Archive

Time to Choose Your Inflation Adventure with Velocity and Money

We have CPI coming up in a few days, but M2 came out recently and it is worth commenting about, so let me drop some thoughts about the state of money and velocity right now and the context we are operating in.

M2 grew 0.88% in February, causing the y/y change to rise to 4.88% (quarterly, however, it is 6.65% annualized). I saw somebody recently observe that money growth was about 6ish back before COVID, so this level is not very worrisome to that pundit. I think that’s wrong – not that this level is worrisome in the big picture, but the trend is bad and the current level is actually not consistent with low and stable inflation as it was prior to the late twenty-‘teens.

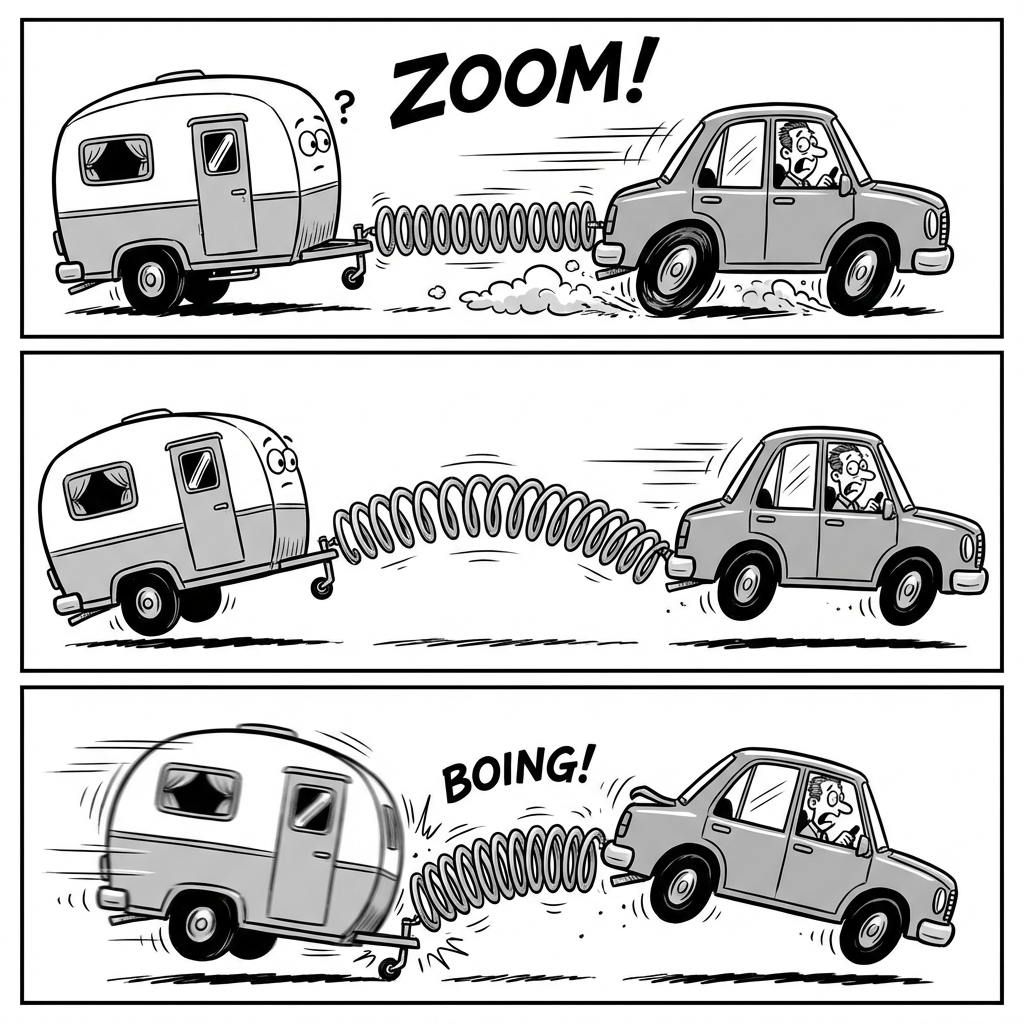

Before we get to that, let’s review the state of play for money velocity. Remember when velocity plunged early in COVID, and people said inflation wouldn’t happen because the transmission mechanism was broken? That comment was so funny it made me blow milk out of my nose, even though I wasn’t drinking milk. It was entirely an artifact of the different time frames over which the money supply was changing, compared to the time frames required for prices and output to change. MV=PQ, and M was changing suddenly. Since GDP can’t suddenly change 20%, money velocity became the capacitor that held the excess charge which slowly bled into prices. In my podcast, and occasionally in this blog, the image I shared was of a car rapidly accelerating away from a trailer hitched to it by a spring. At first, inertia keeps the trailer from traveling as fast as the car, and the spring stretches. Once the car stops accelerating, though, the spring compresses and the trailer catches up. The illustration below is courtesy of Lovart.ai.

So where are we? Here is the US monetary system over the 2019-2025 period showing total growth from December 2019. The x-axis shows the total percentage growth in money as a percentage of real output (M/Q). The y-axis shows the total change in the price level. Now, I have to point out that when I was talking about this, in 2021 or 2022, we were very far away from the diagonal line showing where the two changes are equal. And I said we would be going back to the line, and we went back to the line. People really ought to listen to me more.

The other way to look at this is that velocity is back almost to where it was prior to COVID.

So is there any problem here? Velocity is back to where it was, but if it’s stable and money is growing at 4.9% y/y, then P+Q grows at 4.9%, so 2% inflation with 3% growth…sounds pretty good.

This is where we review the “but 6% worked!” argument.

You can see from the chart that yes, since the late 1990s M2 grew at 5-10% and we never had much of an inflation problem. Why now? Well, during that period velocity was steadily declining – and that is the only way that you can sustain 6% money growth with 3% real economic growth and get 2% inflation. The question, then, was why velocity was declining. Remember, some people think this is a trend, because they don’t really understand what drives velocity. During that period, interest rates steadily declined. This was also a period of increasing globalization and a demographic dividend (more workers relative to the aged). Now, whether the interest rates declined because of those trends because both trends were disinflationary, or if interest rates declined because of a dovish Fed and they only got lucky because of those trends…I don’t know. But the point is that the largest driver of lower money velocity during that period was lower interest rates.

And interest rates are now approximately fair. Some people think they’re too low with inflation too hot, some people think they’re too high with economic growth seeming to slow, but let’s just say they’re not 300bps wrong at this point. Here is our velocity model. With lots of crazy volatility, it has velocity pretty close to on-target. Here’s the problem: the last time prior to COVID were as high as they are now (I’m looking at 5y Treasuries), it was also prior to the Global Financial Crisis and the regime of interest rate repression. Back in 2007, 5y rates were this high, and money velocity was about 2.0, some 40% higher than here. What is holding velocity down right now in our model is a very high level of economic policy uncertainty, which causes people to hold more cash than they otherwise would given the level of interest rates. Thanks to the war between the President and his allies on one side, and the minority party on the other side, not to mention the Iran war, there is a lot of uncertainty right now and that is causing people to conserve cash.

It won’t always be that way, but with M2 growing near 5%…it really needs to be that way. By the way, the money growth situation is a bit worse than it looks, too: there has in the last couple years been a fairly dramatic rise in the amount of non-M2 money that is growing in defi/crypto space. Bitcoin isn’t money, but stablecoins are very much like money. The scale of the Stablecoin money supply is small compared to the ‘off-chain’ money supply, but it is starting to get large enough to matter. Anyway, we know the sign of that growth, and it’s a big fat plus.

So no, 6% is not a stable rate of money growth going forward from here. This is not the early 2000s. It is not the 1990s. If we could manage to just have 6% growth, then we’re probably going to end up being in the mid-to-high-3s on inflation, and that’s tolerable. But if that’s the midpoint of money growth, then mid-to-high-3s is the midpoint on inflation with some periods a little below that and some periods a little above that.

Economies adapt, and an economy can work fine at 4-5% inflation or even higher as long as it is stable. But 4% inflation feels different than 2% inflation, and the economy will work differently in that sort of regime. Businesses will be more likely to pass through cost increases rather than absorb what they think are short-term variations (see “How Expecting Inflation Un-anchors Manufacturers’ Pricing Strategy”). Equilibrium equity prices are lower. Menu costs and search costs go up. And so on. We may already be seeing some of these long-term structural changes. The Fed just published a FEDS Notes entitled “Is the Inflation Process in Advanced Economies Different After the Pandemic?” The short answer? Yes it is. The question is, are we on track to get the inflation process back to the way it used to be? And the answer there appears at this juncture to be: no.

The Dollar – Best House on a Bad Block

I’m here to draw your attention to something alarming happening in currencies at the moment. Here is a picture of the US Dollar, which has lost a huge amount of value in the past year.

Now, before certain ones of you get all excited and say that this proves Trump is ruining the dollar and forcing foreigners to vamoose out of the United States, take a look at the Euro.

I’m not going to tease you too much with this. The first chart is just the dollar in terms of ounces of gold; the second is the Euro in terms of ounces of silver. Don’t worry, longtime readers: I’m not about to go all gold-bug on you. I could have done those charts with almost any currency against a wide variety of commodities: the Bloomberg Commodity Index is up 23% since mid-August, and +12% since the end of the year. So this isn’t just a precious metals story, and it isn’t just a dollar story. It’s a fiat currency vs ‘stuff’ story.

The recent breathless coverage of the melt-up in precious metals seemed to me to miss the bigger point of what it means. It’s awesome if you’re long precious metals. But the abrupt turn vertical is – or should be – alarming. But nothing looks alarming when it’s pointed higher.

Treasury Secretary Bessent, as I write this, just came out and stated that the United States has a strong dollar policy and has not intervened (at least not yet) to push the dollar lower against the yen. That’s all very nice but I don’t worry a lot about the level of the dollar against other currencies in the medium term and here’s why.

Let’s look at the monetary pipes, which to me imply an increase in the dollar and/or a sharp increase in long-term interest rates regardless of what happens to overnight policy rates. (Many people are concerned about long-term rates because of some vague sense that we are borrowing too much or because everyone is going to sell their US bonds – to buy what with the dollars they receive, no one seems to mention – but there is a mechanical/accounting relationship could cause that outcome).

To this end, the illustration below (Source: Enduring Investments[1]) is a helpful visual guide. For this analysis we are interested in the flows of the dollar system, more than its stock. And the important flows are – or have been – pretty stable. The US has for a long time run a substantial budget deficit, which means the government needs to source dollars by borrowing them. The three sources of those dollars have historically been foreign investors, the Fed, and domestic savers. Foreign investors have extra dollars because the trade deficit means that Americans send more dollars to foreign producers than foreign consumers send to US producers, and those extra dollars are invested in the US into government bonds (spigot on the lower left) or otherwise invested in markets or direct investment (spigot on the lower right). The Fed balance sheet, over the last decade or so, has often been a supplier of dollars to the system when it has been expanding more often than not. Finally, there are domestic savers who buy Treasury bonds among other things (but consider that when they’re buying US stocks, for example, the dollars are just sloshing from one domestic saver to another – that’s why there’s no flow shown for domestic savers buying US stocks). Those three ‘suppliers of dollars’ are the top hoses filling up the barrel of dollars in the illustration below.

Those flows tend to reach stasis via automatic stabilizers. For example, if the government is draining more money (with a big budget deficit) than is being supplied elsewhere, then either interest rates rise to induce domestic savers to provide more money, or the trade deficit expands. My concern is that automatic stabilizers tend to take time to stabilize, and currently there are some big changes. See the next illustration and focus on the differences compared with the prior one.

The cessation of the expansion of the Fed’s balance sheet has been happening for a while, and the balance sheet has even been shrinking a little. But the Trump Administration’s trade policies have caused two major changes: first, the trade deficit has been shrinking sharply (see charts below, source Bloomberg; the first shows the net trade balance monthly and the second shows the recent trends of declining imports and rising exports).

Some of this may be ‘payback’ for the surge in imports at the beginning of the year by importers trying to beat the imposition of tariffs, but there seems little question now that the trade deficit really is closing substantially. At the same time, foreign companies have been tripping all over each other to start making substantial investments into the US. In the second ‘barrel of money’ chart above, note the spigot at the lower right is really gushing, and two of the hoses supplying dollars have slowed to a trickle or stopped.

If that’s a fair representation, then what are the implications? If those trends persist, then the demand for dollars is going to outweigh the supply of dollars, leading to two outcomes. One of those is that in order to induce more dollars to fund the federal deficit, interest rates will have to rise. The Fed can control the policy rate, but in order to keep long-term rates down the Committee may eventually be forced to start up their hose again – intervening to buy Treasuries in the market to prevent long rates from rising, and expanding the balance sheet. The market stabilizer here would be for interest rates to rise and induce more domestic savings; if for policy reasons the Fed doesn’t want that then they’ll have to add more money themselves, with inflationary consequences. (It’s inflationary either way, but if interest rates rise it’s only indirectly inflationary in that higher interest rates also increase money velocity).

The other implication is that the dollar would strengthen on foreign exchange markets, since if foreigners are going to invest in the US in financial markets (or with direct investment, building new plants and so forth) they will need dollars to do so and the trade deficit is no longer providing a surplus of those dollars. It’s likely also that, with fewer dollars being sent abroad, domestic stock and bond markets would struggle more than they have been. A stronger dollar would be disinflationary at the margin, helping to hold down core goods prices, but this effect is fairly small…especially in the broader context I’ve mentioned, which is that all fiat currencies right now are getting smashed versus real stuff.

These are the implications of the recent large changes in financial flows. There are potential offsets available. If the trade deficit declines and the federal budget deficit declines also, it diminishes upward pressure on interest rates since domestic savers do not have to be incentivized to provide as much of the dollars in deficit. You can infer this from the barrel illustrations as well: if the federal budget moves towards balance, it lessens the net change in the system.

And there had been some positive signs on that score. The tariff revenue has been large, and some of the spending priorities of the prior Administration have been de-emphasized. These are positive developments which could lessen the pressure on the dollar and interest rates…except that the Trump Administration has been mooting the idea of ‘tariff dividend checks,’ increased defense spending, buying Greenland, and other significant spending initiatives.

It is also possible, even probable, that the Fed or Congress could change banking liquidity regulations in such a way that banks are forced to hold more Treasuries, which would add an additional hose to the top of the barrel. However, the more assets that banks are required to hold, worsening the return on assets of traditional banks, the more banking functions will start to move to non-bank entities or into crypto, increasing the money supply while decreasing the Fed’s control of it.

The upshot of all of these changes is that – based on the flows as we see them now, which could change – I believe we are going to see a significantly steeper yield curve and a significantly stronger dollar over the next few years.

Having said all of that, let me circle back to the start of this note – while the USD is not likely to collapse against other currencies, the movement against commodities (not to mention equities) and other real assets is disturbing. The US money supply has been accelerating recently; M2 is only +4.6% in the last 12 months, but that’s near (or may even be above) the maximum rate that is sustainable without causing inflation in a country that is deglobalizing and in demographic reverse. I am not bullish on gold and silver at these levels, and am more cautious on commodities than I have been in a while. But while I am a dollar bull against other currencies, I am a bear of fiat currencies against real assets generally…and I am concerned that the recent waterfall-like behavior of fiat presages a re-acceleration of CPI-style inflation. Commodities feed broadly into prices, but so do wages and lots of other things that are measured in terms of dollars. If the problem is fiat, and not gold and silver themselves, then it’s a bullish signal for inflation.

[1] These images were generated using AI image generation tools to create an illustrative representation for explanatory purposes.

The Fault, Dear Brutus, is in R*

I want to say something briefly about the “neutral rate of interest,” which has recently become grist for financial television because of new Trump-appointed Fed Governor Stephen Miran’s speech a couple of days ago in which he opined that the neutral rate of interest is much lower than the Fed believes it is, and that therefore the Fed funds target should be more like 2%-2.25% right now instead of 4.25%.

Cue the usual media clowns screaming that this is evidence of how Trump appointees do not properly respect the academic work of their presumed betters.

If that was all this is, then I would wholeheartedly support Miran’s suggestion. Most of the academic work in monetary finance is just plain wrong, or worse it’s the wrong answer to the wrong question being asked. And that’s what we have here. Anyone who thinks that Miran is an economic-denialist should read the speech. It is mostly a well-reasoned argument about all the reasons that the neutral rate may be lower now than it has been in the past. And I applaud him when he comments “I don’t want to imply more precision than I think it possible in economics.” Indeed, if we were to be honest about the degree of precision with which we measure the economy in real time and the precision of the models (even assuming they’re parameterized properly, which is questionable), the Fed would almost never be able to decisively reject the null hypothesis that nothing important has changed and therefore no rate change is required!

I can’t say that I agree with Miran’s argument though. Not because it’s wrong, but because it’s completely irrelevant.

Sometimes I think that geeks with their models is just another form of ‘boys with their toys.’ And that is what is happening here. The “neutral rate of interest” is a concept that is cousin to NAIRU, the non-accelerating-inflation rate of unemployment. The neutral rate, often called ‘r-star’ r* (which is your clue that we’re arguing about models), is the theoretical interest rate that represents perfect balance, where the economy will neither tend to generate inflation, nor tend to generate unemployment. Like I said, it’s just like NAIRU which is a level of unemployment below which inflation accelerates. And they have something else in common: they are totally unobservable.

Now, lots of things are unobservable. For example, gravity is unobservable. Yet we have a very precise estimate of the gravitational constant[1] because we can make lots of really precise measurements and work it out. Economists would love for you to think that what they’re doing with r* is similar to calibrating our estimate of the gravitational constant. It’s not remotely similar, for (at least) two enormous reasons:

- Measuring the gravitational constant is only possible because we know (as much as anything can be known) what the formula is that we are calibrating. Fg=Gm1m2/r2. So all we have to do is measure the masses, measure the distance between the centers of gravity, and infer the force from something else.[2] Then we can back into G, the gravitational constant. Here’s the thing. The theory of how interest rates affect inflation and growth, despite being ensconced in literally-weighty economics tomes, is just a theory. Actually, several different theories. And, by the way, a theory with a terrible record of actually working. To calibrate r*, the hand-waving that is being done is ‘assume that interest rates affect the economy through a James and Bartles equilibrium…’ or something like that. It is an assumption that we shouldn’t accept. And if we don’t accept it, calibrating r* is just masturbation via mathematics.[3]

- With the gravitational constant, every subsequent measurement and experiment confirms the original measurement. Every use of the model and the constant in real life, say by sending a spacecraft slingshotting around Jupiter to visit Pluto, works with ridiculous precision. On the other hand, r* has approximately a zero percent success rate in forecasting actual outcomes with anything like useful precision, and every person who measures r* gets something totally different. And r* – if it is even a real thing, which I don’t think it is – evidently moves all the time, and no one knows how. Which is Miran’s point, but the upshot is really that monetary economists should stop pretending that they know what they’re doing.

In short, we are arguing about an unmeasurable mental construct that has no useful track record of success, and we are using that mental construct to argue about whether policy rates should be at 2% or 4%. Actually, even worse, Miran says that the market rate he looks at is the 5y, 5y forward real interest rate extracted from TIPS. The Fed has nothing to do with that rate. But if that’s what he is looking at why are we arguing about overnight rates?

I should say that if there is such a thing as a ‘neutral rate’ that neither stimulates nor dampens output and inflation, I would prefer to get there by first principles. It makes sense to me that the neutral long-term real rate should be something like the long-run real growth rate of the economy. And if that’s true, then Miran is probably at least directionally accurate because as our working population levels off and shrinks, the economy’s natural growth rate declines (unless productivity conveniently surges) since output is just the product of the number of hours worked times the output per hour. But I can’t imagine that the economy ‘cares’ (if I may anthropomorphize the economy) about a 1% change in the long-run real or nominal interest rate, at least on any time scale that a monetary policymaker can operate at.

The best answer here is that whether Miran is right or not, the Fed should just pick a level of interest rates…I’m good with 3-4% at the short end…and then change its meeting schedule to once every other year.

[1] Which may in fact not be constant, but that’s a topic for someone else’s blog.

[2] In the first experiment to measure gravity, which yours truly replicated for a science fair project in high school, Henry Cavendish in 1797 figured the force in this equation by measuring the torsion force exerted by the string from which his two-mass barbell was suspended, with one of those masses attracted to another nearby mass.

[3] Yeah, I said it.

What Makes a Stable Coin Stable?

The early growth of Bitcoin and the cryptocurrency space was originally stimulated by the mistrust of centralized control of monetary policy and financial institutions. While Bitcoin is a fiat currency, in the sense that it is not ‘backed’ by anything and has value only because other people believe it has value, the rules for the expansion of the total float of Bitcoin are mechanical and so the unit benefits from being isolated from the whim of flesh-and-blood central bankers. Milton Friedman once said in an interview with the Cato Institute that “We don’t need a Fed…I have, for many years, been in favor of replacing the Fed with a computer [which would, each year] print out a specified number of paper dollars…Same number, month after month, week after week, year after year.”[1] And, with Bitcoin, that is exactly what you have. Management of Bitcoin is decentralized, automatic, and the rules are stable.

Unfortunately, ‘fiat’ cryptocurrencies are anything but stable. Moreover, since their value depends entirely on the trust[2] of other actors in the economic system that these currencies will have value, it is entirely possible that any of them could crash just like any fiat currency sometimes crashes when confidence in the currency issuer vanishes. There is no intrinsic value to a fiat currency – digital, or analog – which means that they are stable only when looked at in a self-referential frame. A US Dollar has a stable value of $1 but is volatile from the viewpoint of a Mexican-peso-based observer. I will return to this observation presently.

Because these fiat cryptos are unstable when looked at by a participant in the analog world, the concept of ‘stablecoin’ was developed. In Coinbase’s summary ‘What is a stablecoin?’, the first two bullet points are:

- Stablecoins are a type of cryptocurrency whose value is pegged to another asset, such as a fiat currency or gold, to maintain a stable price.

- They strive to provide an alternative to the high volatility of popular cryptocurrencies, making them potentially more suitable for common transactions.[3]

Why is a stable price important? The answer goes back to the question of whether Bitcoin and similar cryptos are money, or assets. In the conventional definition of money, such a label only applies to units that provide a medium of exchange, store of value, and unit of account. First-generation cryptos certainly serve as a medium of exchange but are sketchy on the ‘store of value’ and ‘unit of account’ dimensions. Nothing natively is priced in BTC, so it is not a good unit of account, and the high volatility creates a high barrier to any argument about being a store of value. Cryptos are most assuredly financial assets. It is hard to argue that they are money.

Enter the stablecoin. By pegging the value to an existing currency, a stablecoin ‘borrows’ the characteristics of that currency as a store of value and unit of account. It’s true by mathematical association: if USDC is equal to one US dollar, and the US dollar is money, then (as long as it’s accepted a medium of exchange) USDC is money because it has equal ‘store of value’ and ‘unit of account’ dimensions.[4] A stablecoin maintains its stability by means of holding reserves and being fully convertible on demand into the underlying currency.[5]

But Stable with Respect to What?

Stability, though, depends on the frame of reference. Consider a stablecoin linked to the US Dollar, which always can be minted or burned at $1 (ignoring fees). Consider a second stablecoin linked to the Japanese Yen, which always can be minted or burned at ¥1. Which one is stable?

Figure 1 – US Dollar Frame – US Dollar is stable

Figure 2 – Japanese Yen Frame – Japanese Yen is stable

The answer, of course, depends on your frame of reference. From the standpoint of someone in Japan, who is buying goods and services with Yen, a stablecoin like USDC that is linked to the dollar is most assuredly not stable in any useful sense of the word. Conversely, a US dollar investor would not find a Yen stablecoin to be stable. This, then, is an important element of defining a stablecoin: something which matches the volatility and behavior of the basis of the frame you are in, is stable with respect to you. This raises an interesting question when it comes to stablecoin regulation. A coin could very easily be regulated as a stablecoin in one jurisdiction, and not be regulated as such in a different jurisdiction – even between regulatory jurisdictions that are congruent in their treatment of most assets.

What passes for stability, in short, depends on the transactional frame – literally, the underlying currency in which transactions happen – of the observer.

Stable with Respect to When?

The meaning of stability also fluctuates with the time horizon of the observer. Fixed-income investors are very familiar with the concept of Macaulay duration, which is the future horizon at which the value of a bond holding is completely insensitive to parallel shifts in the yield curve, because the change in the value of reinvested coupons (which goes up with higher interest rates) exactly offsets the change in the value of the remaining cash flows (which go down with higher interest rates). What is the riskiness of a bond with a 7-year duration? Or more to the point of this discussion – which is riskier, a 1-month Treasury bill, or a 7-year zero coupon bond?[6]

As it turns out, it depends on the applicable horizon of the observer.

Suppose an investor pursues one of two strategies: in the first strategy, he or she buys a 1-month Treasury bill, initially at 5%, and then rolls the proceeds every month for 7 years. Alternatively, he or she could buy a 7-year zero coupon bond yielding 5%. Using a simple two-factor model with no drift, I generated 250 iterations of T-bill paths and yield curve shapes, to produce hypothetical monthly time series of returns for the two strategies. For example, here is one such random path (Figure 3):

Figure 3 – Illustrative single random path of cumulative returns for two strategies

The a priori expected return is approximately the same for both strategies; sometimes the T-bill roll strategy ends up ahead and sometimes the buy-and-hold strategy wins. With similar expected returns, a rational investor would therefore choose the one which has the lowest risk. But the riskiness or stability of the returns depends very much on the observer’s time horizon. Each of the following three charts is drawn from the same 250 Monte Carlo iterations, but the cumulative return is sampled at a different horizon. In Figure 4, the cumulative returns are sampled at the 1-month horizon. In Figure 5, the sampling is at the 3-year horizon. In Figure 6, the sampling is at the 7-year horizon. For each figure, the cumulative return for the T-bill strategy is shown on the x-axis and the cumulative return for the zero-coupon-bond buy-and-hold strategy is on the y-axis.

Figure 4 – 1-month T-Bill strategy is riskless at a 1-month horizon

Figure 5 – Both strategies are relatively risky at a 3-year horizon

Figure 6 – The 7-year zero-coupon-bond is riskless (in nominal terms) at a 7-year horizon

Although this conclusion is trivial and inevitable to fixed-income investors, the reason for our observation here is to point out that what is considered ‘stable’ not only depends on one’s functional currency but also on one’s holding period horizon.

Is the Nominal Frame the Most Important Frame?

The prior points are likely obvious to most investors. If you are investing with the intention of spending the proceeds in US Dollars, then a USD frame is most relevant. If you are investing for a known future nominal payout (for example, a life insurance company hedging scheduled annuity flows), then an investment that matures to a given value at the time when the money is needed is the most-relevant frame. However, investors sometimes lose track of one of the most important frames, and that is the “real” frame where values track the price level.

While a $1 bill is ‘stable’ in nominal terms – it will always be worth $1 – it is very unstable in purchasing-power terms.

Figure 7 – A dollar is inherently unstable in the main consumer frame

The framework where we ignore the value of the dollar, in preference for the fixed price of the dollar at $1, is the “nominal” framework. When inflation is low and stable, this frame is a useful shorthand in much the same way that when traveling abroad a tourist in the year 2000 might translate Mexican Peso prices into US Dollar prices by dividing by 10 even though the exact exchange rate differs from 10:1. In the short term, such a shortcut framework makes up for in convenience what it surrenders in precision. But in the long term, what starts out as mild imprecision becomes wildly inaccurate as the Peso exchange rate has gone from 10:1 to 20:1.

Similarly, while the nominal frame is the default for short-term comparisons it is clearly not the most important one to a consumer. Someone who is negotiating a salary at a new job, who knows he or she made $40,000 per year in 2004, would be ill-suited to use that figure as the starting point. The frame that matters over time is the real, or inflation-adjusted, frame. In the chart above, if we plotted the purchasing power of an inflation-adjusted 1983 dollar, it would be a flat line at $1.[7] On the other hand, if we plotted the nominal value of that same inflation-adjusted 1983 dollar, it would show a mostly steady increase from $1 to $3.15 over the same time period.

As before, the frame matters. A dollar that is stable in nominal space is very unstable in purchasing-power space. A unit that is stable in purchasing-power space looks unstable in nominal space.

If an investor or consumer had to choose one frame to care about, it would surely be the one in which his or her money represents not just a medium of exchange and a unit of account, but also a store of value. What this means is that a coin that is native currency and inflation-adjusted in the local price level is the most stable of stablecoins. And what that further implies is that what we currently call ‘stablecoins’ are stable only in the narrow context of being fixed at a certain nominal value of domestic currency…and that is suboptimal since all investors and consumers live in a world where prices change.

Tying Frames Together

What is interesting is that each of these frames describes “stability” in a different context. People in one frame see their own side as stable and the other side as volatile – and the exact same thing is true, in reverse, for the other side.

The various frames do traffic with each other. A holder of US Dollars (in the nominal-USD-short-term-stable frame) exchanges those dollars with a person who holds Euros (in the nominal-Euro-short-term-stable frame). We call that an exchange rate. And what ties together the nominal dollar and the inflation-linked dollar is the price index.

Figure 8 – Exchanging dollars with different purchasing power is functionally the same as exchanging currencies with different purchasing power.

In fact, the relationship between the Dollar and the Euro is so much like the relationship between the nominal dollar and the inflation-linked dollar that in 2004 Robert Jarrow and Yildiray Yildirim wrote a paper describing how to value inflation-protected securities and derivatives using a model designed for foreign exchange.[8] And that highlights the fact that an inflation-linked stablecoin isn’t some strange construct but rather an important new product to be added to the cryptocurrency universe. It is just another currency – one that is fixed in time, rather in nominal dollars, that is exchangeable to today’s dollars at the ‘inflation exchange rate’. If a 1983 dollar existed today, it could be exchanged for $3.15 current dollars because the dollar that was frozen in time in 1983 buys more than today’s dollars. That’s just an exchange rate!

Conclusion

It seems that ‘stability’ is not a stable term. Perhaps a more accurate description of the current crop of ‘stablecoins,’ which are exchangeable 1:1 with the base currency, is “fixed coins.” Only an inflation-linked coin would be a “stablecoin” in the true sense of the word, and only because being stable in purchasing-power space is the most important frame.

[1] http://www.cato.org/publications/commentary/milton-rose-friedman-offer-radical-ideas-21st-century

[2] This is not to be confused with the trustless nature of the transaction verification process of the blockchain, where the peer-to-peer nature of the process allows transactors to be certain their counterparty has the amount of bitcoin in question before completing a transaction. Rather, this is a comment on the entire system itself.

[3] https://www.coinbase.com/learn/crypto-basics/what-is-a-stablecoin

[4] Arguing that a coin pegged to gold or other commodities is a stablecoin is a bit of a stretch. Such a coin may be granted intrinsic value by such backing, and it may even be a better store of value in the long run because of such backing, but it is lacking as a unit of account (nothing is priced in gold units) and as a short-term store of value it leaves a lot to be desired.

[5] So-called ‘algorithmic stablecoins’ are mostly stable because of fiat reasons. That is, only because people believe the algorithm can guarantee that the coin is fully backed, will they behave as if they are. My usage of ‘stablecoins’ leaves out algorithmic stablecoins.

[6] I made this a zero-coupon bond to make it easier. A zero-coupon bond has a Macaulay duration equal to its maturity. However, at the 7-year horizon, any bond with a 7-year Macaulay duration has the same risk to a parallel shift of the yield curve: none. The point of this paper, though, is not fixed-income mathematics so take my word for it for the sake of this argument.

[7] Naturally, whether it is truly precisely flat depends on whether the price index we are adjusting with is an accurate representation of changes in purchasing power. Of course, such an index would look different for every person based on his or her consumption patterns so the line would not be truly flat for any person. But it would be much more stable than the non-inflation-adjusted dollar.

[8] Jarrow, Robert A. and Yildirim, Yildiray, Pricing Treasury Inflation Protected Securities and Related Derivatives Using an Hjm Model (February 1, 2011). Journal of Financial and Quantitative Analysis (JFQA), Vol. 38, No. 2, pp. 337-359, June 2003, Available at SSRN: https://ssrn.com/abstract=585828

Transcript: “What the Money Velocity Comeback Means for Inflation, and Investors”

Episode #50 of the Inflation Guy Podcast was well-received. In particular, my analogy of the car-trailer-spring system to explain why velocity is doing what it is doing garnered some strong positive feedback. Several people suggested that I publish a transcript, for those people who would prefer to read it (or who don’t know I do a podcast). What follows is a somewhat-edited version of the podcast. I took out a lot of “um” and repeat words, and the usual sorts of things that you’re embarrassed to see when you read a transcript of what you said. I tightened it up a little bit in some places and added a clarifying word here and there in brackets. But for the most part, it’s true to the original.

If you have any questions, ping me. And subscribe to the podcast, follow me on Twitter @inflation_guy (or subscribe to the private Twitter feed), or hmu to talk about how we manage money at Enduring Investments for individuals and small institutions.

Hello and welcome to Cents and Sensibility, the Inflation Guy Podcast.

I am Michael Ashton, I’m the Inflation Guy, and I’m your host. And today we have Episode 50 of The Inflation Guy Podcast and I’m going to return to money velocity because we had data out today for the fourth quarter of 2022 and there was a significant move higher in money velocity. I’ll get to that in a bit and talk about the implications that we should take away – the practical implications for what this means.

But I want to talk about this because it’s sort of become de rigueur among certain bond bulls to point at the massive drop that we had in money velocity that coincided with the massive increase in M2 during the COVID-crisis response. And those bond bulls say that velocity is permanently impaired and so the velocity plunged and it’s never gonna come back. And so it successfully blunted the importance of the massive rise in money. But we don’t have to worry about about that ever coming back. We don’t have to worry about it from now on.

This is obviously crucial to the case for lower inflation because that case basically boils down to: money growth has rapidly decelerated – it’s been negative over the last…I think it’s negative over the last 12 months now. But for a while it’s been flat to negative and so “therefore inflation will fall.”

That’s only true, though, if the sharp fall that we had in velocity is not reflected in now having a sharp rise in velocity at the same time that the sharp rise in money is being mirrored by insufficient money growth or money supply decline.

So if money…that spike now comes back and velocity plunged but doesn’t come back, then that’s the case for why we had some inflation, but not as much as the money supply spike would suggest, and now we’re going to have disinflation (or some people even say deflation – hard to believe that though).

To believe that money velocity plunged and then isn’t gonna come back, you have to believe that velocity declined for a permanent reason. But it didn’t, and that’s the bottom line here: that’s not how velocity works.

[This podcast] Episode 10 was about money velocity…and Episode 30. [Periodically in] this podcast [I have] also talked about how money velocity had turned higher last summer; at the time it was just sort of a the beginning of a turn higher. But in this quarter, the quarter just completed – the fourth quarter of 2022 – the velocity of M2 rose at an 11.4% annualized rate (which means it went up 7.3% for the whole year).

That happened, naturally, because we had money supply down while we had fourth quarter growth – real growth “Q” – that was positive, and obviously an increase in prices as well. So your PQ side of things was quite positive for the fourth quarter and M declined. And since velocity is essentially a plug number, it means velocity had to go up a lot to balance the left side of that equation, the MV=PQ equation.

Essentially, what’s really happening with velocity and the reason that velocity sort of had to come back – obviously it’s a plug number, but here’s the bottom line story of why velocity plunged. It wasn’t any permanent impairment. You should think about it this way:

You have a rapid-moving variable in in the money supply which spiked all of a sudden and you have a slower-moving variable, which is prices (because it takes time for people to change prices and for that price change to be picked up in the survey measures at the BLS and so on). And so that’s sort of like you have an automobile attached to a trailer, but instead of having a sort of a fixed rig that is attached to the trailer, you have a spring. So as the car moves away…the car goes into gear and starts to pull away. It’s moving faster than the trailer and so the spring stretches and eventually the trailer starts to move and eventually comes along. And as long as the car doesn’t continue to accelerate forever, eventually that spring will compress again and the trailer will catch up.

In fact, actually that analogy is so apt in this case, I wonder if you can’t model the whole situation with a k constant, like you would with spring physics. Because the analogy is very good. Essentially what’s happening is that, you know, money supply went zooming away and prices came along, but they came along more slowly. And so now the car is sort of sort of decelerating and the trailer (prices) is catching up to the spring, which is money velocity is starting to go back the other direction.

It’s best to think about this…and I mentioned this in the other times that I’ve talked about velocity…it’s best to think about this as being caused by (if you have to think about in terms of a cause: obviously it’s mainly a quantitative thing that sort of has to happen because we have two variables that are moving in two different paces)…it’s best to sort of think about that as being caused by precautionary demand for cash. Which is kind of what happened, right?

So, during the crisis, the government dumped tons and tons of cash into everybody’s accounts and it wasn’t spent immediately. It took some time to spend it.

So why wasn’t it spent immediately? Well, part of it was people had to figure out what to spend it on, but part of it was it was a scary time and so people figured, “well, maybe I’ll hang on to this a little while or maybe I’ll use it to pay off some debts or whatever.” It took a while for it to actually be spent until people’s financial situation got stressed enough that they had to go dip into the money that they swore they were gonna save…or what have you.

That’s the way I have modeled this is as a precautionary demand or a demand [for liquid cash] based on fear and concern about things. But the real reason is that this happened so fast, the money was flushed so fast into the system that there just was no way that prices could really respond that quickly.

Now the bottom line here is that velocity is not permanently impaired. In fact, it should rise with interest rates, as interest rates go up. And that is in fact kind of what’s happening…although I think most of what we’re seeing is this decline in the precautionary demand, but some of it is that with higher interest rates, there are more opportunities to do something other than hold cash earning zero. There’s some opportunities to take that away from true cash balances and checking balances and stuff and put it into term deposits and stuff like that.

And that means that velocity is going to come back (and it is), and that means that prices will eventually have to catch up with the car, right? The trailer eventually has to catch up with the car.

Money supply has risen since the beginning of this crisis, something around 40%, which means that prices are going to have to go up something in that neighborhood.

Actually, if velocity was unchanged over the entire length of this period and money supply only went up 40%…if you want to know how much prices are gonna go up, you have to divide the increase in money supply (that’s 40%) by the increase in GDP, whatever that turns out to be. So if GDP is up 10% then we need to see prices up an aggregate of 30%-ish or so. And so that’s sort of where I think we’re eventually going to go.

So what’s the takeaway? What does that mean, and what should you do about it?

The important takeaway is that while we are past peak inflation for now, there’s no sign that we’re going to crash back to 2% anytime soon. If in fact money velocity had not initially plunged – if velocity had been flat through this whole period – then I would be looking at the [recent] decline in the money supply growth going down to zero, and even negative, and I would say, “look, inflation should be coming down hard here; it should be going negative.” The problem is that we still haven’t had the rise in prices that you would have expected from the initial rise in money. Where that shows up is [in] that velocity plunge and [it] hasn’t come all the way back over the long haul.

The level of prices, as I said, is closely related to the level of M2 over GDP. And that’s just a consequence of the algebra of MV=PQ. So since 1990 that…well, let’s just go back further.

If you go from like 1959 to 1991, about 32 years, that relationship was super tight. M2 over that time period roughly tripled: it was up 286%. Sorry, roughly quadrupled. I’m sorry: M two divided by GDP was up 286% And the GDP deflator was up 303%. So they both roughly quadrupled over that time frame. Since 1990, that tight relationship has been less tight, which has shown up as a lot of velocity volatility.

Now, this is not irrelevant, volatility. Some of it is because there’s a changing definition of money; M2 and M1 have kind of become blurred over time. Some of that volatility is an error in measuring nominal GDP. Some of it, and maybe most of it, is excessive Fed activism on interest rate management…you know, pushing interest rates for example artificially too low since the Global Financial Crisis, which artificially depressed money velocity and so on.

But the basic relationship over a long period of time is still there. There are people out there who sort of adjust money supply in certain ways to get a better fit and I’m just I’m just not super comfortable that I know exactly the right way to do that.

I’m looking at the big picture here and I know if M2 divided by GDP goes up a lot, then we should have prices go up a lot.

Anyway, the bottom line is that inflation is not going to crash back down. We still have a lot of potential energy in the system that is pushing prices higher. And that means that market expectations of inflation are too low right now. The inflation swaps market is pricing that by June we’ll have year-on-year inflation back to 2.16%, which would just be an amazing crash back down without gasoline plunging back down. That would be truly, truly amazing. And 10 year inflation expectations, as measured by breakevens (the difference between 10 year nominal treasuries and 10 year TIPS, the difference in those yields), is 2.3% right now. That’s just crazy. Tthose expectations are just too low unless velocity’s permanently impaired.

And what that means practically for you, the investor, is that if anything you should be overweight (still) inflation hedges even though inflation is coming down from its recent peak. At the very least you should be no worse than flat – you shouldn’t be short inflation here.

You probably should be in inflation-linked bonds still rather than nominal bonds. [There are] a couple of different reasons for that, but one of them is that right now inflation-linked bonds, or [rather] the nominal bond market, is pricing inflation way too cheaply. Inflation-linked bonds will give you actual inflation and it’s likely to be higher than what’s being priced in the nominal bond market.

Real estate, commodities…all these things which are classic inflation hedges are probably still good here,even though inflation is coming down. In general, equities are not good in that kind of circumstance, but if you’re going to be in equities – and everyone tends to hold some equities – you should look for firms with pricing power. What does that mean? Hell if I know what “firms with pricing power” means exactly. Everyone thinks they have pricing power until they don’t, and they think they don’t have it until they try it and discover that they do, right?

Right now, all kinds of firms do have power to raise prices and many of them are raising prices. So it’s hard to tell which ones are the ones that will be able to keep raising prices to keep up with the input cost pressure (largely wages) that they’re going to continue to have here going forward.

Which companies have the ability to sort of stay ahead of that? I’d say in general, you’re gonna look at firms that have a lower labor content, because commodity prices have come down…or they’re going up less fast, I guess. But labor rates continue to rise rapidly and probably will for some time.

I think firms with domestic supply chains are probably better off, or at least North American supply chains, are probably better off than the ones with long international supply chains.

I think that maybe something like apartment REITS could be interesting, especially because everybody was so convinced that that real estate was going to collapse – and it’s clearly not collapsing. Rents is something that tends to keep up with wages over time. Maybe rents have gotten a little bit ahead of themselves, but I think that the decline or the deceleration in rents is probably already kind of priced into those markets.

As always, by the way, podcast musings should not be construed as recommendations.

You know, I try to avoid mentioning specific tickers all the time because I’m an advisor and that gets sticky because if you recommend, say, Tesla, [then] you have to then give all the reasons why Tesla might go down and, you know, there’s all kinds of rules about that. So I try to not spend a lot of time recommending specific securities. But you know, you can always become a client! And we can talk all about it. Or you can send me email at inflationguy@enduringinvestments.com and we can have some conversations about that, but the bottom line is that you shouldn’t be letting your guard down.

Money velocity has been coming back for a while; it’s starting to come back more seriously. Even though money supply is declining, or flat to declining, it does not mean that inflation is going to plunge back to 2% because we have this potential energy that’s still working its way through the system. There’s no sign that velocity is permanently impaired.

So, don’t let your guard down. Defend Your Money! …and if inflation is coming for you, remember: you know a guy.

The Quintillion-Dollar Coin

I was going to write a technical column today about how the sensitivity of bonds (and consequently, lots of other asset prices) to interest rates increases as interest rates decline, and discuss the implications for equity investors nowadays as interest rates head back up. That article will have to wait another week. Today, I want to just quickly dispense with a really silly idea that keeps making the rounds every time there is a standoff on the debt ceiling, pushed by the same guys who think Modern Monetary Theory (MMT) will work (even though we just tried it, and it didn’t).

The idea is that, thanks to a law passed back in the 1990s, the Treasury has the right to issue a platinum coin of any denomination. Ergo, it could produce a $1 Trillion coin, deposit it at the Federal Reserve (who does not have the option to not accept legal tender, Secretary Janet Yellen’s recently-voiced concerns notwithstanding), and continue to pay the government’s bills. Why? One well-traveled and entertaining simpleton started explaining the reasoning for doing this by saying “there’s this silly, anachronistic and ineffectual law on the books called the Debt Ceiling…”

If we started doing really really silly, not to mention stupid, things to get around every law that we thought was silly and anachronistic, legislators would be busy 24 hours a day, 7 days a week. (And, obviously, the law isn’t “ineffectual”; if it was then we wouldn’t need to get around it.)

I am continually amazed by how durable the really stupid ideas are. For instance, the notion that the government is lying about inflation to the tune of 6% per year is an idea that never seems to die even though you can show with basic math that it can’t possibly be the case. So, let’s dispense with this one even though I am sure I will have to keep slaying this dragon when it inevitably comes back from the dead.

A useful tool of logic that’s handy when you are trying to smoke out a dumb idea is to ask, “If that works, why don’t we do lots more of it?” Let’s not try to figure out why a $1 Trillion coin is a bad idea. Let’s try to figure out why a $1 Quintillion coin (a million trillions) is a bad idea.

After all, if we are going to mint a coin anyway, it doesn’t cost much more to stamp “Quinti” than it does to stamp “Tri”. And if the Treasury minted a Quintillion-dollar coin and deposited it at the Fed, it would be much more significant. With that balance, the Treasury could pay off all outstanding debt, fully fund Medicare and Social Security, and cancel all taxes basically forever while also dramatically increasing services! Why isn’t that a better idea? I spit on your Trillion-dollar coin.

Naturally, that would be a terrible idea and it’s now obvious why. I can think of several reasons, but I’ll leave most of them for other people to highlight in the comments. The immediate one is that by paying off all federal debt, increasing spending and decreasing taxes to zero, the money supply would increase immensely and immediately. As we saw quite recently, the result that rapidly follows is much higher inflation. Much much higher inflation. I will see your 8% and raise you 800%. Yes, to some extent that would depend on the Congress deciding to do that spending and cut those taxes – but do you doubt that would happen? And the Treasury offering to buy back all of the outstanding bonds wouldn’t need Congressional authorization. That’s trillions in money being suddenly returned to bondholders, which puts it back in circulation.

A trillion here, a trillion there, and pretty soon you’d be talking real money.

One Experiment Ends and Another Begins

Today the Federal Reserve hiked rates 75bps, the biggest single-meeting increase since 1994. Two days ago, the markets had incorporated an expectation for 50bps. After a well-placed Wall Street Journal article that somehow everyone on the Street knew was a warning from the Fed, the markets immediately priced 75bps. I’ve never seen anything so dramatic, nor as blatantly insider. Giving weight to a “Fed mouthpiece” journalist who is assumed to have great sources at the Fed is a time-honored tradition. But I have never seen the entire market re-price with a virtual 100% certainty overnight based on a news article (especially when the last thing the Chairman had said on the subject of 75bps was fairly dismissive, not long ago). Ergo, I’m fairly confident that the article was only the public whisper. We will never know, and they like it that way.

Cynicism aside, today marked an important moment when the central bank finally admitted that inflation is higher and likely will stay higher than they previously have assumed (gone from the statement was a note that “the Committee expects inflation to return to its 2 percent objective and the labor market to remain strong”), rates will have to go higher – although they still don’t anticipate raising rates above inflation, according to the ‘dot plot’ – and that they probably can’t make this omelette without breaking some eggs.

Powell still refused to cop to the fact that this was a total policy error, and completely identifiable in real time. It’s always amazing to me that when policymakers make massive errors they always seem to think that no one saw the mistake coming. Greenspan said that about the tech bust. Bernanke said that about the housing bust.

But this was more than just a mistake. This was an intentional policy decision that was driven by a seductive but completely idiotic theory: the idea, promulgated by Modern Monetary Theory acolytes, that if the economy is not at full employment the government can spend any amount of money and the central bank can print it, and it will not cause inflation. The last two years were an experiment, testing that proposition. Massive government spending, financed by bond sales that the Fed promptly bought, was nothing more than MMT and lots of people said so at the time, including this author. In January 2021, right after the first stimmy checks went out, I wrote this:

So I expect that as things go back to normal, inflation will rise – and probably a lot.

This is the test! Modern Monetary Theory holds you can print all you want, with no consequences, subject to certain not-really-binding constraints. The last person who offered me free wealth with no risk was a Nigerian prince, and I didn’t believe him either. I will say though that if MMT works, then we’ve been doing monetary policy wrong for a hundred years (but then, we also leached people to cure them, for hundreds of years) and all of our historical explanations are wrong – and someone will have to explain why in the past, the price level always followed the GDP-adjusted money supply.

…and I’d also said something like that in November 2020. And in March 2020. And I certainly wasn’t alone. The meme that “MMT” stood for “Magic Money Tree” was well-traveled.

So this is in no way unforeseen. The prediction in advance was that this behavior would provoke very high inflation. And the MMTers said “pshaw.” They were wrong, and that experiment is over. The next person who mentions MMT, you are entitled to run out of town on a rail.

That’s the good news. [I will say that I did not believe the Fed would get religion this quickly, but then they also haven’t been punished by asset markets yet for turning hawkish. Still, I didn’t really think the Fed would get to 1% before they’d start reversing course, and I was definitely wrong on that!]

But now the bad news. We are starting a new experiment, and unlike the last one this experiment isn’t as obvious. The Federal Reserve is now, for the first time, trying to control high inflation by changing only the price of money, with no pressure at all on the quantity of money. Always before, the Fed changed interest rates by putting pressure on reserves. Banks that wanted to continue to lend had to bid up those scarce reserves, and so interest rates rose. As I’ve written frequently (and even talked about in my book “What’s Wrong With Money?” six years ago!), that isn’t how it’s done today. Banks live in a world where lending is not reserve-constrained at all, and only capital-constrained.

Changing interest rates, without putting pressure on reserves to drag down money growth, is an experiment just like MMT was an experiment. The Fed has models. Oh yes, they have models. Gobs of models. Given what we’ve just gone through, how much confidence do you have in their models? Here’s the thing. Raising interest rates, if banks have unlimited lending power, probably[1] means more money and not less. That’s because banks are very elastic when it comes to making profitable loans. Give them more spread, or a higher yield over funding, and they will lend a bunch of money. On the other hand, borrowers tend to be less elastic. If you’re a consumer who has an 11% consumer loan, and it goes up to 12%, is that really going to make you borrow less? Mortgage origination is one place where you’d expect to see an elastic demand response to higher rates, but less than you might think when home prices are rising 15% per year. In short, if you don’t restrain banks by pressuring reserves, I suspect it’s very likely that you get more lending, not less, with higher interest rates.

But we don’t really know one way or the other.

What concerns me now is that at least with MMT, we knew it was an experiment. It may have been a stupid experiment, or merely an excuse to do ‘transformational’ things in response to the COVID recession, but we knew we were doing things we had never done before. When we talk about interest rate policy, though, there aren’t a lot of people who think the Fed is doing anything new. People think that the Fed always operates by raising interest rates, because we “know” that “tightening policy” is synonymous with rate hikes. The problem is, that’s a mental shorthand. That isn’t, in fact, the way the Fed has historically operated. When the Fed was doinking around with inflation between 1% and 3%, the precise mechanism didn’t really matter – the Fed’s actions probably didn’t have any meaningful effect one way or the other. Now, however, we are in a dreadfully important time. There’s a reason that NASA tests rockets without anyone aboard, before they strap anybody to it. We, though, are all involuntary participants in this experiment.

Hope it ends better than the last one.

[1] Fine, fine, this is speculation on my part too because I haven’t done it either. But my forecasting record is better than the Fed’s.

Money Illusion and Boiling Frogs

“Twice a day we are all forced to await the quotation of the Zurich bourse. Every fresh drop in its value [of Austrian kronen to Swiss franc) is followed by a wave of rising prices … The confidence of Austrian citizens in the currency administration of the State is shaken to its foundation. The State which is perpetually printing new banknotes deceives us with the face value … A housewife who has had no experience of the horrors of currency depreciation has no idea what a blessing stable money is, and how glorious it is to be able to buy with the note in one’s purse the article one had intended to buy at the price one had intended to pay.” – account of Frau Eisenmenger, recounted in When Money Dies (Adam Fergusson).

“Speculation on the stock exchange has spread to all ranks of the population and shares rise like air balloons to limitless heights … My banker congratulates me on every new rise, but he does not dispel the secret uneasiness which my growing wealth arouses in me … it already amounts to millions.” – Ibid.

These two passages come from the contemporaneous observations of an Austrian living through the early stages of the hyperinflation that followed WWI in that country. I don’t for a minute mean to suggest that the global economies are on the verge of hyperinflation, but I present these as an apt illustration of a concept called money illusion. In the first passage, the writer makes plain that the kronen is buying less and less, in terms of real goods, every day. Similarly, it buys less and less in terms of equity shares. The former, we tend to regard as a negative, and the latter as a positive, even though they are both related in this case to the same phenomenon: the unit of measurement is losing its value, so that it buys less real stuff as time passes. Isn’t that interesting? For someone who is continually investing in the equity market – I’m looking at you, millennials – higher prices should strike us as a bad thing just as higher car prices strike us as a bad thing.

I don’t mention that, though, to suggest that equities are a great place to hide out from inflation. In fact, they’re a pretty lousy place: as inflation rises the multiple paid on earnings declines so that even if nominal earnings are rising with inflation equity market prices can’t keep up. That’s not as bad as holding paper money and watching it go to zero, but it ends up being about the same when the inflation gets serious enough that the market itself collapses – as it did in each example of monetary hyperinflation (Germany, Austria, Zimbabwe, etc) that we have seen to date. But again, it isn’t my purpose today to warn about the dangers of treating equities like real assets when multiples are at nosebleed highs.

The interesting part is the money illusion. The writer in the passages above is uneasy, because while she is making millions she understands that those millions are losing value almost as fast (and ultimately, faster) than she can make them. But for a while the higher and higher prints of the market, the rising value of one’s home, and the accelerating increase in wages makes people feel wealthier. And wealthier people are happier and tend to spend more of the marginal wealth, when that wealth is real. But in this case the wealth is an illusion, because that additional wealth buys (at best) the same amount it did previously.

In classical economics, we would call spending more in this circumstance – despite having a similar claim to wealth in real terms – irrational. Although we use dollars to translate our labor into the things we want to buy, we all understand that we are really trading our labor for those things – it’s just that we need a medium of exchange because no one wants to directly exchange groceries for inflation-focused asset management services. More’s the pity. So homo economicus would regard his increasing millions in the market and not feel any wealthier as he knows the units of account are growing weaker. The money dropped into his bank account through a universal direct stimulus also wouldn’t be treated as actual wealth, since if we handed everyone a trillion dollars then obviously we all wouldn’t be living like trillionaires because the people who sell goods and services would adjust their prices (if they did not, then those vendors are voluntarily decreasing their own claim to the real wealth, by accepting smaller real payments in return for the same amount of goods). Wealth is just a claim on the national product. If everybody’s nominal wealth rises, but the nation is not able to produce more units of real output, then in aggregate we clearly are not wealthier because the pie is the same size. (Now, if you hand everyone a trillion dollars except for one guy, then that guy is poorer and everyone else slightly richer. Ergo, direct cash payments to the poor are clearly a way to distribute actual wealth, especially if those who don’t receive those payments also face higher taxes. So fiscal policy here definitely shuffles the deck of the wealthy. It just doesn’t make us wealthier in aggregate.)

The question of how people behave when they see additional income that comes from a greater money supply, rather than from additional productivity/output, is crucially important in monetarism. In the quantity equation of exchange, MV≡PQ, an increase in the quantity of money and in the velocity of money (MV), which is the total nominal amount of expenditures, necessarily equals the real output times the price level of that output (PQ). The amount that is spent equals the amount that is bought. But how the right side divides between P and Q is very, very important. If there is no money illusion, then an increase in the quantity of money will primarily increase prices while output will remain stable. Shopkeepers are unwilling to part with their wares for a smaller piece of the pie in real terms. On the other hand, if money illusion is rife then producers respond to consumers flush with cash by providing as many goods and services as they can; they view the masses as having more actual wealth to spend and so output increases and prices don’t rise as much.

Unfortunately, it seems that money illusion operates primarily when the quantities involved are small, or narrowly distributed. When incremental money creation is widely distributed and significant in size, then (as the second quote at the start of this article suggests) consumers, suppliers, and investors eventually figure it out. When that happens, a change in M is almost fully reflected in a change in P, as over time it usually is anyway. So the secret of recovering from a negative economic shock by expansionary monetary policy is to boil the frog slowly.

No one involved in current policy circles is interested in boiling the frog slowly. And that means it’s not going to end well.

In this context, the current bubbly stock market looks decidedly better. The chart below shows the S&P 500 divided by M2 (and multiplied by 100 because sometimes I don’t like looking at decimals on my y-axis). Now, the S&P 500 level isn’t the purest look at the total value of the equity market, but you get the general idea here – stocks have outrun the growth rate in the money supply, even over the last year, but the new records we are hitting are mostly on money vapor.

Average-Inflation Targeting, In a Nutshell

Let the bow-tie set argue about the niceties and the nuances. Here is what I can tell you about inflation targeting so that we can all understand the debate: suppose they changed the rules of baseball in an analogous way.

A new pitcher comes in to the game. He throws a pitch over the batter’s head. His next pitch skips behind the batter. His third pitch sails 2 feet high and outside. His fourth pitch almost hits the mascot.

“Yer out!” barks the umpire. Because the four pitches averaged out to strikes. My questions:

- I don’t know that the new rule gives me any greater confidence in the pitcher.

- It isn’t clear to me how that rule would help the batter.

- Maybe this helps a bad pitcher. But I wonder why a good pitcher would need that rule.

That is all.

Trust Masters, not Models

Normally, when I write about markets, I try to point at models but there is a lot of guesswork and gut-work in analysis. When times are sort of normal, then models can be a big part of what drives your thinking. But times have not been ‘normal’ for a very long time, and this is part of what drives big policy errors (and big forecasting errors): if you are out of the ‘normal’ range, then to make a forecast or comment usefully on what is going on you need to have a good feel for what the model is actually trying to capture. You need to know where the model goes wrong.

When I was a rates options trader – stop me if I’ve told this story before – I found that I preferred to use a simple Black-Scholes pricing model instead of some fancy recombining-trinomial-tree-with-heteroskedastic-volatility-model. That was because even though Black Scholes doesn’t match up super well with reality, I at least had a good feel for where it fell short. For example, the whole reason we have a volatility smile is because real-world returns have fat tails, but pricing models like Black Scholes are based on the normal distribution. When the smile flattens, it means returns are becoming more like they’re being drawn from a normal distribution; when it steepens it means that the tails are becoming fatter. So that’s easy to understand.

If you understand why an option model works, then it’s easier to think about how to price something esoteric like an option on an inflation swap (which can trade at a negative rate, but actually isn’t a rates product at all but rather is a way of trading a forward price), and not mess it up. But if you just apply and try to calibrate a bad model – especially if it’s really complicated – then you get potentially really bad outcomes. And that is, of course, exactly where we are today.

We haven’t been ‘normal’, I guess, for a couple of decades. Central banks, and in particular the Federal Reserve, have dealt in the markets with a heavier and heavier hand. Nowadays, the Fed not only has expanded its balance sheet by trillions in a very short period of time, but it has expanded the range of markets it is involved in from Treasuries to mortgages to ETFs and now individual corporate bonds. And, since the whole point of this is because the Fed wants to make sure the stock market stays elevated (they are preternaturally terrified at the notion of a wealth effect from a market crash, even though historically the wealth effect has been surprisingly small) I suspect it is only a matter of time before they directly intervene in equity markets.[1] C’est la vie. There is no normal any more.

But at least the ‘normal’ we have had over the last decade was just modestly outside of the prior normal. Things didn’t work right according to the ‘traditional’ way of thinking about things; momentum became ascendant in a way we’ve never seen before and value almost irrelevant. We are now, though, working on a whole different part of the number line. This means that economists will continue to be surprised at almost everything they see, and it means that any model you look at needs to be informed by a good intuition about how the hell it works.

So, for example, let’s consider the money supply. Over the last 13 weeks, M2 is up at a 63% annualized rate. With two weeks left in the quarter, it looks like we will end up with something like a 10.25%-10.50% growth in the money supply for the quarter. The Q2 average money supply, compared to Q1 (important in looking at the MV=PQ equation), is going to be about 13.85% higher. That’s not annualized! Remember, the old record in M2 growth for a year was a bit above 13%, in 1976.

The current NY Fed Nowcast for 2nd Quarter GDP – keeping in mind that no one has any idea, this is as good a guess as any – is -19.03%. I really like the .03 part. That’s sporty. That would mean q/q growth of -4.75%.

If we want the price deflator to come in around 1.75% (+0.44% q/q), which is where it was for the year ended in Q1, then that means money velocity needs to fall about 16% for the quarter. (1-4.75%)*(1+0.44%)/(1+13.85%)-1 = -15.97%. If money velocity falls less, and that GDP estimate is correct, then inflation comes in higher. If money velocity falls more, then inflation comes in lower. If GDP growth is actually better than -19% annualized, then inflation is lower; if GDP is worse, then inflation is higher. We don’t need to worry much about the M2 numbers themselves, as they’re almost baked in the cake at this point.

The biggest amount that money velocity has ever fallen q/q is about 5%. But clearly, these are different times! We’ve also never seen a 19% decline in growth.

Weirdly, our model has M2 money velocity for Q2 at 1.159, which would be a 15.6% decline in money velocity. Let me stress that that is a total coincidence, and I put almost zero weight on that point estimate. Contributing to that sharp decline, in our model, is the small decline in interest rates from Q1, the increase in the non-M1 part of M2, the small increase in global negative-yielding debt, and (most importantly) a large increase in precautionary demand for cash balances due to economic uncertainty. (This is why it’s hard to get velocity to stay down at this level. The current low levels depend on low interest rates, which will probably persist, but also on dramatic precautionary savings, which are unlikely to). Small changes in money velocity will have big effects on inflation: if our model estimate for velocity was right, we’d see annualized inflation for Q2 at 4.3% or so. Here’s how confident I am in our model: for Q3, it is seeing unchanged velocity (approximately), which with money trends and the GDP Nowcast figures from the NY Fed would imply that y/y inflation would rise to 6.22%, about 17.5% annualized for the quarter. Not going to happen.

Here’s where knowing a bit about the underlying process and assumptions really matters. Velocity is effectively a plug number, in that bureaucrats are good at measuring money and pretty good at measuring GDP and prices, but really bad at measuring velocity directly. So velocity is solved for. And our model (along with every other model, probably) treats the response of money velocity to the input variables as more or less instantaneous. For small changes in these variables – movements in money growth from 4% to 6%, or GDP from 2% to 0% – the assumption about instantaneity is pretty irrelevant. The economy adjusts prices easily to small changes in conditions. But that’s not true at all for big changes. On the available evidence, many prices (if not most) accelerated a bit in Q2, which surprised almost everyone including us. But no matter what the model says, prices are not going to drop 5% in a quarter, or rise 5% in a quarter, for the entire consumption basket. Price changes take time – heck, rents don’t change every month, and it takes time to rotate through the sample. Also, manufacturers don’t tend to make large changes in prices overnight, preferring to drip it in and see consumer response. But here’s the point: the model doesn’t know this. So I suspect we will see money velocity this quarter around 1.14-1.17…not because I believe our model but because I think prices will accelerate by a little bit and I think the real uncertainty surrounds the forecast of GDP. Over time, velocity and inflation will converge with our model, but it will take time.

For what it’s worth, I think that GDP growth will be a little lower than the NY Fed thinks, for a different model reason: the model assumes that changes in various economic data can be mapped to changes in GDP. But that assumes a fairly stable price level…what they’re really mapping this data onto is the nominal price level, and assuming that the price level doesn’t change enough to matter. So I think some of the dollar improvement in durable goods sales, for example, reflects rising prices and not growth, which would be manifested in a slightly lower GDP change and a slightly higher GDP deflator change.

What does this mean and why does it matter?