging away from home fell significantly, New Cars was a marginal decline…and health insurance didn’t add as much as it was supposed to (not sure why) although it was positive. Looks like a well-rounded soft number.

- Here is m/m OER. Back to prior level, but no payback.

- In the big picture, the 3-month average isn’t all that soothing, especially when we look at Used Cars and other quirks that will likely be repaid.

- So Black Book was -1.85% in September, NSA CPI Used Cars was -5.63%. BB was +1.07% in October, NSA CPI Used Cars was -1.40%. Private auctions were strong. This is confounding – might be a seasonal quirk that BLS reflects different seasonals, but the NSA pretty far off.

- m/m CPI: 0.0449% m/m Core CPI: 0.227%

- Last 12 core CPI figures

- M/M, Y/Y, and prior Y/Y for 8 major subgroups

- Primary Rents: 7.18% y/y OER: 6.85% y/y

- Further: Primary Rents 0.5% M/M, 7.18% Y/Y (7.41% last) OER 0.41% M/M, 6.85% Y/Y (7.08% last) Lodging Away From Home -2.5% M/M, 1.2% Y/Y (7.3% last)

- Some ‘COVID’ Categories: Airfares -0.91% M/M (0.28% Last) Lodging Away from Home -2.45% M/M (3.65% Last) Used Cars/Trucks -0.8% M/M (-2.53% Last) New Cars/Trucks -0.09% M/M (0.3% Last)

- Here is my early and automated guess at Median CPI for this month: 0.359%

- Now, this is really the important thing. Median is still 0.36%. That tells you this is left-tail stuff more than the rents stuff.

- Piece 1: Food & Energy: 0.17% y/y

- Food at Home was +0.26% SA; Food Away from Home +0.37%. Food added 0.04% to headline, which was right on my forecast. Look, talk to any restaurateur – wages are still a big problem. Food AFH isn’t going to deflate soon.

- Energy was -0.22% m/m NSA; I’d estimated -0.17% so it was very slightly more drag.

- Piece 2: Core Commodities: 0.0948% y/y

- Piece 3: Core Services less Rent of Shelter: 3.71% y/y

- Piece 4: Rent of Shelter: 6.76% y/y

- Core Goods: 0.0948% y/y Core Services: 5.5% y/y

- Core goods actually ticked up slightly. Despite the decline in Used and New cars.

- This is part of the core goods story – continued acceleration in Medicinal Drugs. Honestly this is something we’ve been expecting for a long time and just surprised how long it has taken. Many of the APIs for pharma come from China.

- Core ex-housing actually ticked up very slightly from 1.97% y/y to 2.05% y/y. That sounds great but prior to COVID it hadn’t been above 2% since 2012 so that’s still too high.

- Largest declines (annualized m/m) in core were Lodging Away From Home (which is quite surprising) at -26% and Car and Truck Rental (also surprising) at -17%. Both core services but only the latter is “supercore”.

- Largest advances Motor Vehicle Insurance +26%, Tobacco +25%, Jewelry and Watches +16%.

- I am probably not going to be exactly right on median because in my calculation the median category is Northeast Urban OER, which means we’re relying on my ad-hoc seasonal adjustment. Could be as low as 0.32% m/m, or a smidge higher. Either way, it’s not price stability.

- I guess on Health Insurance I’ll have to leave the explanation to someone with a pointier pencil. My calculations had the effect being about 2bps/month; this month is was about 0.8bps. I would call that negligible except that previously it had been a 4bps drag.

- Our housing model, updated with the latest data. Kinda right on par. But notice our model never gets anywhere close to deflation in housing. Those calling for such are going to be disappointed.

- This is a strange dichotomy and I wonder if some physician can explain it. Maybe doctors are making their money by channeling expensive services through hospitals. But it’s weird to see hospital inflation so buoyant while doctors’ services are deflating.

- Education and Communication was a little soft. Some of that was a curious (to me) -0.24% NSA m/m decline in College tuition and fees. Probably a quirk. Also Telephone hardware was -1.9% m/m.

- Apparel was soft – partly this is expected because of the lagged strength of the dollar on core goods, but the -5.1% decline in Women’s outerwear seems unusual.

- The EI Inflation Diffusion Index is back almost to flat. Note that doesn’t mean 0 inflation. To get back to persistently having Median CPI around 2-3%, you’d want to see the diffusion index quite a bit negative. I think that’s going to be difficult.

- Last chart, and it tells the story. Left tail is growing, but rest of the distribution is moving left only reluctantly. The big fingers on the right are housing. It’s encouraging that there is more diversity here – a sign that the money impulse that affects everything is waning.

- Here is today’s summary. Core was surprisingly tame but it was largely from some quirky one-offs. Median didn’t improve very much. Neither Core nor Median over the last 3 months is where the Fed wants it. This doesn’t change, therefore, the higher-for-longer meme.

- It also doesn’t demand further tightening, but that’s not news. We already knew the Fed was done.

- Looking ahead, there will be further slow progress on housing, although as I keep saying – not as much as some forecasters think. The problem is that outside of housing, core inflation doesn’t look like it wants to fall much further.

- Naturally all of this depends on what the Fed does going forward. If the money supply keeps bumping along around zero growth, then eventually the velocity rebound will run its course and inflation will go back to 2-3%.

- But higher rates mean that velocity is probably going to do more than just rebound, so higher for longer will need to be longer than people expect – or, possibly, than the Fed can maintain in the face of recession.

- That’s the hard part. This so far has been the easy part. If market rates rise again in sloppy fashion after the new year, despite recession signs…what does the Fed do? Inflation won’t be at target yet, or even close. Stay tuned!

- …and thanks for staying tuned. Have a good day.