Archive

Inflation Guy’s CPI Summary (June 2026)

Okay, I will admit that I came into today thinking ‘this is one of the more low-stress releases in quite a while. We know headline inflation is going to be negative, and it’s just a question of whether core is 0.20% or 0.26%.’ The Bloomberg consensus was for -0.12% (seasonally adjusted) on headline CPI, and +0.23% on core CPI. That core CPI forecast would annualize to 2.8% or so, clearly indicating that inflation hadn’t fully returned to target but also not super alarming. The swap market was aligned with economists’ forecasts.

Wow, were we collectively wrong on that!

The conspiracy nuts are going to have a field day with this, even though the Federal Reserve has nothing to do with the Bureau of Labor Statistics. We get a new Fed Chairman and wham! Inflation suddenly has a sharp, surprising drop. I don’t think we need to get involved in that. There are some weird things with this number, and they all sort of got weird in the same direction, but I wouldn’t call them suspicious. However, the conspiracy nuts will point out – rightly – that there’s nothing other than gasoline that feels like its price is declining. And yet…the actual data for today showed a m/m decline in headline cpi of -0.42% and a decline in core of -0.02%.

That is a massive miss in core and the biggest decline – outside of March, April, and May 2020 – since March 2017. And in March 2017, the dip was caused by a 7% single month decline in Wireless Telephone Services, caused because the sudden shift to ‘unlimited data’ plans blew up the hedonic adjustment for data…going from 5gb to ‘infinity’ caused issues. (I wrote about that in How the BLS Methodology for Wireless Plans Exaggerated a Small Effect). Before that, January 2010 when post-housing-bubble home prices and rents were in retreat and almost turning the y/y core inflation negative (it got down to 0.6%). Before that, 1982. So, an outright decline in core CPI is rare, and especially with the overall trend firmly in the too-high-for-the-Fed zone, this is a large outlier.

The last-12-core numbers chart looks more like headline CPI than core CPI. That’s partly due to the Oct/Nov dips caused by the way the BLS handled the shutdown, and the April spike due to the payback on the rental survey. But let’s say that if you were selling straddles on core inflation, this is drastically more vol than you were pricing.

So, we go hunting for culprits. Breaking into the 8 major subcategories suggests some places to look.

A lot of the Transportation decline is of course gasoline, but the gasoline drag was pretty much spot-on what had been in the forecast. The forecasts had been looking for an 0.35% difference between headline and ex-food-and-energy CPI, and we actually had 0.40%.

One part of the explanation – as every part of a big miss on core must be – comes from rents. Primary Rents were +0.15% m/m, and OER was +0.24% m/m. Last month, those were +0.36% and +0.30%, which were not drastically far off from the current trend. But this month, the y/y decelerated again.

Airfares was +0.21% m/m; that’s a place I looked as a possible culprit since while it’s in ‘services’ these days it’s mostly a pass-through for energy and with energy dropping sharply I thought it was possible. It hasn’t happened yet, though. Lodging Away from Home was a surprising -2.32% m/m (surprising because the assumption is that the World Cup would keep it bid for another month), but LAfH moves around a lot and we can’t put it all at the feet of the hotels. Used Cars was -0.23% m/m, and New Cars -0.02% m/m, and that’s part of it too but hardly big enough to call it a major surprise.

So we continue to investigate but note that Median CPI is likely to be low also. My early estimate is +0.156% m/m, although I note that the median category is probably one of the regional OERs so I’ll be off by a little bit at least.

If that sort of Median CPI was repeated 11 more times, it would mean y/y Median CPI would be at 1.9%, well below the Fed’s target (since Median is typically above core by 0.25%-0.50%). Color me skeptical.

It’s worth noting that Core Goods inflation did not abruptly collapse. My thesis is that if the Fed’s going to get back to target, and I’m even vaguely right about housing, then you really need to see core goods to be around zero to have a good shot of getting there. And we aren’t really even sniffing it yet.

Or, alternatively, we would want to see SuperCore drop sharply. There’s no obvious sign of that, but it does bear noting that Core-Services-ex-Housing was -0.21% m/m.

That was the lowest supercore since 2020, and before that the Cell Phone Services thing in 2017.

Let’s look, since I’ve mentioned it twice now, at cell phone services.

Three things bear pointing out here. First, note the general deflation in cell phone services prices. Yeah, yeah, I know your contract hasn’t gone down in price much but you’re getting more and more quality. It’s a pretty steady trend. Second point: note that the upward divergence in 2023 almost exactly mirrors the downside divergence in 2026 before this month. The shapes are actually almost congruent. You get that frequently in a year/year rate when an item spikes in price, and then that spike falls out of the y/y. But this isn’t a year/year rate. This is an NSA price index. I can’t think of any reason for that weird phenomenon…it must be methodological somehow. Third point: this month’s spike is clearly an outlier. That doesn’t mean it isn’t real, but it does mean I don’t expect it to be repeated. For scale, note that the change is about 1.5 points on the index. The 2017 decline was 3.7 points. Odd, and I can’t explain it yet, but again: unlikely to be repeated. For what it’s worth, this is not an irrelevant weight: “Telephone Services” in the CPI carries a 1.5% weight. Thanks, “screenagers!”

I always survey the biggest-gainers and biggest-losers monthly change list, using the breakdown the Cleveland Fed uses for Median CPI. Because they are the tails, they don’t affect the median but they do affect core. This month, the biggest losers list included Lodging Away from Home (already mentioned), Jewelry and Watches (small weight), Communication (just mentioned), Infants’/Toddlers’ Apparel (small weight), and … Motor Vehicle Insurance, which declined at an annual rate of 22%. Odd?

Car insurance is 2.7% of CPI, so it is noticeable. Does this make sense? It’s possible, I suppose, because of the decline in used car prices…and, perhaps, there’s an effect from mass deportations here, since if you have fewer uninsured motorists then the cost of insurance should fall. I did not see it coming, and unlike the telephone thing I can imagine there could be some modest further declines ahead if I’m right about the causes.

So: housing, cell services, car insurance. Definitely some outliers. Rents will probably recover to get back to a more-normal run rate of +0.25%/month – after all, even with this surprise we’re right on our model.

Is it only outliers? The Enduring Investments Inflation Diffusion Index declined, so there was some narrowing of the inflation advance, but it didn’t exactly plunge. I’m going to say then that this was more the outliers than a fundamental shift of inflation momentum (at least, that’s what I think right now!)

From the Fed’s perspective…from Warsh’s perspective…this is obviously very welcome. There is little chance of any hike in US policy interest rates this year. There wasn’t much chance of it before this number either, since the new Chairman’s stated preference is for a smaller balance sheet and lower interest rates (both of which policies retard inflation, in different ways). But there is even less of a chance of a rate hike now. However, it does bear remembering that as we move later in the year, the core and median y/y numbers are going to rise, simply from base effects, and especially in October and November when the shutdown effects fall out. Ergo, it may be difficult to price out all hikes from the yield curve, unless the economy starts to visibly weaken.

Let me leave you with one last chart, to remind you that it is premature to declare victory over inflation.

M2 y/y growth is back to 5.6% y/y, and climbed at a 7% annualized rate over the last 6 months. The balance sheet has actually been growing, not shrinking, since December. Is that Powell’s last middle finger to Trump? In any event, that’s one reason that money growth is back in the range that was normal prior to COVID. But during that pre-COVID period, there were unique trends that held inflation lower than it otherwise would be: demographics and globalization being two of them. Those effects have reversed, and consequently (I’m sorry but I can’t say it often enough) a 6%ish growth in the money supply is no longer consistent with 2% inflation. Either the Fed needs to get religion (and Warsh has the hymnal open, but it’s not clear yet if anyone is going to sing along with him) and shrink the balance sheet to rein in money growth, or inflation is going to remain stubbornly resistant to a return to 2%. Phones and car insurance can’t do it all.

This Warsh Guy Might Be a Keeper

A few weeks into the Warsh Fed Chairmanship, and there are a couple of changes that I think are worth pointing out. Both are subtle, and I present them as a longtime Fed watcher and rates strategist and Inflation Guy.

The first one is something I missed at first, until I heard it again. Warsh has been talking in terms of the Federal Reserve having a 2% inflation target or goal. This may not seem like much, since central bankers routinely pledge allegiance to that goal. But over the Powell term as Chairman, that went from being something concrete to merely vacuously aspirational. First, in 2020, the Fed abandoned a 2% target and instead implemented “Flexible Average Inflation Targeting,” or FAIT. That policy said that if inflation ran below (above) the 2% target, the central bank would adjust policy to allow it to subsequently run above (below) the target for a time in order to get the average back to 2%. Now, this presumes a fine motor control over inflation that the Fed most certainly has never demonstrated, and it also conveniently left out parameters such as the averaging period. But at least it was a strategy (ambiguous, but a strategy) rather than merely a goal.

Then, in August 2025, Chairman Powell announced that the Fed was abandoning the ‘make-up’ part of the strategy. So, the Fed would still target 2%, but only as an average over time, and if inflation deviated from that average, they wouldn’t do anything about it. I wrote about it at the time in “The Fate of FAIT was Fated.” It really helped highlight the flaccidity of the Powell chairmanship.

Yet, Powell continued to talk in terms of a 2% target. In my mind, that’s just going back to an aspirational, hypothetical goal. We aren’t trying to get inflation to 2% now, mind you, just over time. Over some unspecified amount of time. And if we try to lower inflation and can’t get it down, we just re-select the averaging period, I guess. If we were at 5% for a while, so you lost a lot of real wealth, and then inflation returns to 2%…well, then a year or so later the Fed says ‘see? The average over the last year was 2%. Sorry about all that other money you were counting on. That’s never coming back.’

Anyway, so Warsh has been referring to a 2% target. It’s not clear to me in what context he means that. In the original sense of ‘we respond when it deviates from that level’? In the current sense of ‘it would be nice, but we aren’t going to take any specific actions over any specific period’? Or does he mean to reinstitute a commitment strategy so that 2% means something? I sure hope it’s the latter, and I have certainly seen some signs that Warsh is a bit sharper than the last few Fed Chairmen, but until he says so I suppose we don’t know for sure. He could do worse than to systematically dismantle everything that Powell did…

The other change is large and obvious, but there is a subtle effect that I think is being missed and should be pointed out. Under Chairman Warsh, the Fed has moved to eliminate forward guidance. The number of speeches from Fed officials is probably likely to decline as a result, since that’s the only reason anyone goes to listen to a Fed speaker.[1] I have said a huge number of times that I think more opacity from the Fed is super important in helping to squeeze excess financial risk from the system. Other folks have made the same observation, and clearly Warsh agrees with this – he frames it in terms of giving the Fed more flexibility to change course when data changes, but the only reason that opacity does that is because in the alternative case there is a disincentive to change very much lest people think the central bank – gasp! – is unable to forecast the economy very well and is being surprised a lot.

But here is what I think people have missed. It is my belief that this change is also part of the Fed’s inflation-fighting strategy. Here is the mapping of my reasoning. Less guidance obviously produces more policy uncertainty, and I just pointed out that means it is prudent to carry less financial leverage. Another way to say the same thing, but focusing on individuals rather than institutions, is that increasing policy uncertainty leads to more demand for precautionary cash balances. Institutions respond to greater uncertainty and volatility by reducing risk. Individuals respond to greater uncertainty by holding more cash, so that they can respond to the increased vicissitudes of life – job loss, for example.

And that’s important, because an increase in the demand for precautionary cash balances implies lower monetary velocity, and lower velocity means a lower price level for the same level of money and output. This is a big part of why inflation did not immediately explode when the Fed and Treasury dumped trillions of dollars of liquidity into the economy almost overnight – people were scared and held a lot of that cash for a while, rather than spending the money. As we know, velocity eventually rebounded as people spent those balances down, and inflation resulted.

As a matter of fact, Economic Policy Uncertainty is an input variable into Enduring Investments’ model for money velocity. It is not nearly as important a variable as the absolute level of interest rates, but we can reject the hypothesis of irrelevance at the 1% level and it improves the fit of the overall model so it is economically relevant as well.

Again, I don’t really know if this is part of Warsh’s master plan, or just a fortunate outcome. But luck is the residue of design. For now, I’m hopeful this is more design than luck – but I will take it, either way.

[1] It isn’t like they are at all entertaining, even to an economist. Why would you subject yourself to a Fed speech, if there is no useful forward-looking content?!

Inflation Guy’s CPI Summary (May 2026)

While the worst is probably over for the monthly CPI prints, the real question going forward is ‘how much better does it get?’ We know that energy prices will eventually retreat, but even if they merely flatline they will stop flattering headline CPI. But where does core and more importantly median CPI settle in? That’s the real question. For now, we just have one more month of data so let’s dig in.

The economist surveys had CPI at +0.51% headline and +0.27% core. The inflation swaps market was in roughly the same place, with +0.66% NSA the last trade.

The last month has seen a lot of volatility in markets (duh), but in particular a significant increase in real yields.

Nominal yields have risen a bit, and get all the ink when 30-year yields peek above 5%. That actually masks the real problem, which is that nominal yields have risen so little only due to the sharp decline in inflation expectations. In the front of the curve, that decline in breakevens is significantly a carry phenomenon (as we roll through months with solid NSA accretion) and so, therefore, is some of the rise in real yields. But a 40bps increase in real yields at the 5-year point gets one’s attention. And at 2.17%, 10-year real yields are near the absolute highs they’ve seen since the Lehman-related spike over 3% in 2008.

(Oh, and if any technician tells me this is a ‘flag’ formation projecting to 5%, I’m going to smack you. Real yields don’t go to 5%.)

The uptrend in real yields, as an aside, has also been bad for gold. Gold behaves like a long duration TIPS bond and as TIPS have sold off, gold has been a whipping boy. That won’t last forever. I like buying 10-year TIPS anywhere north of 2%, and if real yields get above 3% some day – back up the truck. Let’s hope that isn’t soon though.

The actual data comes in today at +0.473% m/m on headline CPI and +0.208% on core CPI. Both of those are below expectations, with core a meaningful miss. Here are the last 12 core CPI figures (keep in mind that last month’s jump was a payback for the 6-months-ago quirk in rents due to the government shutdown).

And here are the m/m, y/y, and prior y/y for 8 major subgroups. It’s striking that Apparel is +4.8% and “Other” is +4.9%. Those are not usually exciting categories! I’ll return to this a little later.

Here is the coarse breakdown of core goods (+1.06% y/y) and core services (+3.42%).

It isn’t surprising that core goods is decelerating. It’s actually somewhat concerning that it isn’t decelerating faster. The hook higher in core services bears some further investigation. Even though the overall numbers looked good this month, this breakdown isn’t all sunshine and roses.

Primary rents were +0.36% m/m, and 2.92% y/y versus 2.79% last month. OER was +0.3% m/m, 3.32% y/y. The jump in Rent of Primary Residence is a little concerning (although I will note that it puts the actual y/y number exactly on our model, which goes pretty flat near this level for the next year). Last month’s hook higher made sense because of that make-up month due to the shutdown/6-month lag effect. But that isn’t the issue here. Lodging Away from Home was alto +0.4% m/m, 5.2% y/y. Some people will say this is a World Cup effect, and possibly we are seeing a little bit of that in Lodging Away from Home. But this isn’t France. The US is a pretty huge country and there is no way that World Cup tourism is enough to move rents for the entire country.

But landlords are seeing higher direct and indirect costs. This is why rents are not going to go into broad deflation any time soon.

What might also be flagged as a World Cup effect, but more likely is just jet fuel pass-through, is the 2.69% m/m rise in Airfares after a 2.82% rise last month. I have airfares just slightly above the model given jet fuel prices, and within the error bars, so if there’s an impact there it’s pretty small. I think this is worse in Europe. Airfares are indeed part of the story in the core-services move higher that I noted above. Rents are too, but the airfares increase is easier to figure out.

The median category this month looks like Recreation at 3.51% annualized m/m. I may be slightly low, depending on where the regional rent indices get adjusted, but my guess for Median CPI is +0.287% m/m for a small acceleration y/y to 2.83%.

I have to say – if you shovel some of April’s jump back into October and November where it belongs – it still doesn’t look like deceleration to me.

Okay, here are the four pieces charts. Food & Energy +9.81% y/y. Core Commodities +1.06% y/y. Supercore +3.55% y/y. Rent of Shelter +3.33% y/y

The Core Services less Rent-of-Shelter (Supercore) is the one I don’t like, but again part of that is the Airfares/energy thing. None of this looks like super good news, though.

By the way, there were only 3 categories that declined at a faster annualized rate than 10% this month: Car and Truck Rental (weird) at -40% annualized, Motor Vehicle Insurance (very weird) -18%, and Misc Personal Goods -11%. Above 10%, and ignoring food and energy, we have Jewelry/Watches (41%), Misc Personal Services (28%), Communication (17%), Tobacco and Smoking Products (+13%), Infants/Toddlers Apparel (+12%). Motor Vehicle Maintenance and Repair just missed the cut at +9.95% annualized.

Here are a couple of interesting things I’m watching. This chart is Computer Software and Accessories, and it’s where AI tools land. Now, it’s a tiny, tiny part of the basket at the moment but I’ll bet it’s larger when they reweight next year. This is the NSA price index, not the rate of change – so prices for computer software and accessories are higher than they’ve been for years.

Like I said, this is a tiny category but it actually matters more for PCE. That fact annoys the Fed, who just published a research piece (https://www.federalreserve.gov/econres/notes/feds-notes/measurement-of-computer-software-and-accessories-inflation-20260522.html) explaining that this is partly ‘measurement error.’ Uh-huh. Boy are we getting picky.

Also, I happened to notice that computer prices are actually increasing, due to upward pressure on DRAM and other component prices thanks to AI demand. This sort of annoys me because I need a new laptop and the prices aren’t going down like they usually do if you wait. And yes, that’s the main reason I noticed.

This is one of those categories that animates conspiracy theorists because the BLS hedonically adjusts it…so since computers are always improving, there’s a general decline in the quality-adjusted-price over time. Well, not just a general decline, but a pretty large decline. “But computer prices haven’t actually fallen! Yes I get more computer but I don’t have the option to get the old one! I want my Windows 95!”

So prices going up, at least if it continues, is interesting. It’s a symptom of AI demand. It’s still not a large part of CPI, but I think AI is going to start showing up more here and there. Like here:

This is obviously not all AI – the upswing happened in the aftermath of COVID, possibly partly because work from home means power needs are broader throughout the day. But the continuation recently…I am pretty sure AI data center demand, if it isn’t yet affecting this, is going to!

And that is emblematic of the long-term story here. Not this month’s story per se. But these upstream pressures on petroleum and electricity are passing through more and more downstream. And that’s a hard dynamic to arrest. It is difficult to put that genie back in the bottle.

Now, this isn’t to say there is no good news.

This is Medicinal Drugs, aka pharmaceuticals, in core goods. It was -0.8% this month after -0.3% last month, and is -2.2% y/y. This looks like a real TrumpRX effect. On the other hand, Hospital Services is still rising at about 6% y/y, so while overall Medical Care in the CPI is +2.6% y/y, that’s being flattered because of the TrumpRX effect which won’t last forever.

Now, earlier I pointed out Apparel’s interesting y/y increase. The absolute price of apparel basically peaked in 1993 or so. This is a wonderful picture of the power of offshoring, as we went from producing a lot of apparel domestically to producing basically nothing, and saw apparel prices decline in real terms and even in outright terms for nearly 30 years. There was a sharp dip and recovery due to COVID, but in the last year or so the Apparel index has actually gone to new all-time highs.

Some of that is re-onshoring. Some right now is actually petroleum since many types of fibers are downstream petroleum byproducts. Think polyester, but it’s broader than that. But prices prior to the energy spike were already at 20-year highs.

The bottom line here is that the rise in the headline CPI is causing some people to shrilly declare that the Fed needs to raise rates. That’s ridiculous – the Fed looks through energy price increases. Although as I said before, those energy price increases, if they are sustained long enough, start to percolate through, and they appear to be…core and median and trimmed mean CPI won’t be heading back to target (not that there is a target any more) any time soon. As long as the economy stays pretty strong, the Fed has actually stumbled into what should be a comfortable spot for a while. Warsh will work on trimming the balance sheet, hopefully, but I wouldn’t expect rate changes for a while and that’s a change in my view from before when I thought the Fed would be easing (I thought growth would be weaker and I continue to be confounded on that). I’m saying that while the headline inflation data look ugly, that will pass as energy prices decline. But I do think it will be difficult for the Fed to get comfortable with Median CPI going back up, or just not going back down, while growth is strong.

“Mike, Mike, Mike…you’re making too much of these little things! Core doesn’t look too bad. Median is not alarming.”

Yes. But electricity, petroleum, the demographic pivot, re-onshoring, and let’s not forget money growth. These are not small things and they affect how difficult the future looks with respect to inflation. The tree’s leaves are pretty but the trunk is rotten. I am not optimistic about future shade.

Time to Choose Your Inflation Adventure with Velocity and Money

We have CPI coming up in a few days, but M2 came out recently and it is worth commenting about, so let me drop some thoughts about the state of money and velocity right now and the context we are operating in.

M2 grew 0.88% in February, causing the y/y change to rise to 4.88% (quarterly, however, it is 6.65% annualized). I saw somebody recently observe that money growth was about 6ish back before COVID, so this level is not very worrisome to that pundit. I think that’s wrong – not that this level is worrisome in the big picture, but the trend is bad and the current level is actually not consistent with low and stable inflation as it was prior to the late twenty-‘teens.

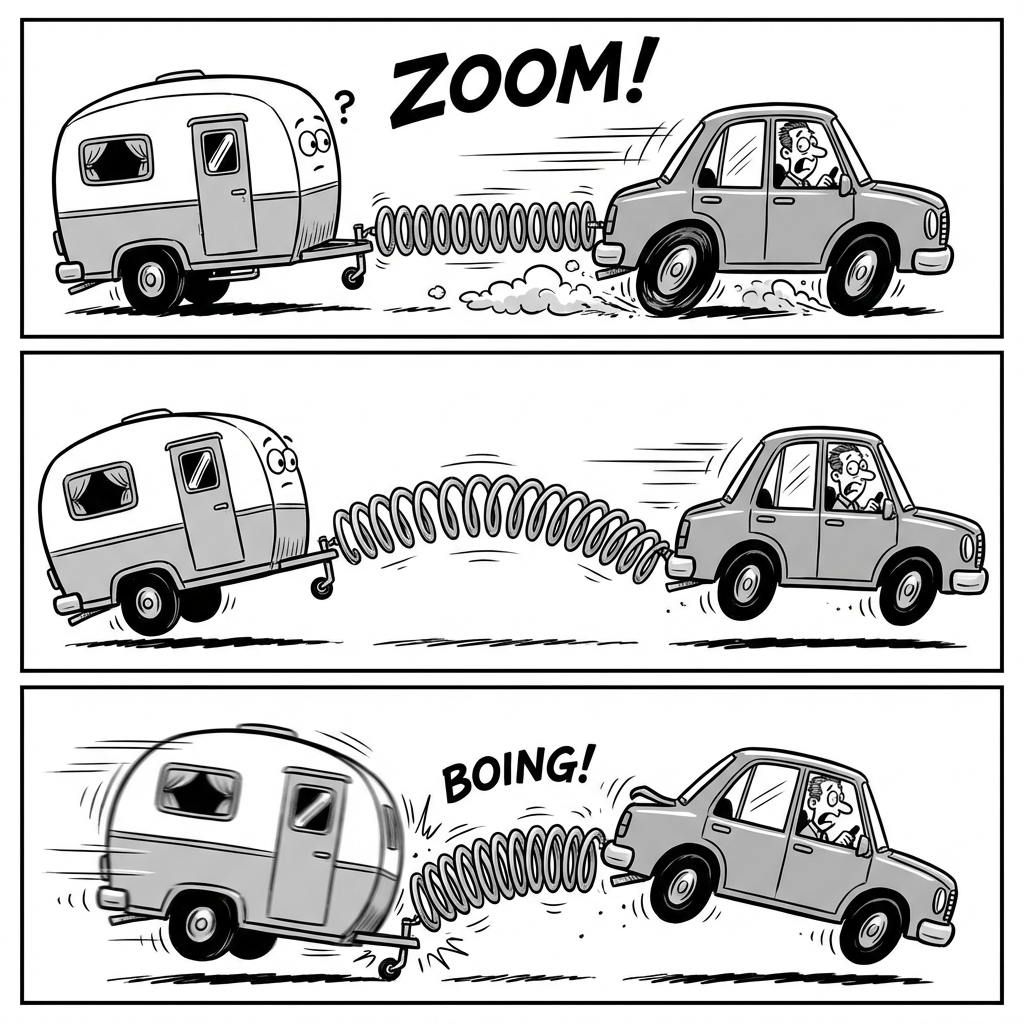

Before we get to that, let’s review the state of play for money velocity. Remember when velocity plunged early in COVID, and people said inflation wouldn’t happen because the transmission mechanism was broken? That comment was so funny it made me blow milk out of my nose, even though I wasn’t drinking milk. It was entirely an artifact of the different time frames over which the money supply was changing, compared to the time frames required for prices and output to change. MV=PQ, and M was changing suddenly. Since GDP can’t suddenly change 20%, money velocity became the capacitor that held the excess charge which slowly bled into prices. In my podcast, and occasionally in this blog, the image I shared was of a car rapidly accelerating away from a trailer hitched to it by a spring. At first, inertia keeps the trailer from traveling as fast as the car, and the spring stretches. Once the car stops accelerating, though, the spring compresses and the trailer catches up. The illustration below is courtesy of Lovart.ai.

So where are we? Here is the US monetary system over the 2019-2025 period showing total growth from December 2019. The x-axis shows the total percentage growth in money as a percentage of real output (M/Q). The y-axis shows the total change in the price level. Now, I have to point out that when I was talking about this, in 2021 or 2022, we were very far away from the diagonal line showing where the two changes are equal. And I said we would be going back to the line, and we went back to the line. People really ought to listen to me more.

The other way to look at this is that velocity is back almost to where it was prior to COVID.

So is there any problem here? Velocity is back to where it was, but if it’s stable and money is growing at 4.9% y/y, then P+Q grows at 4.9%, so 2% inflation with 3% growth…sounds pretty good.

This is where we review the “but 6% worked!” argument.

You can see from the chart that yes, since the late 1990s M2 grew at 5-10% and we never had much of an inflation problem. Why now? Well, during that period velocity was steadily declining – and that is the only way that you can sustain 6% money growth with 3% real economic growth and get 2% inflation. The question, then, was why velocity was declining. Remember, some people think this is a trend, because they don’t really understand what drives velocity. During that period, interest rates steadily declined. This was also a period of increasing globalization and a demographic dividend (more workers relative to the aged). Now, whether the interest rates declined because of those trends because both trends were disinflationary, or if interest rates declined because of a dovish Fed and they only got lucky because of those trends…I don’t know. But the point is that the largest driver of lower money velocity during that period was lower interest rates.

And interest rates are now approximately fair. Some people think they’re too low with inflation too hot, some people think they’re too high with economic growth seeming to slow, but let’s just say they’re not 300bps wrong at this point. Here is our velocity model. With lots of crazy volatility, it has velocity pretty close to on-target. Here’s the problem: the last time prior to COVID were as high as they are now (I’m looking at 5y Treasuries), it was also prior to the Global Financial Crisis and the regime of interest rate repression. Back in 2007, 5y rates were this high, and money velocity was about 2.0, some 40% higher than here. What is holding velocity down right now in our model is a very high level of economic policy uncertainty, which causes people to hold more cash than they otherwise would given the level of interest rates. Thanks to the war between the President and his allies on one side, and the minority party on the other side, not to mention the Iran war, there is a lot of uncertainty right now and that is causing people to conserve cash.

It won’t always be that way, but with M2 growing near 5%…it really needs to be that way. By the way, the money growth situation is a bit worse than it looks, too: there has in the last couple years been a fairly dramatic rise in the amount of non-M2 money that is growing in defi/crypto space. Bitcoin isn’t money, but stablecoins are very much like money. The scale of the Stablecoin money supply is small compared to the ‘off-chain’ money supply, but it is starting to get large enough to matter. Anyway, we know the sign of that growth, and it’s a big fat plus.

So no, 6% is not a stable rate of money growth going forward from here. This is not the early 2000s. It is not the 1990s. If we could manage to just have 6% growth, then we’re probably going to end up being in the mid-to-high-3s on inflation, and that’s tolerable. But if that’s the midpoint of money growth, then mid-to-high-3s is the midpoint on inflation with some periods a little below that and some periods a little above that.

Economies adapt, and an economy can work fine at 4-5% inflation or even higher as long as it is stable. But 4% inflation feels different than 2% inflation, and the economy will work differently in that sort of regime. Businesses will be more likely to pass through cost increases rather than absorb what they think are short-term variations (see “How Expecting Inflation Un-anchors Manufacturers’ Pricing Strategy”). Equilibrium equity prices are lower. Menu costs and search costs go up. And so on. We may already be seeing some of these long-term structural changes. The Fed just published a FEDS Notes entitled “Is the Inflation Process in Advanced Economies Different After the Pandemic?” The short answer? Yes it is. The question is, are we on track to get the inflation process back to the way it used to be? And the answer there appears at this juncture to be: no.

Inflation Guy’s CPI Summary (January 2026)

Let’s start by setting the context for today’s CPI number.

A couple of months ago, we missed a CPI because of the shutdown. The BLS simply didn’t have any data to calculate the October 2025 CPI. That wasn’t the real problem. The real problem was that the BLS’s handbook of methods more or less forced it, in calculating the November CPI index, to assume unchanged prices for October for some large categories – in particular, rents. This caused a large, illusory decline in y/y inflation figures. Importantly, this was also temporary – there has been some catch-up but the big one comes in a few months when the OER rent survey rotation will cause a large offsetting jump in that category, exactly six months after the illusory dip. Until then, inflation numbers will be more difficult to interpret and the year-over-year numbers will be simply wrong. So when you read that today’s figure resulted in the “smallest y/y change in core inflation since 2021, and consistent with the Fed reaching its target” – that’s just wrong. The true core y/y number is roughly 0.25%-0.3% higher than what printed today. The CPI ‘fixings’ market is currently pricing headline CPI y/y to rise to 2.82% four months from now, and that isn’t because of a coming rebound in energy prices.

I guess what I am saying is this:

Ladies and gentlemen, please take your seats. We will be experiencing some mild turbulence.

January, in general, is already a difficult month in CPI land because of the tendency for vendors of products and services to offer discounts in December and then implement annual price increases in January. But those price increases are not systematic, which means they are difficult to seasonally-adjust for. Ergo, January misses are rather the norm.

So with that context, the consensus estimates for today’s number were for +0.27% m/m on the headline CPI, and +0.31% on core. Some prognosticators were quite a bit higher than that – I think Barclays expected +0.39% on core CPI. The question was basically whether there is still any tariff increase that needs to be passed through; if so then January is a good time to do it. That didn’t really happen. The actual print was +0.17% on headline and +0.30% on core.

The miss on headline happened because while gasoline prices actually rose in January, the average price in January was lower than the average price in December – because in December, gasoline prices dropped sharply. While Jan 31 gas versus Dec 31 gas was $2.87 vs $2.833 (source AAA), January 1 vs December 1 was $2.83 vs $2.998. So, even though gasoline prices rose over the course of January compared to the end of December, that’s now how the BLS samples prices.

Be that as it may, core inflation was pretty close to target. One way to look at it is that y/y Core CPI, at 2.5%, is the lowest since March 2021. Another way to look at it is that the m/m Core was the third highest in the last year, and annualizes to 3.6%. So is it ‘mission accomplished’ for the Fed? Erm, nothing in the chart below tells me inflation is trending gently back to 2%. You?

The core number was actually flattered by a large drop in used car prices, -1.84% m/m. Used car prices actually rose in January, but less than the seasonal norm so that resulted in the large drop and that caused a meaningful drag. (Let’s not get in the habit of just dropping everything that doesn’t fit the narrative, though.) Anyway, core goods as a whole dropped to 1.1% y/y from 1.4%, while core services eased to 2.9% y/y from 3.0%.

While core goods fell more than expected because of that Used Cars number, it’s not surprising that it is moderating some. The question isn’t whether core goods prices will keep accelerating to 3% or 4%; the question is whether it stays positive, or slips back to the negative range it inhabited for many years. That’s an important story even though core goods is only 20% of the CPI. Until now it has been a ‘tariffs’ story, but going forward it’s an ‘onshoring’ story. My contention is that we should not expect a return to the persistent goods deflation that flattered CPI for a generation thanks to offshoring of manufacturing to low-labor-cost countries, because the flow is reversing. That is the story to watch, but it isn’t January 2026’s story.

While we are talking about autos, I’ll note that New Cars showed a small increase. I wonder (and I don’t have a strong forecast here) what the changes in car sales composition now that electric vehicles are no longer being pushed by the executive branch. Obviously non-electric cars are cheaper, so if we had a real-time measure of the average sales price of a car it would probably fall as consumers go back to buying cars they want instead of cars that look cheaper because of tax breaks. I don’t know though how much actual sales will change (auto production will certainly change as carmakers no longer have to check the box by making a certain number of cars that were hard to sell), and I don’t know how detailed the BLS survey is and whether it takes into account fleet composition. I guess we know that if there’s any effect, the sign should be negative. I suspect it is a small effect.

Turning to rents, as we do: Owners Equivalent Rent was +0.22% versus +0.31% last month. Rent of Primary Residence was +0.25% vs +0.27% last month. The chart below shows the m/m changes in OER… except that it does not show the 0 for October. There’s clearly a deceleration here, but my model says it should be flattening out right about at this level. Also not January 2026’s story, but it will be 2026’s story.

There was a small decline, -0.15% m/m, in Medicinal Drugs. Some folks had been eagerly waiting for that to show a large drop, thanks partly to the Trump Administration’s efforts to force drug manufacturers to align prices in the US market with prices in the ex-US market. There is not yet any discernable trend. Potentially more impactful is the Trump RX initiative, which by bringing transparency and cutting out the middleman in the really-effed-up consumer pharmaceuticals pipeline (dominated by three big wholesalers and three big pharmacy benefit managers, each of which is highly opaque about pricing) could well cause a significant decline in consumer-paid drug prices. But…remember that when those drugs are paid for by the insurance company, it isn’t a consumer expense and only shows up indirectly in the CPI. Yeah, that makes my head spin also. Bottom line: pharmaceutical prices are likely to decline some for consumers, but we just aren’t really sure where that will show up in the CPI and how soon it will happen.

The best news in the report today is the continued deceleration in core-services-ex-rents (‘Supercore’), which decelerated even with Airfares being +6.5% m/m.

Psych! You fell victim to one of the classic blunders! This is again a y/y figure that is flattered by the lack of October data. On a m/m basis, supercore had the biggest jump in a year, +0.59% (SA). Still, I think this is decelerating along with median wages deceleration. Of course, all of that data is messy right now as well, but the spread of median wages over median inflation remains right around 1%.

There is some early evidence that the downward slide in wages might be leveling off; if it does, that will limit how fast supercore can moderate. There are also some cost pressures in insurance markets that are probably going to show up in the next 6 months or so. But that’s not January 2026’s story.

The story in January 2026 is that the waters remain muddied by the government-shutdown-induced gap. The current y/y figures are all flattered by that event, and exaggerate how good the inflation picture is. That’s how the Administration can trumpet victory while the reality on the ground is that inflation is not converging to trend.

I’m working on the assumption that the Fed knows this, and the combination of core inflation that seems steady around 3.5% (abstracting from the shutdown gap), better-than-expected labor market indicators, and a distinct animus among current Fed leadership towards the President means that there’s no reason to expect an adjustment in overnight rates any time soon. Frankly, I think the argument is better for a rate increase than a rate decrease. On the other hand, rents do appear to be continuing to decelerate even if we ignore the October gap. My model says that isn’t going to continue, and even if I’m wrong I’m likely to be closer than the folks calling for deflation in housing. And moderation in Supercore is encouraging, even if – again – I don’t think that continues to the point the Fed needs it to be. Core goods inflation appears to have peaked, and the question is whether we go back to core goods deflation or not.

In each of these cases, my modeling suggests that the current level of median inflation of around 3.5% (ex-gap) is likely to end up being an equilibrium-ish level. But it isn’t ridiculous to look at the current trends and see good news on inflation. Either way, there’s not a Fed ease coming imminently. But if those trends continue until Warsh is confirmed and becomes Fed Chairman, there could be a rate cut later in the year.

But that’s not January 2026’s story.

Inflation Guy’s CPI Summary (December 2025)

Let’s start this month by remembering the absolute dumpster-fire that was last month’s CPI. The number for November was patently ridiculous on its face, and it took mere minutes to realize that the BLS was showing 2-month changes for what were essentially one-month changes:

“Because what it looks like is that for many series the BLS didn’t calculate a two-month change based on the current price level – it looks like, especially for housing, they assumed October’s change was zero so that the two-month change reported for this month was actually a one-month change spread over two months. For example, even with the low Owners’ Equivalent Rent print in September, the y/y figure was 3.76%, so about 0.31% per month. The BLS tells us that the two-month change in OER was +0.27%. That looks more than a little suspicious to me.”

That in fact was what had happened. The BLS has clearly spelled-out procedures for what happens when they cannot collect a price. If they can collect the price for other similar items, they impute the data for the uncollected price by ‘adjacent cell imputation.’ Happens all the time, and has happened more since there have been fewer data collectors, and that has upset a lot of people…but it’s no big deal. What happens less often is that the BLS can collect no similar price, or they don’t have a statistically-significant sample; in that case the BLS procedures call for the prior price to be carried forward and then the price gets naturally corrected the next time it can be gathered. I’ll talk more about this in a week or two, but if the item was generally rising in price that unchanged estimate for monthly price change will be a little low in the first month and a little high in the second month. If the item was generally getting cheaper, you’ll be a little high and then a little low when you catch up. But that’s better than taking a wild unscientific guess.

But normally, that happens for tiny categories. In this case, since no prices were collected, the BLS realized that its procedures called for carryforward pricing. After the data were released, they were very transparent about the fact that this caused understatement in the CPI, and that while most categories will be corrected by normal sampling in a month or two, the rent and OER samples will take about six months to correct because of the way those samples use overlapping six-month survey panels. You don’t need to worry about the fine details here, but to realize that the October number is missing, the November number is garbage, and the year/year numbers won’t be “right” for a while.

Ergo, take everything in today’s number, and all the charts, with a grain of salt.

A little side note is that the BLS was able to collect some data for November, when there was historical data available, so some of the series are complete. And some series have a dash (“-“) for November. Bloomberg simply omits October for those series. The practical consequence is that this is a massive mess for anyone who has built spreadsheets based on fairly normal assumptions about data structure! And it will be for a while. Anyway, on to today’s number.

Over the last month, inflation markets have been little changed.

They’re actually even more unchanged than that looks like, because the apparent rise in short-term inflation expectations is a quirk of the fact that every day, the window covered by a 1-year swap rolls forward one day, and as it turns out the day that it loses on the front end is a day when the NSA CPI was declining sharply thanks to the garbage report we just mentioned. So, the new 1-year swap has less of that garbage dragging the y/y rate down, and so it rises slightly. The net result is that inflation expectations at the front end are not really rising.

The expectations for the December CPI were for +0.31% on the seasonally-adjusted headline, with +0.32% on Core. These are even more guessy guesses than normal, since economists had to figure which categories might jump back and by how much. The actual CPI came in at +0.307% (SA) on headline CPI, and +0.239% on Core CPI. We will ignore the y/y rates for now. If we take those numbers at face value, it would annualize to 2.9% on Core CPI and 3.75% on headline CPI. That doesn’t seem wildly off, with the obvious caveat that annualizing a one-month change is stupid. Sorry.

Now, the Median CPI is going to be a snap-back sort of month. I think. The median category appears to me to be one of the regional OERs, so the actual number will depend on the seasonal adjustment the Cleveland Fed applies to that subindex. And I don’t know what the Cleveland Fed did for their last data point so they may be jumping off differently than I did. But any way you slice it, we’re going to be around 0.30-0.35% for median.

This is right about where the trend was prior to September. A word on September: while it is convenient to think that September was the ‘last good data point’ we had before the shutdown, remember that month had an outlier Owners’ Equivalent Rent number (0.14%, vs a series of 0.28%-0.40% that happened in the year prior to that) that we expected to rebound in the next month. We never saw the rebound. Median CPI was also affected by that, and so the last truly normal number was August. The upshot of it is that there may be some continued deceleration in median CPI, but it isn’t clear at all.

Core goods as of this month were +1.42% y/y. They look to be leveling off a bit, and it may be that the bump from tariffs (which, contrary to economic theory but in keeping with the way it really works, got bled into prices over a period of time rather than all at once) is petering out. Too early to tell, and part of this leveling out is due to soft Used Cars data in this month’s release. Core Services, mostly housing, continues to decelerate but see all of the caveats about rents.

And yes, rents went back to doing what they had been doing. Primary Rents were +0.26% m/m, and Owners’ Equivalent Rent was +0.31% m/m. So, yeah: that dip in OER in September was a mirage, and we’re still running at 3-4% in rents although the one-month BLS blip makes it appear that we’re still decelerating. I am not sure that’s really true.

Speaking of rents, Barclays put out a great piece earlier this week. It’s called “Apples and oranges in the CPI basket: Why market rent gauges mislead on shelter,” and if you have access to it you should read it. If you do not have access to it, you can just read my articles from the last few years. Seriously, though – it’s a very good piece and I’ll talk about it more in a week or so. But here are two of my favorite exhibits from their writeup.

Since 90% or so of rents are continuing rents, and all of the high-frequency rent indicators are recording new rents…can you see why there’s a problem?

That’s why a few years ago I migrated my model for rents to be based on a bottom-up estimate of what landlord costs were doing. Here is that model with the updated Primary Rents.

Normally, the Enduring Model has more lead time, but since part of it relies on PPI data that haven’t been released since September (and which is coming out tomorrow), the look forward is shorter than normal. Still, it says the same thing I’m saying above and approximately what Barclays is now saying – 3% on rents is about where it should be. It is not likely to decline sharply from here. And that means that getting CPI to 2% is going to depend on a collapse in goods prices or core services ex-rents, neither of which I see happening soon.

Although I should point out that core services ex-rents, aka Supercore, has been looking better of late.

As with everything else, we need to wait and see how this evolves once we get a few more months of decent data. I expect core services ex-rents to continue to decelerate a little, but that’s mainly because of Health Insurance (which fell -1.1% last month, and because of the way the Health Insurance estimate changes only once per year and gets smeared over 12 months this should work out to a drag of about 1bp/month on Core CPI). Outside of Health Insurance, the downward pressure on core services ex-rents is lessening.

And really, that’s the summary of the number: some of the effects from bad stuff (e.g. tariffs, which were never as big a deal as people treated them) are wearing off but some of the positive trends (e.g. the deceleration in rents) have also mostly run their course. The Enduring Investments Inflation Diffusion Index shows that there’s a bit of an upward trend in the distribution of accelerations/decelerations.

All of which points to the same thing I’ve been saying for a while, and that’s that once the spike was over we knew inflation would drop but it was likely to settle in the high 3s/low 4s (since amended to mid-to-high 3s). The tailwinds on inflation have turned into headwinds, so monetary policy overall needs to be tighter than it otherwise would be. The Fed doesn’t see it that way yet, and new additions to the Board of Governors are definitely more likely to be dovish than hawkish. Not only that, the federal government is also adding liquidity…or will be, if the President convinces Fannie Mae and Freddie Mac to buy $200bln in mortgages. A Federal Reserve which appreciated the inflation risks would be preparing to drain away that liquidity, no matter what it was going to do on interest rates. There’s no sign of that.

As a result: I think it’s reasonable to expect dovish outcomes from the Fed from here, although Chairman Powell will doubtless try to stick it in the eye of the President (and the American people get caught in the crossfire) before his term is up. That differs from the Fed of the last 30 years only in degree. They are going to be too loose, and there’s a good risk that inflation heads higher from here (not to 9%, mind you, but getting the sign right will matter).

Inflation Guy’s CPI Summary (November 2025)

What better way to end this crazy year than with an economic data point that we don’t know how to really interpret? Happy New Year!

Recall that, thanks to the government shutdown, the BLS released September CPI (by recalling workers to calculate the number based on data already collected) but didn’t do any of the normal price-collection procedures for the prices that are normally collected by hand. That’s far less than 100% of the index, but it’s a lot and so the October CPI was not released at all. Which brings us to today, and the November CPI – where the data was mostly collected somewhat normally. However, the calculation procedures had to be adjusted in ways we don’t really know about. You’d think that the way you do this is that you figure out the value that equates to the price level you just measured, and just say ‘hey, that’s a two-month change’ but it isn’t quite that easy. And some very smart people think this could bias the CPI lower for a few months. Whatever they end up doing, the lack of an October number is still going to mess up all the feeds (e.g. from Bloomberg) and all of the scripts and spreadsheets based on those feeds.

The BLS said in a FAQ yesterday that “November 2025 indexes were calculated by comparing November 2025 prices with October 2025 prices…BLS could not collect October 2025 reference period survey data, so survey data were carried forward to October 2025 from September 2025 in accordance with normal procedures.” In other words, November will basically be a 2-month change. (Or so we thought: see below).

Looking back to the last real data we got, in September: recall CPI was weaker than expected, but a big part of that was because of what looked like a one-off in OER. But the breadth of the basket that was accelerating was increasing, which was not a good sign. Normally the OER question would have been answered last month but…oh well.

Coming into the month…we at least have market data!

There was a big drop in short inflation swaps and breakevens this month. A lot of that is due to the steady drop in gasoline prices (see chart below), but some of it may be because sharp-penciled people anticipated that the BLS adjustment for October’s missed data is going to bias the number lower.

And boy, did it. This number is absolute garbage.

There are going to be two eras going forward: pre-shutdown inflation data and post-shutdown inflation data. Much like when there are large one-offs in the data, as in Japan years ago when there was an increase in the national sales tax rate, the year-over-year data for the next year are going to look artificially low. The BLS never adjusts the NSA data ex-post. If it’s wrong, it stays wrong. We can really hope that this doesn’t affect seasonal adjustments when the BLS calculates the new factors for next year, because that would mean next October’s CPI is going to be massively biased upwards.

Because what it looks like is that for many series the BLS didn’t calculate a two-month change based on the current price level – it looks like, especially for housing, they assumed October’s change was zero so that the two-month change reported for this month was actually a one-month change spread over two months. For example, even with the low Owners’ Equivalent Rent print in September, the y/y figure was 3.76%, so about 0.31% per month. The BLS tells us that the two-month change in OER was +0.27%. That looks more than a little suspicious to me.

Largely from that effect, core services inflation dropped from 3.5% y/y to 3.0% y/y in just two months. Riiiiight.

If in fact these two-month changes are all (or mostly) one-month changes, then the data makes a lot more sense. Either way, it’s hard to believe that the y/y change in Health Insurance dropped from 4.2% y/y to 0.57% y/y, thanks to a -2.86% decline in November from September. Yes, the Health Insurance category does not directly measure the cost of health insurance policies, and October is often when the new estimation from the BLS goes into effect, but a monthly -1.43% pre month decline for the next 12 months in Health Insurance is implausible.

Ergo, I’m not going to show most of my usual charts. This is garbage all the way down. Now, in my database instead of having a blank for October as the BLS does (for many but not all series. Seriously this is going to completely mess up any spreadsheet based on pulling data from Bloomberg), I am going to assume the price level adjusted smoothly over those two months – that is, I interpolated between September and November. That’s naïve, but it’s necessary to assume something and that’s better than assuming no change for October!

I have no idea what this will do to Median. If the Cleveland Fed follows the BLS lead, they’ll report a blank for October and a Median of something like 0.24% for the two-month period (that’s what I calculate), but it’s also garbage because garbage-in, garbage-out.

Really, this is a low point for inflation people and a low point honestly for Inflation Guy. I expected more from the BLS. I spend a lot of time defending these guys (heck, I just wrote a column on “Why Hedonic Adjustment in the CPI Shouldn’t Tick You Off”) because the staff involved in calculating the CPI are solid non-partisan professionals (aka pointy-head types) who really are trying to get as close to the ‘right’ answer as actual data allows. I can’t say that’s true in this case. Now, maybe when we get more data we will discover that the economy has abruptly shifted into something like price stability on the way to outright deflation, and it just happened to have a major inflection in October when no one was looking. But to me, it just looks like bad data.

Policymakers still gotta make policy, even if garbage data is all they have. But the correct response to not knowing what’s happening is not to assume you know what’s really happening and act accordingly – the right approach to extremely wide error bars is to do nothing. The correct approach for the Fed is to do nothing until they have another 3-6 months of data and can start getting some confidence about current trends again. That’s not the world we live in. In this world, the Fed will recognize that the inflation data is squirrelly so their behavioral response will be to ignore it and in the policy context that means that they’ll make policy for a while here based solely on the labor market. Get ready for much more market volatility around the Payrolls report again! To me, that looks like it’s likely to be an ease in two of the next three meetings, before the FOMC needs to recognize that the new inflation data is still showing 3-4% inflation. It’s possible that the Committee could take a pause while they wait for the incoming Fed Chair in May. But the inflation data will not be an impediment to an ease, and will no longer be a strong argument for holding the line if growth data looks weak.

I may be being overgenerous here. It’s also possible this will reinforce the FOMC members’ priors since many of them were utterly convinced that inflation was going to drop significantly due to housing. This, in the presence of bad data, would be a pure error. But the result is the same: an easier Fed than is healthy for the monetary system right now.

There are lots of reasons to think that yields further out the curve will stay stable or rise. But yields at the short end should probably reflect easier money going forward.

Sorry I couldn’t be more help. Here’s looking forward to 2026!

Inflation Guy’s CPI Summary (September 2025)

Well, it seems like it’s been a while since the last CPI update! Thanks to the government shutdown, it has been since this data is a week and a half later than it was scheduled to be. The importance of the CPI release is obvious, but it was reinforced by the fact it’s the only one the government is calling people back to release. It isn’t that we don’t have reasonably-accurate alternative ways to measure price pressures, though – it’s because unlike Payrolls and most other government releases that are important touchpoints for economists, the CPI is an important legal touchpoint for contracts, bonds, and legal obligations of the federal government. In this case, September’s data is a crucial number needed to calculate COLA adjustments for Social Security for next year. If this had been October’s data? I’m not sure they call back workers to release it. But that’s next month’s problem.

Speaking of next month’s problem: the government shutdown did not affect data gathering for this month’s number; they had to recall the people to collate the data and publish it but not the collectors. So the quality of the data should be fine. The data-quality question is much murkier when we look forward to next month, but since much less of the data collection is done by guys with clipboards these days, it might not be as bad as you think. Still, that will be the concern for the October CPI released next month. Like I said: next month’s problem!

Heading into the release, consensus was for +0.37% on headline CPI (SA) and +0.29% on core. I have to admit that I was confiding to people that this seemed sporty because the prior month had seen a surprising acceleration in rents that could be reversed, indications are that Used Cars would be a drag, and Food at Home also looked soft (I was right on 2 out of 3 – Food at Home was an add). That told us going in that if we were going to get to +0.29% core, either I had to be wrong on most of that or core goods ex-used cars was going to have to be pretty strong. Tariffs definitely are helping to push that narrow group of the consumption basket higher. But is that enough? Let’s see.

The backdrop going into the data was that rates have been generally softening, and the inflation swaps curve has been steepening (lessening its inversion, with near-term inflation pricing dropping more than longer-term inflation expectations). That’s consistent with a return to normalcy…but it’s really happening because energy prices have dropped quite a bit until the last couple of weeks, and that has a more immediate impact on the front of the inflation curve. The mean reversion time for energy prices is something like 15 months, so by the time you’ve gotten a few years out the curve today’s lower gasoline prices shouldn’t much affect your expectations of inflation forwards. But it affects inflation spot, which propagates through the forwards.

Actual print: SA CPI +0.31%; SA Core +0.227%. Softer than expected, and it took only a moment to see that a big part of that was due to a sharp deceleration in Owners’ Equivalent Rent (see chart). Some of that was the give-back I expected, but it was more than that and so we should put this in the back of our minds for next month – we’re probably due a reversal in the other direction over the next month or two.

Interestingly, even with the miss the Core CPI time series doesn’t look terribly weak. I mean, +0.227%, repeated for a year, still gives you 2.7% core CPI. And we won’t get downside drags from cars and housing every month.

Interesting jump in apparel this month. It’s a small category and always volatile, but since we also import almost all of our apparel it’s one place I look for tariff effects. But note the y/y numbers are still very low and in fact decelerated with this jump, implying last year’s bump in September was even larger. That’s a seasonally-adjusted figure, but I wonder if the problem here is that seasonal adjustment is failing us. Maybe pre-holiday mark-ups (from which we can show great discounts in a month!) are happening earlier. In any event it’s only 2.5% of the CPI so probably not worth too much computational cycles.

Core goods inflation rose slightly to +1.54% y/y, and core services declined to 3.47% y/y. The latter is mostly and maybe entirely due to housing, which is a core service. The former is interesting because Used Cars/Trucks was -0.41% m/m. That was expected, but it means that other core goods were more buoyant.

So here are OER and Primary Rents. 3.76% y/y (only +0.13% m/m) and 3.4% y/y (only +0.2% m/m). You can’t really tell a lot about the miss today from this chart – I showed the m/m series earlier, and the bottom line is that this continues to level out. I think the flattening is going to be more dramatic over the next 3-6 months but we’ll see. Lodging Away from Home rose again, +1.3% m/m, and is now flat y/y.

At this point, I’m thinking: with rents a downside surprise and Used Cars a downside surprise, this isn’t that bad a miss. In other words, if you’d told me we were going to get those numbers from rents and cars I would have thought core would be a lot weaker than +0.23% m/m.

Earlier I showed the last 12 Core CPIs. My guess at Median looks better, but that’s mostly because the median category is West Urban OER and even split up, an aberration in OER – and that’s what I think this is – is enough to sway Median CPI. It also means my estimate of median, +0.213% m/m, might be off because the Cleveland Fed separately estimates the seasonals for the regional OERs and so I have to guess at that part. My guess will take y/y Median CPI to 3.5% from 3.6%. And the Fed is easing. Hmm.

Here are the four-pieces charts. Food and Energy +2.99% y/y. Core Commodities +1.54%. Core Services less Rent of Shelter (Supercore) +3.37%. Rent of Shelter +3.53%. These are the four pieces that add up to CPI. None of them looks terrible except for Core Goods, and there’s limited upside to that – and it has a short period, so in a year it’s likely to be lower. I do think that going forward, core goods remains positive instead of the steady deflation it was in for decades, but not big positive. However, you need it to be negative if you want inflation at 2%, unless you get core-services-ex-rents a lot lower (but that’s highly wage-driven, and reversing illegal immigration helps support that piece somewhat) or rent of shelter a lot lower. The latter is certainly receding but it’s not going to go a lot lower.

I don’t usually spend a lot of time talking about energy, because that’s a hedgeable piece (largely – gasoline is a big part of energy and that’s easy to hedge with a little lag; electricity is harder). This month, Energy was +0.12% NSA. But next month, we’ll see a decent drag because of the sharp drop in gasoline over the last few weeks. That’s a little early compared to the usual seasonal, and it may mean we get the usual December drop in gasoline in October CPI.

Except…that I think the White House has teased that we might not get October CPI at all, just skip it, because of the difficulty gathering data. If that is true, the fallback mechanisms will kick in. See my piece on what that means, here, but the bigger point is that you wouldn’t get my scintillating commentary. I guess again that’s not this month’s problem.

Now, I have to show this almost by habit, and because the economists expecting housing deflation will be dancing in the streets. Take pictures, and show them again next year. They never learn. Housing inflation is slowing but there is no sign rents are going to come anywhere near deflation. Except maybe on a weighted basis if Mamdani gets elected Mayor of New York City and freezes rents. But then we’ll have to start looking rents ex-NYC.

How disinflationary a period are we in? Wellllll…of the item categories in the median CPI calculation, there were zero core categories that decelerated faster than 10% annualized over the last month (-0.833% or faster). On the plus side, there were Personal Care Services (+11.9% m/m annualized), Footwear (+12.0%), Motor Vehicle Fees (+14.2%), Tenants’ and Household Insurance (+15.2%), Lodging Away from Home (+17.5%), Miscellaneous Personal Goods (+17.9%), Men’s and Boys’ Apparel (+19.3%), and Public Transportation (+21.5%). These are small categories for the most part – but not all import goods and interesting in that the tails are all to the upside. That’s not the way a disinflationary economy usually looks, although I don’t want to overstate the importance of a single month!

Here’s the observation about long tails compressed into a single number, the Enduring Investments’ Inflation Diffusion Index. It’s signaling upward pressure.

Below is a chart of the overall distribution. The two big spikes in the middle are mainly rents and OER. But take those away and you can see there’s not a lot of categories in the 1-3% range, and a decent weight in the 5-6% range. This doesn’t really look like a price system settling back down placidly to 2%.

Now, the stock market clearly loves this, which makes sense. The Fed is going to ease, probably twice more this year. But that was already baked into the cake in my mind, because the Fed no longer targets 2% inflation. Remember that in the most-recent change to the 5-year operating framework the Fed, in Chairman Powell’s words, “…returned to a framework of flexible inflation targeting and eliminated the ‘makeup’ strategy.” I talk more about that here: https://inflationguy.blog/2025/09/02/the-fate-of-fait-was-fated/ Ergo, the Fed doesn’t really care if we get to 2%. They’d prefer to not see inflation head higher, but they can spin a story to themselves that even though median inflation is in the mid-to-high 3s, “the process of inflation anchoring is underway” or somesuch nonsense. As long as it’s not hitting them in the face that inflation is going up, they’ll keep relying on their models that say it should be going down. N.b., those are the same models that said inflation shouldn’t have gone up that much to begin with, and should have been transitory, but we all know “Ph.D.” stands for “Pile it higher and Deeper.”

Eventually, inflation going up probably will hit them in the face. But that’s such a 2026 problem.

The Fault, Dear Brutus, is in R*

I want to say something briefly about the “neutral rate of interest,” which has recently become grist for financial television because of new Trump-appointed Fed Governor Stephen Miran’s speech a couple of days ago in which he opined that the neutral rate of interest is much lower than the Fed believes it is, and that therefore the Fed funds target should be more like 2%-2.25% right now instead of 4.25%.

Cue the usual media clowns screaming that this is evidence of how Trump appointees do not properly respect the academic work of their presumed betters.

If that was all this is, then I would wholeheartedly support Miran’s suggestion. Most of the academic work in monetary finance is just plain wrong, or worse it’s the wrong answer to the wrong question being asked. And that’s what we have here. Anyone who thinks that Miran is an economic-denialist should read the speech. It is mostly a well-reasoned argument about all the reasons that the neutral rate may be lower now than it has been in the past. And I applaud him when he comments “I don’t want to imply more precision than I think it possible in economics.” Indeed, if we were to be honest about the degree of precision with which we measure the economy in real time and the precision of the models (even assuming they’re parameterized properly, which is questionable), the Fed would almost never be able to decisively reject the null hypothesis that nothing important has changed and therefore no rate change is required!

I can’t say that I agree with Miran’s argument though. Not because it’s wrong, but because it’s completely irrelevant.

Sometimes I think that geeks with their models is just another form of ‘boys with their toys.’ And that is what is happening here. The “neutral rate of interest” is a concept that is cousin to NAIRU, the non-accelerating-inflation rate of unemployment. The neutral rate, often called ‘r-star’ r* (which is your clue that we’re arguing about models), is the theoretical interest rate that represents perfect balance, where the economy will neither tend to generate inflation, nor tend to generate unemployment. Like I said, it’s just like NAIRU which is a level of unemployment below which inflation accelerates. And they have something else in common: they are totally unobservable.

Now, lots of things are unobservable. For example, gravity is unobservable. Yet we have a very precise estimate of the gravitational constant[1] because we can make lots of really precise measurements and work it out. Economists would love for you to think that what they’re doing with r* is similar to calibrating our estimate of the gravitational constant. It’s not remotely similar, for (at least) two enormous reasons:

- Measuring the gravitational constant is only possible because we know (as much as anything can be known) what the formula is that we are calibrating. Fg=Gm1m2/r2. So all we have to do is measure the masses, measure the distance between the centers of gravity, and infer the force from something else.[2] Then we can back into G, the gravitational constant. Here’s the thing. The theory of how interest rates affect inflation and growth, despite being ensconced in literally-weighty economics tomes, is just a theory. Actually, several different theories. And, by the way, a theory with a terrible record of actually working. To calibrate r*, the hand-waving that is being done is ‘assume that interest rates affect the economy through a James and Bartles equilibrium…’ or something like that. It is an assumption that we shouldn’t accept. And if we don’t accept it, calibrating r* is just masturbation via mathematics.[3]

- With the gravitational constant, every subsequent measurement and experiment confirms the original measurement. Every use of the model and the constant in real life, say by sending a spacecraft slingshotting around Jupiter to visit Pluto, works with ridiculous precision. On the other hand, r* has approximately a zero percent success rate in forecasting actual outcomes with anything like useful precision, and every person who measures r* gets something totally different. And r* – if it is even a real thing, which I don’t think it is – evidently moves all the time, and no one knows how. Which is Miran’s point, but the upshot is really that monetary economists should stop pretending that they know what they’re doing.

In short, we are arguing about an unmeasurable mental construct that has no useful track record of success, and we are using that mental construct to argue about whether policy rates should be at 2% or 4%. Actually, even worse, Miran says that the market rate he looks at is the 5y, 5y forward real interest rate extracted from TIPS. The Fed has nothing to do with that rate. But if that’s what he is looking at why are we arguing about overnight rates?

I should say that if there is such a thing as a ‘neutral rate’ that neither stimulates nor dampens output and inflation, I would prefer to get there by first principles. It makes sense to me that the neutral long-term real rate should be something like the long-run real growth rate of the economy. And if that’s true, then Miran is probably at least directionally accurate because as our working population levels off and shrinks, the economy’s natural growth rate declines (unless productivity conveniently surges) since output is just the product of the number of hours worked times the output per hour. But I can’t imagine that the economy ‘cares’ (if I may anthropomorphize the economy) about a 1% change in the long-run real or nominal interest rate, at least on any time scale that a monetary policymaker can operate at.

The best answer here is that whether Miran is right or not, the Fed should just pick a level of interest rates…I’m good with 3-4% at the short end…and then change its meeting schedule to once every other year.

[1] Which may in fact not be constant, but that’s a topic for someone else’s blog.

[2] In the first experiment to measure gravity, which yours truly replicated for a science fair project in high school, Henry Cavendish in 1797 figured the force in this equation by measuring the torsion force exerted by the string from which his two-mass barbell was suspended, with one of those masses attracted to another nearby mass.

[3] Yeah, I said it.

Inflation Guy’s CPI Summary (August 2025)

Before I begin talking about today’s CPI, a quick word about the 24th anniversary of the terrorist attacks of 9/11. As someone who worked 1 block from the Towers, I can tell you it’s a day I will never forget and filled with images I can never erase. But I also remember that in the weeks that followed, the country was unified in a way I’d never seen. Rudy Giuliani was “America’s Mayor” for his courage and steady hand during the disaster and in the period that followed. When I traveled to the Midwest, menus were filled with ‘Freedom Fries’ and strangers asked with concern about my family and friends when they heard I was from New York. It seems crazy to me that only 24 years removed from that, the country is divided in a way I’ve never seen. Everyone said “we will never forget.” And then they forgot.

But I do not forget. I give prayers and thanks for the brave first responders I saw that day and for the families of those who didn’t return. And you should too.

All of which makes the monthly CPI report seem very small. In truth, it is small all of a sudden. From being one of the most-important releases for a couple of years because of the Fed’s assumed reaction function, it has abruptly been pushed to the back. This is partly because of the weak Employment data and the massive downward revisions to the prior data but that point is reinforced by the Fed’s recent adjustment to the inflation targeting framework, in which they removed any imperative to make up for periods of high inflation by engineering lower inflation so that the reaction function is basically one way. (See my writeup on this at https://inflationguy.blog/2025/09/02/the-fate-of-fait-was-fated/.) I guess there’s an ironic parallelism here. After the inflationary 1970s and the pain of bringing inflation back down, the Fed said “we will never forget.” And then they forgot.

But I do not forget. And neither should you. An investor’s nominal returns are irrelevant (except to the IRS). What matters is real returns, and a period of higher and less-stable inflation has historically resulted in lower asset prices since the most important indicator of future returns over normal investing horizons is starting price. If markets need to adjust to higher inflation to give higher nominal returns, the easiest way to do that is to lower the starting price. So whether the Fed cares, we should.

And with that – we came into today with real yields having fallen some 20bps this month, but with inflation expectations having not declined much at all. Obviously, that’s the market’s reaction to the presumed tilt of the Fed.

The CPI report was slightly above expectations, which were already somewhat higher than in prior months. So when people tell you this was a ‘small miss higher,’ that’s mainly because economists adjusted their expectations, not because the number was similar to prior months. Month/month headline inflation (seasonally adjusted) was +0.382% (expectations were +0.33%), with core at +0.346% (expectations were +0.31%). Markets have not reacted poorly to this figure, but I wonder if core had been slightly higher and rounded to +0.4% if we’d have seen more introspection.

But as I said, this is a ‘small miss’ but that does not mean it was a small number. Indeed, with the exception of the jump in January associated with tariff noise, this is the highest core figure in 17 months.

There were a number of upside categories, but one of them was not Medical Care. Some people had been looking for a move higher here, and Doctor’s Services rose a bit, but Medicinal Drugs fell -0.372% m/m and is now down year/year. That surprises me, but there are a lot of pressures on the drug industry right now and it is going to take a while to see how it shakes out.