USELESS Coin vs Very Useful Coin

It is rare, in the investment world, for an investment to honestly and fully disclaim its basic nature in a way that finishes the story and requires no further analysis from us before making an investment decision. I have found such an investment. It is a cryptocurrency/meme coin called, appropriately, USELESS. https://coinmarketcap.com/currencies/theuselesscoin/ If you were to buy all of the USELESS in existence, it would cost you (as of this writing) about $272 million dollars. This seems to me to be a lot of money to pay for something useless, but what do I know?

Now, it should be noted that there are lots of useless coins. DOGE coin. Fartcoin. I could go on and on. But the difference here is that as far as I can tell, USELESS is being completely honest. It is not usable as a payment rail. It is not redeemable for anything, at any time, and therefore it is guaranteed to one day be worth zero. It doesn’t even come printed on a nice certificate so that the scripophiles can frame it and put it on the wall.

To be fair, as I said it isn’t the only such memecoin that is useless. It is merely the only one that turns that uselessness into a dare. It is a game, of seeing who eventually gets the ‘pride of place’ as top-ticking it, paying the highest price for something that is useless and that never pretended otherwise. (People who bought Enron stock were buying something that turned out to be worth zero, but they didn’t know it at the time. USELESS buyers are fully aware and cannot possibly claim otherwise.)

And actually, ironically, that unlocks the reason this coin exists. It reminds me of a fantasy baseball auction. For those of you who don’t play fantasy sports, there are generally two varieties: the ‘draft’ kind, where people take turns drafting players, and the ‘auction’ kind, where someone offers a player and a price they will pay for that player, from a limited budget allotment. The other participants in the draft all take turns bidding until someone wins the player, and then the process is repeated until every fantasy team is full. Done correctly, a bidder doesn’t merely bid for the players he or she wants but also bids up the price of a player he or she does not want, in order to force someone else to pay more than that player is worth. This part of the auction is a game, trying hard to make someone else pay top dollar – which requires you to figure out what everyone else’s top price is – while not getting stuck with the now-overvalued hot potato.

I think that’s what USELESS is. It’s a game of trying to push the price higher and higher, until someone is stuck with the honor of having paid the highest price for an utterly worthless unit. It’s a game; it’s only a game; and it is just as much of an “investment” as is the forty-two dollars you paid to select Juan Soto for your fantasy team.

Now, as you all know by now I have been at least partially converted and no longer think that all crypto is useless. The absolute opposite of USELESS is the enormous utility of our inflation-linked stablecoin, USDi. And yes, I’ve written about it before. And yes, I will write about it again. Because it’s as useful as it gets. There is no such thing as inflation-linked cash in traditional finance space. I am not aware of any bank that offers an inflation-linked savings account. And this is not a little thing. This is a big, big thing.

The chart below shows a hypothetical efficient frontier made up of a lot of different asset classes; this frontier might look a little different from what you’re familiar with because the x-axis and y-axis are in real terms whereas most of us learned finance in nominal terms where you had a Treasury bill as the risk-free asset. But we don’t care about nominal returns (if we did, we’d own stocks in the most hyper-inflating country we can find) – we care about real returns. In the nominal world, Tbills or money market funds exist with sub-zero real returns most of the time. More importantly, they have significant risk in after-inflation terms. As a result, in real space we are confined to the blue curve as our efficient frontier (the curve shows the lowest-risk portfolio that achieves a given expected real return. Remember these numbers are all hypothetical but the point I am making doesn’t depend on the numbers).

But USDi is, as I said, super useful. It is the origin security, the zero-real-risk, zero-real-return point. And that means that it improves every portfolio in real terms, with the possible exception of very-high-risk portfolios.

Now, most of these securities don’t yet exist in the defi world. There really aren’t any tokenized commodities yet, except in the narrow edge case of gold and one or two other single spot commodities – and no tokenized commodity indices yet, and commodity indices have additional sources of return beyond the spot commodity return. No tokenized TIPS, and few tokenized equities. Someday, the defi world will have these things. But what it does have right now, which is really useful and a good enough reason to visit the crypto world, is the low-risk security: USDi. How useful is that?

[N.b.: USDi was originally launched in a manner only available to accredited investors. However, because of growing regulatory clarity about its status as a stablecoin or currency rather than as a security, we have re-launched USDi so that the mint/burn functions are available to all. The coin’s address on mainnet is 0xAf1157149ff040DAd186a0142a796d901bEF1cf1. We will be adding functionality to allow minting or burning via user tools on our website, but in the meantime users can make a public call to the blockchain to mint or burn versus USDC. Reach out via the https://USDiCoin.com website if you want more information.]

Inflation Guy’s CPI Summary (June 2025)

If you squint, can you see an effect of the deportations of illegal aliens in today’s CPI report?

I don’t want to encourage anyone to obsess over every jot and tittle of the report. That’s almost always a fraught exercise. But there were at least a couple of things in the data this month which could indicate both inflationary and disinflationary effects of the deportation campaign. A serious part of my brain is saying ‘come on, there just haven’t been many deportations in the context of the population of illegals, how can we see an effect?’ And that instinct is probably right.

Before we get into today’s release let’s remember that there is one important context to keep in mind and that is that unless there are major surprises to the downside, core and headline inflation are going to be accelerating for most of the rest of the year on a year-over-year basis. I discussed this in a short podcast last week, Ep. 145: Beware the Coming Inflation Bounce. So we need to keep in mind as we think about markets and policy that the optics are going to look worse for a while here.

That is, unless we get numbers like we did in the May CPI, which was a major miss due mostly to very soft figures on rent inflation. Last month, Primary rents were +0.213% m/m and Owner’s Equivalent Rent (OER) was +0.275%. Rents are decelerating but not that fast, but if they did then a 2% target on inflation becomes at least possible. It’s not yet possible.

The consensus for today’s number was +0.26% on headline and +0.25% on core. Right in the middle of 0.2% or 0.3% rounded prints. What happened is that we got one that ticked up and one that ticked down. Actual CPI was +0.287% on headline, and +0.228% on core inflation. That caused the year/year headline number to print +2.7%, up from 2.4% last month (and higher than 2.6% expected), and y/y core to be 2.9% (vs 2.8% last month, and as-expected). The usual suspects trumpeted ‘another miss softer on core CPI! Rate cut on tap for September!’ But what is the real story?

The real story is not nearly that encouraging. As we will see, there are quite a few signs that the core miss was an aberration. Not a bad one, but deceiving.

Here is my guess at Median CPI.

The median category is likely the West Urban OER subcategory, which means that the actual median will depend on where that seasonal adjustment comes down. But two of the four OER subcategories are higher than that, so I doubt my guess is wildly off (when it isn’t one of those subcomponents, I nail the median but because they split up OER, sub-seasonals matter). So median should be around 0.30%, or 3.6% annualized. Median CPI has rounded to 3.5% y/y since February and it’ll be there again. That looks like progress has stopped. The chart below doesn’t include today’s figure but to illustrate that we’re seeing a flattening out of progress.

Now, this is what we would expect if tariffs were starting to affect prices generally, is that median would accelerate a little bit but core not necessarily. However, tariffs aren’t going to affect prices generally. They’re going to affect core goods primarily. So what is going on here?

One clue is that there was only one category this month that had an annualized monthly change of less than -10%. Normally there are a handful of categories on the tail (for example, there were 8 categories – in the way we slice them up for calculating Median CPI – where the annualized monthly rise was greater than +10%). This one category was Lodging Away from Home. Month/month was -2.9%, and year-over-year changes in hotel prices are at -2.5%: near the lowest levels since the sharp declines during COVID.

That may be where we squint and see a positive (lower inflation) effect of the deportations. We should expect that mass deportations should cause a relief on upward pressure on certain goods and services that happened when 8mm+ new residents arrived over 4 years. Folks love to focus on the wage effects as being inflationary (more on that in a moment) but they forget that you’re removing a bunch of consumers and while not 100% of illegal aliens work, 100% of them consume. And one of the things they consume is shelter. To be sure, we haven’t had anything remotely like ‘mass’ deportations yet. But releasing some of the hotels that were being paid for by cities to house migrants is one place that it’s totally understandable we should see a positive effect. The effect on home prices will come later.

While some pressure may continue to come off of shelter inflation, there’s this disturbing trend in Tenants and Household Insurance – and that’s before State Farm announced a 27.2% increase for Illinois. Yuck!

To be balanced on the deportation issue, let me point out something that comes up in the ‘four pieces charts’. Piece 1 is Food and Energy; Piece 2 is Core Goods; Piece 3 is Core Services less Rent of Shelter aka Supercore; Piece 4 is Rent of Shelter.

First, notice that core goods continues to trend positive – finally. Y/Y core goods went to +0.7% from +0.3%, despite continued softness in autos. The auto softness will not last forever; some of it is likely due to front-running tariffs. But more interestingly, note the small but measurable hook higher in Supercore. That’s where wages show up most strongly, so if deportations are causing better wages, we would expect that. So is this a deportations effect at the margin? I doubt it. As I said before, deportations are no where near “mass” yet so I’d be surprised to see an effect there. But watch this space.

So how excited are we about the core surprise lower?

The answer is not at all. Core goods is trending positive and while I don’t expect a massive tariff effect I am pretty sure it won’t be negative. Core services is going to have some upward pressure if deportations turn out to make a difference at all. Eventually, the effect on shelter and on other goods and services demand will be disinflationary but timing-wise that’s going to be after the tariff effect. And in the meantime, monetary aggregates are accelerating again in the US and Europe.

Is the story, then, that core inflation is going to continue to surprise to the downside? Well, when you look at the broader picture, at not only which prices are rising and falling but how broadly it’s happening, the news is not all unicorns and rainbows. Here is a chart of the weight of the CPI basket that is inflating at faster than 4% y/y.

That has improved, but I can’t help but notice that it is not even vaguely in the vicinity of pre-COVID. How can we get overall inflation to 2% if nearly half of the basket is inflating faster than 4%? Well, you’d need core goods to be really soft, and that part is done.

We can see that also in the Enduring Investments Inflation Diffusion Index (EIIDI), which has been sub-zero for a while but this month, jumped to positive.

These tell the same story – this month we could get all excited about the core miss…except that outside of Lodging Away from Home, the story isn’t so happy.

From a policy standpoint, there is just no reason to drop rates below neutral and we’re pretty close to neutral right now. Here’s something to think about (but the Fed won’t think about this because they don’t pay attention to money). Abstract from tariffs for a moment – tariffs are never a reason to maintain higher rates, because they are a one-off. But let’s suppose you believed that mass deportations would push up inflation and wages. The argument for a central banker would be that fewer workers in the economy implies a smaller economy, and a smaller economy needs less money. Therefore, while tight Fed policy can’t affect tariffs, they could affect prices that are rising because of deportations.

Again, let me clarify that I don’t think deportations are doing anything yet, and I think they’re as likely to push prices down in shelter and some core goods as they are to push wages and prices higher in services. I’m just saying that if you think deportations are inflationary, there is a monetary policy response that makes sense and it isn’t easy money.

So unless the economy starts to soften more seriously, there just isn’t a good argument right now for rate cuts. And now that the y/y numbers are heading higher because of base effects at least, the optics are going to be worse for the Fed to consider an ease. There is always an ‘unless’, and here the ‘unless’ is ‘unless Powell resigns and is replaced with an uber-dove.’ I can’t imagine that Powell wants to be the first Fed chairman ever to resign in disgrace, and no one can force him out, but stranger things have happened. However, I can’t handicap politics. I’m only handicapping inflation.

And, by the way, if you think that inflation itself is a handicap, consider the USDi coin! Here is a chart of the value of the coin by day. The red dot is where we are.

One final announcement. If you’re an investor in cryptocurrencies (in particular, stable coins) and have a Telegram account, consider joining the read-only USDi_Coin room https://t.me/USDi_Coin where the USDi Coin price is updated every four hours or so…and where these charts are also posted shortly after CPI just as I used to do on Twitter.

When and How Much Tariff Effect?

As we look forward to the CPI report next week, the monthly-repeating theme is ‘when will the tariff effect show up?’ The answer, so far, is ‘not yet,’ but economists who had forecasted the end of life as we know it when the Trump tariffs went into effect have been befuddled.

I’ve already admitted in this column that I was educated in the tradition of ‘tariffs bad,’ but that over the years Trump’s insistence otherwise has made me carefully re-think of which ways tariffs are truly bad, and which ways they’re not so bad. Naturally, if tariffs were uniformly bad – which seems to be the orthodoxy – then it would be really hard to explain why almost every country levees tariffs. Maybe forty years ago we could blame the benightedness of those poor policymakers in other countries, who clearly just didn’t understand how bad tariffs are. But now? Heck, all someone in one of those countries needs to do is ask ChatGPT ‘are tariffs bad,’ and they’ll learn!

… Conclusion: Tariffs can be useful tools in specific, limited circumstances — like protecting vital industries or responding to unfair trade practices. But long-term, high or broad tariffs often do more harm than good, especially in highly interconnected global economies. (ChatGPT, July 9, 2025 query ‘Are tariffs bad’)

But it seems every country has these specific limited circumstances! It’s evidently only bad when the US does tariffs. And that is what made me ask whether maybe there is some nuance. My 2019 article “Tariffs Don’t Hurt Domestic Growth” was really good, I thought.

Even as there has been some small movement in the economintelligencia, though, about whether tariffs are all bad there has been very little movement in the notion that they are clearly inflationary. No doubt, implementing a tariff will raise prices at least a little, but how much is the important question. And regardless of that answer, tariffs are a one-time adjustment to the price level even if that effect is smoothed over a period of time. (This is why it’s weird to hear Powell say that the Fed can’t ease because they’re waiting to see the effect of the tariffs on inflation. That’s economic nonsense. The Fed can’t possibly believe that keeping rates high is the proper response to a one-time shock.)

On this question, I thought I’d share something I wrote in our Quarterly Inflation Outlook from Q1 (in mid-February), in which I roughly estimated the effects of a 20% blanket tariff. I know the answer isn’t “right,” because that’s the wrong question – there isn’t a 20% blanket tariff. But I undertook the estimate to get an idea of the relative scale of effects. (I included in the piece some parts from that 2019 article mentioned above, because I’m not above stealing from myself!) I will add some concluding thoughts after this ‘reprint’ from our QIO – which, by the way, you can subscribe to here.

Tariffs as a Tool to Promote Domestic Growth and Revenue

In the President’s view, the fact that the U.S. has a very low tariff structure compared to the tariffs (and arguably VAT taxes) that other countries place on U.S. goods is prima facie evidence that the U.S. is being taken advantage of and treated unfairly on world markets. The U.S. has, for the better part of a century, been the main global champion of free trade and this tendency accelerated markedly in the early 1990s (as the familiar chart below, sourced from Deutsche Bank, illustrates well).

The effect of free trade, per Ricardo, is to enlarge the global economic pie. However, in choosing free trade to enlarge the pie, each participating country voluntarily surrenders its ability to claim a larger slice of the pie, or a slice with particular toppings (in this analogy, choosing a particular slice means selecting the particular industries that you want your country to specialize in). Clearly, this is good in the long run – the size of your slice, and what you produce, is determined by your relative advantage in producing it and so the entire system produces the maximum possible output and the system collectively is better off. To the extent that a person is a citizen of the world, rather than a citizen of a particular country – and the Ricardian assumption is that increasing the pie is the collective goal – then free trade with every country producing only what they have a comparative advantage in is the optimal solution.

However, that does not mean that this is an outcome that each participant will like. Indeed, even in the comparative free trade of the late 1990s and 2000s, companies carefully protected their champion companies and industries. Even though the U.S. went through a period of being incredibly bad at automobile manufacturing, there are still several very large U.S. automakers. On the other hand, the U.S. no longer produces any apparel to speak of. In fact, the only way that free trade works for all in a non-theoretical world is if (a) all of the participants are roughly equal in total capability, and permanently at peace so that there is no risk that war could create a shortage in a strategic resource, or (b) the dominant participant is willing to concede its dominant position in order to enrich the whole system, rather than using that dominant position to secure its preferred slices for itself and/or to establish the conditions that ensure permanent peace by being the dominant military power and enforcing peace around the world. We would argue that (b) is what happened, as the U.S. was willing to let its own manufacturing be ‘hollowed out’ in order to make the world a happier place on average.

The President (and many of those who voted for him) feel that (b) is inherently unfair, or has reached extremes that are unfair to U.S. citizens. Essentially, the President is rejecting the theoretical Ricardian optimum and pursuing instead a larger slice for his constituents. This is where reciprocal tariffs (where the U.S. matches the tariff placed on its exports by a trading partner, with a tariff placed on the imports of that product from that trading partner) or blanket tariffs (where the U.S. imposes a tariff on all imports of a product irrespective of source – e.g. aluminum – or on all imports from a given trading partner) come in.

Blanket tariffs are good for domestic growth,[1] but definitely increase prices for consumers. How good they are for growth, and how much prices rise, depends on how easily domestic un-tariffed supply can substitute for the imported supply and also on whether your country is a net importer or exporter, and how large the export-import sector is in terms of GDP. Because this is an inflation outlook, let’s make a very rough estimate of the impact on the overall domestic price level of a blanket 20% tariff (such as the one Treasury Secretary Bessent has proposed). We suppose the average elasticity of import demand in the U.S. to be 3.33[2] and the elasticity of export supply to be 1.0[3]. In that case, the incidence of a tariff falls about 23% on consumers: [1.0 / (3.33+1.0) ]. So, for a 20% tariff, prices for the imported goods would be expected to rise about 4.6% (20% tariff x 23% incidence). However, imports only account for about 15% of US GDP, which means the effect on the overall price level would be 15% x 4.6% = 0.69%.

So, for a 20% blanket tariff on imports, Americans should expect to see a one-time increase in the overall price level of something on the order of 0.7%, smeared over the period of implementation. This is not insignificant, but it is also not calamitous. It does affect our estimates for 2025 and 2026 inflation, shown in the “Forecasts” section (somewhat less than 0.7%, because we do not expect a blanket tariff but rather reciprocal and targeted tariffs). Also note that the retaliatory tariffs on US exports have no direct effect on domestic prices, so that whether or not trading partners retaliate is irrelevant to an analysis of first round effects, anyway.

Thus my wild guess back in February was that a 20% blanket tariff would result in a bit less than 0.7%, smeared out over 2025 and 2026. That doesn’t answer the ‘timing’ question, but the delays in implementation (so as to not affect Christmas 2025 prices of the GI Joe with the Kung-Fu Grip) and the importer/retailer initial reaction to try and absorb as much as possible for optics – presumably, easing price increases into the system later – mean that it shouldn’t be shocking that we haven’t seen a big effect yet. My point in the above calculation, though, is that we really shouldn’t expect to see a big effect, regardless.

For what it’s worth, the Budget Lab at Yale estimates that currently “the 2025 tariffs to date are the equivalent of a 15.2 percentage point increase in the US average effective tariff rate,” so if we take my 0.7% guess for 20% then we would be looking closer to 0.5% in total. And in fact, lower even than that since the 15.2% average will have less impact than a 15.2% blanket tariff, assuming that the tariffs will be highest where domestic substitution is easier.[4]

Wrapping this up, let me make one final observation. Current year/year headline CPI inflation is 2.35%. The inflation swaps market, specifically the market for ‘resets’ where you can trade essentially the forward price level, currently suggests that traders expect y/y inflation to rise to 3.29% over the next six months: almost 1 full percentage point from here. But that actually flatters what the market is pricing, because the shape of the energy curves suggests that rise is being dragged about 20bps lower by the implied moderation in energy prices (give me a break, inflation traders: I’m doing this in my head).

So, the market is pricing core inflation peaking about 6 months from now, about 1.2% higher than it currently is. Not all of that is the effect of tariffs; some is due to base effects as the very low May, June, and July 2024 numbers roll off of the y/y figure. But if we get that result, you can be sure that economists will put most of the blame on Mr. Trump, while Mr. Trump will put most of the blame on Mr. Powell. Either way, I think the interest rate cuts that the President would prefer are unlikely unless growth takes a significant stumble.

[1] …but bad for global growth! There is no question that unilaterally applying tariffs to imports is bad for all suppliers/countries providing those imports. If Ricardo is right, the overall pie shrinks but the domestic slice gets larger…at least for the dominant players who already have a large slice. If everyone raises tariffs in a trade war outcome, the less-productive countries suffer the most loss of growth and the most-productive countries likely still benefit. But prices rise for all.

[2] Kee, Nicita, and Olarreaga, “Estimating Import Demand and Export Supply Elasticities”, 2004, Figure 5, available at http://repec.org/esNASM04/up.16133.1075482028.pdf Your answers may vary!

[3] Estimates are wildly all over the map, depending on the exporting country and the product. In general the smaller the country, the more price-inelastic it is. We chose unit elasticity here (a 1% increase in price cause a 1% increase in the quantity supplied) just to be able to get a rough guess.

[4] To be fair, the Budget Lab at Yale also estimates the effect on PCE inflation of a whopping 1.74%. They must be really surprised at the impact so far.

The Twin Deficits – One Out of Two IS Bad

From time to time on this blog, I circle back to the question of the balance of deficits. In my mind, as our economy goes through whatever the “Trump Transition” is, the biggest risk to the bond markets is not from some fear about whether the Treasury will default or whether the US dollar will cease to be the world’s currency of choice for reserves (neither of which I think is going to happen any time soon) but that large secular changes in the balances of savings and dollar demand could lead to outsized moves in interest rates.

First, let me remind you that the deficits are all intertwined. When the US Federal Government runs a deficit and borrows money, they have to get it from people/entities that have saved that money. One place that the government bond salesmen know they can turn to is non-US investors, who are in possession of those dollars because the US runs a large trade deficit with most other countries. When we run a trade deficit, it means we are importing more stuff than we are exporting or, equivalently, we are exporting more dollars than we are importing. Those dollars are pretty useless except to buy things that are dollar-denominated. By construction, we know that the new owners of dollars aren’t buying goods, because if they did there wouldn’t be a deficit; the main other thing they buy are securities or real property.

So if you don’t want other countries buying US stocks, buildings, and farmland, run a big trade surplus and they won’t have the dollars to do it.

It’s a good thing they have all of those dollars, because the Federal government needs them! The federal deficit needs to be funded by those foreign dollars, or by domestic savings (banks, individuals, companies, e.g.), or by the central bank buying up those bonds. And that’s pretty much it. Over time, the trade balance plus the budget balance plus the central bank balance plus private savings equals zero, more or less. During COVID, the massive expansion of the federal deficit was only possible because the Fed bought about the same number of bonds as the government sold. Had they not, interest rates would have risen precipitously because private savers would have had to be induced to put those dollars into bonds.

(Or, the government would give incentives for banks to hold more govvies, say by exempting them from the SLR. Not that such a thing would ever happen!)

Let’s pivot this then back to the Trump Transition. The stated goal of the Administration was to lower the trade deficit a lot, lower the budget deficit a lot, and lower interest rates. That all makes sense and is internally consistent. It could happen that way, if all of it happens that way.

What if, though, the President’s team makes more progress on one front than on the other? Early returns on the tariff front seem to imply that the US will face a smaller trade deficit going forward. Now, the latest spike higher (smaller deficit) here is at least partly and maybe mostly due to a ‘payback’ of the pre-tariff front-running that led to massive deficits in the prior three months. But it should not surprise us that increasing tariffs should cause the trade deficit to decline. That is, after all, sort of the point.

If we concede that the trade deficit is actually heading back towards some better semblance of balance, then that’s plank 1 of the Trump agenda. That will supply fewer dollars to cover the federal budget deficit, though. As long as the federal budget gets into something closer to balance…

That was the promise of DOGE, and of the revenues from tariffs. The latter will indeed be yuge, and will help balancing the budget. Or it would, if we weren’t about to run an even bigger deficit with the Big Beautiful Bill soon passing into law. The trailing-twelve-month budget deficit is just less than $2 trillion, which was a number we never even sniffed prior to COVID. So that’s the demand for savings: the feds look like they’re going to keep on spending more than they take in.

Unlike during COVID, too, the Fed is now letting its balance sheet shrink. No help there.

Now, there is also a movement in Congress to pass legislation preventing the Fed from paying interest on the reserves that banks hold at the Fed. For decades, the way the Fed managed the money supply was to adjust the quantity of reserves, which rationed credit and caused the price of credit (interest rates) to move as well. But it was the rationing of credit, not changing the price, that affected the money supply. Beginning with the Global Financial Crisis, the Fed flooded extra reserves into the system, forcibly deleveraging banks (look at that chart above again) – but, since that would also crush bank earnings, they started paying interest on reserves (IOR). Since, if banks were not being paid to hold reserves, they would hold as little as they could, the Fed had to pay interest or the excess of reserves in the overnight market would cause interest rates to always be zero. So the Fed started to manage the price of credit, rather than its quantity. The central bank fully intends to always hold way more in securities and therefore force way more reserves into the banks, going forward – but has gradually been reducing its portfolio securities. As I said, no help there.

If Congress succeeds in preventing the payment of IOR – and the politics on this looks good since the Fed now runs operating deficits, so that it is basically paying banks interest with taxpayer dollars (see chart below…Fed remits to the Treasury have dried up completely), then as I said above banks will try to hold fewer reserves and overnight interest rates will drop as banks compete to lend their excess reserves at anything above zero, unless (a) the fed increases the reserves banks are required to hold (really unlikely) or (b) the fed makes reserves scarce so some banks will have to buy them and some will sell them (the old way) (also really unlikely). In neither case does the Fed expand the balance sheet as a first intention, so unless we get another crisis the expansion of the Fed balance sheet is unlikely in my view.

So that leaves private savings. If the trade deficit declines and the budget balance doesn’t move significantly towards balance, then interest rates will have to rise, potentially a lot. I think the President’s stated plan makes very good economic sense. I just wonder if it’s going to be derailed by the desire to keep the Federal spend going.

The Road to Crypto Conversion

While this isn’t exactly the conversion of Saul on the road to Damascus, I came to a realization recently that subtly changes the way I look at the potential for large cryptocurrencies, such as Bitcoin.

Historically, my attitude has been dismissive about the value of bitcoin itself. While I recognize the amazing reach of blockchain technology and the genius of using asymmetric key cryptography to secure the public record of private transactions, I’ve always thought that bitcoin didn’t really achieve the promised goal, which was to be a better money than fiat dollars. After all, bitcoin is not backed by anything more than the dollar is – nothing. Its value is based on scarcity, and scarcity by itself is not a source of value (if it was, my toenail clippings would be immensely valuable). So in my 2016 book What’s Wrong with Money? I wrote in a chapter on bitcoin:

“But is bitcoin money? Calling it a virtual currency, or a digital currency, or a crypto-currency doesn’t make it money. At some level, it is of course money in the same sense as cigarettes are to prison inmates. It serves as a medium of exchange, a store of value, and a unit of account – but only within the special community that already accepts bitcoin as credible…It is not yet broadly a credible currency. It doesn’t have universal value because not everyone believes that everyone else will accept bitcoin.”

Even in that chapter I recognized that bitcoin may someday be money-like. And I underwent a partial conversion and even worked for a while on a paper with my co-authors Kari Walstad and Scott Wald to define a measure (“Crypto Trust Index”) that would objectively measure how much like money the cryptocurrency world was becoming. [That paper ended up being overtaken by real-world developments, as stablecoins fully backed by fiat balances are obviously crypto money by identity, rendering the question moot.]

But in my mind bitcoin, eth, etc aren’t money but speculative vehicles – they are distinctly separate from USDC, USDi, and other fully-backed coins. It may be that they belong in a portfolio with stables and/or securities, but since bitcoin has no intrinsic value I have always held the view that I don’t want to own it as it can go to zero in a nonce.[1]

Recently, as I said, I’ve had a mild conversion as a result of two realizations.

The first realization is that even in the traditional securities world, we sometimes invest in things which have no intrinsic value in many states of the world. For example, we buy out-of-the-money options, or equity in a firm that is highly leveraged so that if the business goes under, the equity-holders get nothing. I am not sure this is a good excuse to buy bitcoin, though, since even if a far out-of-the-money option is unlikely to ever have intrinsic value there are at least future states of the world in which it could have intrinsic value. Similarly, that penny stock might end up being worth something if business booms. So we could think about bitcoin as being an option that may go to zero or may go up a lot. The problem with this, and the reason this reasoning alone is not compelling to me, is twofold. First, those far out-of-the-money options and long shots tend to have low prices, not high prices, and bitcoin certainly does not seem to have a low price. Second, there is no state of the world in which bitcoin will ever have an intrinsic value. Therefore, it doesn’t make a lot of sense to think of it as a real option, but at best as a speculation with an option-like payout (low in many states of the world, but massive in a few states). Put another way, while the value of that penny stock or out-of-the-money option can go to zero for some clearly-defined reasons, bitcoin can go to zero for any reason or no reason and it wouldn’t be wrong.

The second realization, though, relates to scarcity. Yes, scarcity alone cannot be the basis for value (see: my toenails). For scarcity to matter, there needs to be exogenous demand. And that demand need not be rational. If someone wants to hold bitcoin, not caring that it has no intrinsic value (or erroneously believing that it has some), then scarcity matters. The realization is that scarcity goes from not mattering at all, to mattering a great deal, as soon as there is any demand. To be sure, if that demand goes away, then scarcity again ceases to matter.

(By the way, it is entirely possible and even likely that someone else has pointed this out.)

So the case for speculating in bitcoin (no, I won’t call it investing) is that since the total supply is independent of price, the supply curve is vertical and moving to the right at an ever-slower rate. As this happens, it takes less and less increase in demand to push price higher.

It also takes less and less decrease in demand to push price lower. Since there is no slope to the supply curve, it means that oscillations in demand are responsible for all of the oscillations in bitcoin’s price. And we can say more about the volatility dynamics. Early in bitcoin’s development – when demand was very low, supply was relatively high compared to demand, and the price was as a result very low – we were operating at the far left end of the demand curve where demand was relatively more elastic and therefore there was a lot of volatility. As bitcoin matures, and demand catches up to the existing supply, we should expect price volatility to decline. And this is, in fact, what has happened (chart below, source: Bloomberg, shows rolling 100-week historical volatility (about two years, but I like round numbers today), now at the low-low level of 43% (about 3x equity market volatility).

The fun part comes later, when the supply curve shifts get slower and slower as the bitcoin halving converges to zero and the bitcoin supply gets closer and closer to its absolute maximum. At that point (and here is where the uberbulls get really excited), if there is a steady secular increase in demand, price just goes up without bound.

Don’t get too excited, uberbulls, because we aren’t there yet. When we are starting to get close to that point I would expect that we will also see volatility start to go up again. If historical volatility continues to decline, it means (a) we aren’t close enough to that point that the vertical singularity is nigh, and/or (b) people are losing interest in or diversifying away from bitcoin so that the steady increase in demand is not manifesting and interest is fluctuating less and less. So, I am waiting for that volatility to begin to expand at higher prices.

In any case, I am much more likely to invest in tokenized real world assets than I am Bitcoin or Ethereum. I am not a speculator at heart. Heck, I’m a bond guy which means I worry more about return of my principal than return on my principal. But if you are already long bitcoin, I will no longer sneer at you, because I recognize at last that one way or the other I will may be driving your car someday – either because it was repossessed and I bought it at auction, or because I am your chauffer.

Did You Know? Want to buy USDi, the inflation-linked stable coin, but don’t own any crypto you can exchange for it? You can actually use the coin as an on-ramp. Accredited investors need merely complete onboarding with USDi Partners and then can invest fiat dollars and receive USDi coins.

[1] Pun intended.

Inflation Guy’s CPI Summary (May 2025)

Well, this was an odd one to sort out.

Going into the CPI announcement this morning, the economist consensus was for +0.17% (seasonally adjusted) on headline CPI m/m and +0.28% on core. Market changes this month have been very contained, partly because of the usual summer doldrums kicking in and partly (most likely) because of the degree of uncertainty surrounding all of the chaotic policy changes that have taken place in 2025. The effects of these changes (and more to come!) are still making their way through the system.

This is a calm surface over a roiling ocean. Economists continue to debate (and their analysis, to me, seems in many cases to be colored by the political lens they are looking through) about the impact that the current tariff structure will have, about the effect of future tariff changes – and what those will be, about the impact of the Most-Favored-Nation policy on pharmaceutical pricing and availability, about the effect the deportation of illegals (and self-deportations) will have on housing (rent inflation softer, but how much?) and labor supply (wages upward, but how much?) and Lodging Away from Home.

Actually, I’m overstating that a little bit. Most classically-trained economists mostly agree about how horrible this will all be, because tariffs bad. My own estimates have tariffs pushing inflation a little higher in the near-term, but not terribly. I also think that mass deportations would be very disinflationary because of the effect on rents but it is looking less and less like ‘mass deportations’ means tens or hundreds of thousands, not millions, and that effect likely won’t be huge.

Meanwhile, the Fed is keeping rates slightly above neutral but money supply growth has re-accelerated to a level that’s not likely to be consistent with inflation at 2%. Underlying trend median inflation is running about 3.5% or so, and is unlikely to fall a lot further given the current configuration of fiscal and monetary policy.

Let’s get into the data, then. The actual CPI was +0.08% (SA) on headline and +0.13% on core. That’s a significant miss, especially on core.

Core inflation has recently been missing low on a fairly regular basis, although most of the misses have been small. Median inflation in most cases hasn’t been confirming those misses, because they’ve generally been one-offs that don’t really wiggle median too much. It’s still a positive sign if the ‘tails’ are to the downside so that core CPI is below median CPI, but Median tells us not to get too excited. This month, though, Median also showed an effect. My estimate is that Median CPI will be the lowest since last July, at +0.25% m/m. It’s still difficult to see a major disinflationary trend here.

There’s more uncertainty than usual around my Median guess, but let’s take it as a given for now.

You don’t have to look too far to see one of the major culprits for the miss this month. Primary Rents were up +0.21% m/m, which is a lot slower than they had been running at.

Owners’ Equivalent Rent was also soft, and between those two surprises it’s probably roughly 5bps of the Core CPI miss. Let’s be clear – rents are not collapsing and indeed, we’ve just converged with our model.

Let’s be clear: if you are in the camp that we’re going to get back to 2%, you need this to not be an aberration. You need shelter inflation to continue to decelerate. But as you can see from the chart of month/month primary rents above, sharp movements in rents tend to be reversed in subsequent months. This looks a lot to me like last July’s surprise, which was reversed in August. We will see. But ex-shelter, year/year Core CPI rose, to 1.87% from 1.78%.

What is interesting to me as I write this, looking at some of the other commentary, is that folks don’t seem to be focusing on this. Of course it’s all tariffs, all the time, and everyone is scratching their heads over why we are seeing price declines in some of the categories where you’d expect the tariffs to help. Key example (and significant example) is autos, where the CPI for Used Cars and Trucks was -0.54% m/m after a similar decline last month, and New Cars were down -0.29% m/m. If there is one place that economists were certain we would see tariff-induced inflation, it was in autos. Not so much, at least yet. This might be because the lags are longer than we expect in a just-in-time manufacturing world, or it might be because demand elasticity is bigger than people thought.

But even with autos, Core Goods inflation accelerated to +0.3% y/y from +0.1% last month.

Remember, above I said that core goods ex-shelter had accelerated. I don’t want to fall into the trap of taking out all of the things that go down, to make the insightful conclusion that everything else went up – but that acceleration in core goods included the weighty autos contribution to the downside so you can tell that there are indeed upward pressures. Just not in the big things.

One place we saw increases was in Tenants’ and Household Insurance, which rose 0.84% last month, and in Motor Vehicle Insurance, which rose 0.68%. That helped keep core services inflation at +3.6% y/y, even with the slowdown in housing. On the other hand, Airfares suffered a third straight significant decline, -2.74% m/m. And while we are surprised to see auto prices decline, given the tariffs, we are also surprised to see Medicinal Drugs prices increase, given Trump’s new “Most Favored Nation” policy. Pharma prices were +0.54% m/m (although the y/y increase slackened some and is only +0.35% y/y). Core Services less Rent of Shelter (aka “Supercore”) is down to 3.11% y/y, and that’s good news even if it’s still quite a bit higher than it was pre-COVID. The trend is your friend, and this is a good trend for now.

As with the market itself, then, we’re seeing a lot of movement in both directions; it’s just all canceling out into a relatively tame increase in the overall CPI basket. That’s not likely to be the ultimate outcome. The last four year/year increases in Median CPI (assuming I’m vaguely right about the m/m, and we’ll know that in an hour or two) have been 3.53%, 3.48%, 3.46%, and 3.44%. That does not give the impression of a series that is in a hurry to get down to 2.25%-2.5%, which would be roughly consistent with sustainable core CPI around 2%. Again, you need to get shelter prices to really decelerate significantly further.

Now, even if that does happen, it isn’t going to keep y/y measures on a steady deceleration track for the next year. While we haven’t seen a major impact from tariffs yet, and my view is that it won’t be a huge impact in any case except for particular items, I am pretty sure we will see something and median and core inflation will see acceleration over the balance of this year and into next year. Thereafter, it depends on what happens with policy in the interim. On that score, while the current numbers still give the Fed no good reason to ease it also should pretty much remove any notion that monetary policy is about to get tighter. M2 growth is back to 4.4% y/y, and 6.4% annualized over the last quarter. That’s back to what was normal when we were experiencing the tailwinds of globalization and positive demographics. It is too fast now that those are headwinds.

But as I said, that’s the story for later this year and it could change. In the meantime, we keep waiting for the tariff effect. If three months from now we still haven’t seen an effect, then things will get very interesting.

One final announcement. If you’re an investor in cryptocurrencies (in particular, stable coins) and have a Telegram account, consider joining the read-only USDi_Coin room https://t.me/USDi_Coin where the USDi Coin price is updated every four hours or so…and where these charts are also posted shortly after CPI just as I used to do on Twitter before they changed the API to make auto-tweeting charts very difficult.

Why a 4.5% Nominal Rate is Roughly Equilibrium…Hmmm, Sounds Familiar…

I was planning to write today about why a 4.5%-5.0% nominal Treasury rate is not only not the end of the world, but actually sort of normal. Naturally, the reason I am even thinking about the topic is because of all of the apparent alarm because the current long bond recent peeked above 5% and the 10-year note at 4.50% continues to flirt with those levels. Because we haven’t seen the 10-year rate above 5% for a sustained period in about 18 years, it is natural that some of the young folks who were raised in an era of free money would think that this is the end of the world.

I’ve previously written about the return of some of the phenomena that we used to take for granted, such as the presence of optionality in the bond contract. After most of two decades of unhealthy interest rates produced unhealthy leverage habits among other unwelcome developments (including the leveraging of the government balance sheet because it was so cheap to borrow for one’s programs with no cost), I suppose it shouldn’t be surprising that there is so much wailing and gnashing of teeth, rending of garments, etc. But for those people who expect the Fed to lower rates significantly, because “after all 2% is the normal level of interest rates,” I am here to say that you probably don’t want the crack-up that would be necessary to make that plausible. The current level of interest rates is inconvenient for many organizations with a borrowing problem, but it is really quite normal.

Anyway, I’d intended to write a longer version of that, and as I started to write something bugged me and I looked back and noticed that I’d already written essentially the same thing a few years ago. At the time (June 2022) I was explaining “Why Roughly 2.25% is an Equilibrium Real Rate,” and of course if you add reasonable inflation expectations of 2.5%-3% you get to 4.75%-5.25% as an equilibrium nominal rate (and a bit higher than that for the 30-year, which also incorporates a modest additional risk premium). If you go and read that article directly, you can also get my screed on how models trained on the last 25 years of data leading up to the inflation spike only survived if they forecast a very strong reversion to the mean, and so *eureka* all of those models missed the entire inflation spike. But here is a reprinted snippet (reprinted by permission from myself) outlining the argument for why the current level of long-term real interest rates is about right.

Kashkari made a different error, in an essay posted on the Minneapolis Fed website on May 6th.[1] He claimed that the neutral long-term real interest rate is around 0.25%, which conveniently is where long-term real rates are now.

However, we can demonstrate that logic, reinforced by history, indicates that long-term real rates ought to be in the neighborhood of the economy’s long-term real growth rate potential.

I will use the classic economist’s expedient of a desert-island economy. Consider such an island, which has two coconut-milk producers and for mathematical convenience no inflation, so that real and nominal quantities are the same. These producers are able to expand production and profits by about 2% per year by deploying new machinery to extract the milk from the coconuts. Now, let’s suppose that one of the producers offers to sell his company to the other, and to finance the purchase by lending money at 5%. The proposal will fall on deaf ears, since paying 5% to expand production and profits by 2% makes no sense. At that interest rate, either producer would rather be a banker. Conversely, suppose one producer offers to sell his company to the other and to finance the purchase at a 0% rate of interest – the buyer can pay off the loan over time with no interest charged. Now the buyer will jump at the chance, because he can pay off the loan with the increased production and keep more money in the bargain. The leverage granted him by this loan is very attractive. In this circumstance, the only way the deal is struck is if the lender is not good at math. Clearly, the lender could increase his wealth by 2% per year by producing coconut milk, but is choosing instead to maintain his current level of wealth. Perhaps he likes playing golf more than cracking coconuts.

In this economy, a lender cannot charge more than the natural growth in production since a borrower will not intentionally reduce his real wealth by borrowing to buy an asset that returns less than the loan costs. And a lender will not intentionally reduce his real wealth by lending at a rate lower than he could expand his wealth by producing. Thus, the natural real rate of interest will tend to be in equilibrium at the natural real rate of economic growth. Lower real interest rates will induce leveraging of productive activities; higher real interest rates will result in deleveraging.

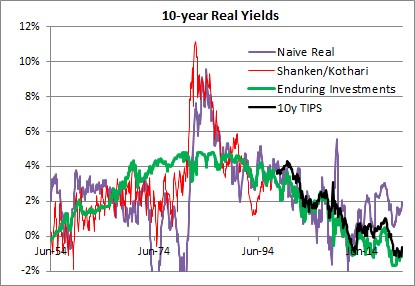

This isn’t only true of the coconut economy, although I would strongly caution that this isn’t exactly a trading model and only a natural tendency with a long history. The chart below shows (1) a naïve real 10-year yield created by taking the 10-year nominal Treasury yield and subtracting trailing 1-year inflation, in purple; (2) a real yield series derived from a research paper by Shanken & Kothari, in red; (3) the Enduring Investments real yield series, in green, and (4) 10y TIPS, in black.

{kind=link}

The long-term averages for these four series are as follows:

- Naïve real: 2.34%

- Shanken/Kothari: 3.13%

- Enduring Investments: 2.34%

- 10y TIPS: 1.39%

- Shanken/Kothari thru 2007; 10y TIPS from 2007-present: 2.50%

It isn’t just a coincidence that calculating a long-term average of long-term real interest rates, no matter how you do it, ends up being about 2.3%-2.5%. That is also close to the long-term real growth rate of the economy. Using Commerce Department data, the compounded annual US growth rate from 1954-2021 was 2.95%.

It is generally conceded that the economy’s sustainable growth rate has fallen over the last 50 years, although some people place great stock (no pun intended) on the productivity enhancements which power the fantasies of tech sector investors. I believe that something like 2.25%-2.50% is the long-term growth rate that the US economy can sustain, although global demographic trends may be dampening that further. Which in turn implies that something like 2.00%-2.25% is where long-term real interest rates should be, in equilibrium.[2] Kashkari says “We do know that neutral rates have been falling in advanced economies around the world due to factors outside the influence of monetary policy, such as demographics, technology developments and trade.” Except that we don’t know anything of the sort, since there is a strong argument against each of these totems. Abbreviating, those counterarguments are (a) aging demographics is a supply shock which should decrease output and raise prices with the singular counterargument of Japan also happening to be the country with the lowest growth rate in money in the last three decades; (b) productivity has been improving since the Middle Ages, and there is no evidence that it is improving noticeably faster today – and if it did, that would raise the expected real growth rate and the demand for money; and (c) while trade certainly was a following wind for the last quarter century, every indication is that it is going to be the opposite sign for the next decade. It is time to retire these shibboleths. Real interest rates have been kept artificially too low for far too long, inducing excessive financial leverage. They will eventually return to equilibrium…but it will be a long and painful process.

At the time I wrote the passage above, 10-year TIPS yielded about 0.25%; today they yield 2.125%. It turned out that returning to equilibrium wasn’t at all a long process. But it certainly was painful!

Returning to the original point: just because 10-year rates are now approximately at equilibrium is not at all a prediction that they will remain at equilibrium. Indeed, if I made that prediction I would be making a very similar mistake to the one I criticized above. Mean reversion in rates is not a particularly powerful force, when set against an active central bank and a profligate legislature. But if it matters at all, it is very important to correctly identify the mean to which rates should revert.

And it’s not 2%.

[1] https://www.minneapolisfed.org/article/2022/policy-has-tightened-a-lot-is-it-enough

[2] The reason that real interest rates will be slightly lower than real growth rates is that real interest rates are typically computed using the Consumer Price Index, which is generally slightly higher than the GDP Deflator.

Inflation Guy’s CPI Summary (April 2025)

Before the CPI analysis, I always try to give some context for where we are in the ‘story’ about the evolution of inflation right now. It’s really difficult to do that, though, because of all of the massive policy changes that are happening – and often in opposite directions with respect to the effect on inflation. Here is the Baker, Bloom & Davis Economic Policy Uncertainty Index, which is derived by scraping news sources. Even strong supporters of President Trump’s have to admit that his Administration has been a whirlwind on economic policy (for many of them, of course, that’s a feature and not a bug).

Here goes, anyway. Remember that last month, core CPI crashed but Median CPI actually accelerated. This kept us from actively celebrating the great inflation news; we knew that the good news was concentrated in a few one offs. In particular, Airfares (-5.3% for March), Lodging Away from Home (-3.5%), Used Cars (-0.69%), Car and Truck Rental (-2.66%), and Medicinal Drugs (-1.30%). But, as Median showed last month, there was really no reason to think that inflation was behind us…even before any effect from tariffs.

Speaking of tariffs, prior to this month we hadn’t really expected to see any effect yet and most economists thought that we shouldn’t see that much impact in the April figures either since the big tariffs on everyone went into place early in that month. However, remember that Mexico, Canada, and China had all faced escalating tariffs prior to April, so if there is going to be an impact we should expect to see something soon. I don’t expect a lot in most categories, but some impact in a few. It will be hard to discern how much of any monthly price change is tariffs, of course. We will look at Apparel, where demand elasticity in the short run is not terribly low. Broadly, though, remember that demand elasticity and foreign content percentage are both important…and foreign content in most goods is pretty low. I’d also look to Medicinal Drugs, since a lot of APIs are China-sourced and the demand for many drugs is pretty inelastic in the short-run, but I didn’t expect a lot of impact there (pharma companies will have had inventories), and going forward it will be muddied by Trump’s announcement of the Most-Favored-Nation policy in pharmaceuticals.

Speaking of that announcement, this month’s review of changes in inflation swap levels is seriously polluted because that announcement combined with the 90-day pause on China tariffs caused a massive crash in 1-year inflation expectations.

Despite the drop in tariff rates on China (for now), remember average tariffs remain the highest since the Great Depression (ominous music)! Of course, back then the US was a significant net exporter, so reciprocal tariffs were a bigger problem. Imports were only about 2-3% of GDP.

(Chart above is from https://www.stlouisfed.org/on-the-economy/2019/may/historical-u-s-trade-deficits)

(Chart above is from https://www.stlouisfed.org/on-the-economy/2020/march/evolution-total-trade-us)

There you go. That’s the context. Now onto the number.

CPI for April was expected to be +0.25%, and +0.27% on Core. The actual prints were 0.221% and 0.237%, respectively, so a mild surprise lower (although it turned the +0.3%/+0.3% rounded expectations to +0.2%/+0.2%, looking more dramatic a surprise than it actually was). Core is right about where it has been for the last 6 and 12 months (0.244% and 0.229% average, respectively) with the big January spike and the March plunge basically offsetting each other.

Amazingly, of the eight major subgroups only Housing, Medical Care, and “Other” increased on a m/m basis. What is especially surprising in that light is that Apparel – where the tariff canary in the coal mine lives – was down on the month.

Core goods continues to hook higher, now at +0.13% y/y. Remember, this is before any tariff effect has really been felt. In my mind, this is more the underlying ‘deglobalization’ effect: as I’ve said for a while, the deep deflation in core goods that we saw was a partial retracement of the COVID spike and we should expect going forward to see a small positive inflation in goods. Core services is decelerating nicely, and it will need to continue to do that if we’re ever going to see downward pressure in median inflation from where we are now.

Speaking of Median CPI, my early estimate is +0.308% m/m, putting the y/y at 3.43%. That’s about where we’ve been, and where we’re likely to be going forward.

Looking at some of those one-off categories from last month, Airfares fell another -2.83% m/m after that -5.3% prior decline. Some of that is jet fuel, some is tourism I suspect. Lodging Away from Home went flat (-0.1% m/m) from -3.54% prior. I think we’ll see continued downward pressure in that category, as hotels in some big cities are gradually emptied of illegal migrants and get added back to the stock of available rooms, but March’s drop was just too big. Used Cars’ decline (-0.53%) surprised some people, because the private surveys showed that prices advanced last month, but the seasonal assumption was a decent hurdle this month that wasn’t cleared. However, if you were worried about how the spike in car parts tariffs would cause car prices to spike…because that’s what the news was hyperventilating about…you needn’t have. New Car prices were also slightly down, -0.01% compared to +0.1% last month.

As for shelter, it continues to flatten out, with Primary Rents 3.98% y/y and OER at 4.31% y/y. Actually, Primary Rents were flat on a y/y basis compared to the prior month, and have basically converged with our model, which is around 3.7%. From here we should expect very slow deceleration, but rents should stay above 3.25% or so on a y/y basis.

Supercore is looking great. This is about the best news in the report, because if Shelter is just about tapped out and Core Goods is trending just above zero we’d need Core Services to continue to dive.

That’s the good news. The bad news is that the spread of median wages over median prices has returned to its long-run average, which means that it will be hard to see additional sharp declines here…it isn’t going to come from squeezing wages further.

Outright, the Atlanta Fed Wage Growth Tracker – the best measure of wages in my opinion – is at 4.3% y/y. That’s right where it was in November. It’s going to be very hard to squeeze services prices lower if wages don’t decelerate further.

Finally, let’s circle back to pharmaceuticals. I’m going to point you again to my article from 2020, which is the first time that the President mooted the idea of a Most-Favored-Nation clause affecting the pharmaceutical industry. https://inflationguy.blog/2020/08/25/drug-prices-and-most-favored-nation-clauses-considerations/ The upshot is that even if the MFN policy takes place exactly as the President states, retail drug prices are unlikely to decrease anything like as much as he has said. In fact, there could even be some circumstances in which drug prices rise because companies stop selling in foreign countries at levels lower than in the US (because they face a more-elastic demand there) but which contribute to the total profit of the drug company. There may be others in which the drug company stops selling the drug at all in the US. Furthermore, drug prices overall have only risen 7% since pre-COVID, compared to 23% for core prices generally (the black line in the chart below is the overall CPI for Medicinal Drugs; the blue is the core CPI price level – both normalized to December 2019).

By the way, if I was concerned about importing APIs from China and wanted the US to start producing more of them, I don’t think I’d be trying to crush end-product prices and reduce the incentive to spin up production of the APIs. So there will be a lot of exceptions to the MFN policy, and you can tell from the performance of pharma companies yesterday after the news (big up with the market, not down!) that investors don’t expect any important impact on the bottom lines of pharmaceutical companies. I agree. I think Medicinal Drugs going forward will probably decline a bit for some celebrated cases, but not in a big way that pushes CPI lower significantly.

The big conclusion here is that inflation continues to run at about 3.5% or so (Median), and there is no sign of a significant further deceleration to come. As long-time readers know, this has been my theme for a couple of years, that we will end up in the ‘high 3s, low 4s’ on median inflation, because the overall backdrop of deglobalization and demographics argue for a higher floor. If the Fed keeps money growth very low, my opinion could change (and I’d already amend my target to ‘mid to high 3s’ as the mode), but I am not very optimistic on that.

However, I also don’t think there is anything about the inflation picture that argues the Fed has a lot of room to drop rates significantly. I said last month “The right answer to uncertainty from a policymaker perspective is to increase the hurdle for taking action. The right answer is to make no changes to policy. I am not confident that the Federal Reserve will correctly separate the ‘price of risk’ effect from the ‘economic growth’ effect. They are correct to note that tariffs by themselves are not inflationary in that they are one-off effects. If they believe that, and they think there’s a big recession coming, they’ll cut rates. That would be a mistake, especially given the uncertainty.” I still think that’s the case. At the moment, there is no reason to cut rates any further than the ‘let’s help Biden’ cuts did, except to appease the President and I see little urgency from this Fed to do that. I wouldn’t expect any big moves from the Committee, any time soon.

One final announcement. If you’re an investor in cryptocurrencies (in particular, stable coins) and have a Telegram account, consider joining the read-only USDi_Coin room https://t.me/USDi_Coin where the USDi Coin price is updated every four hours or so…and where these charts are also posted shortly after CPI just as I used to do on Twitter before they changed the API to make auto-tweeting charts very difficult.

Inflation After 100 Days

It is hard to believe that a third of the year is already past. Some people, of course, would say that it seems like a hundred years have passed in the first hundred days of Trump’s second term, but to me it seems like a blink.

Here’s a quick mark-to-market summary of where I think we stand with respect to inflation and the economy generally…after which I actually have another point for this column:

Uncertainty. That’s the watchword, of course. One place this shows up is in the huge spread between survey data and hard data. The survey data is tinted with fear of uncertainty, and is very negative (and likely influenced by the media deciding that Trump’s Administration signals the End of Days); the hard data is clearly softening but not dramatically so – and frankly, that was already under way in some ways since at least 2023 when the Unemployment Rate started heading slowly higher. In my view the softening of the hard data won’t ever get to be dramatic in this recession, and this will end up being more like a garden-variety recession we used to have pre-2000.

Inflation will be higher than it would otherwise be, because of tariffs, but lower than many people think because people greatly exaggerate the effect of tariffs. Tariffs only affect goods, and only significantly if they are goods facing inelastic demand. There will be some shortages in the near-term, and unlike during COVID when many of the shortages were caused by too much demand induced by money-drops to consumers, in this case it really will be supply constraints. Look out for things like ibuprofen, which is 90% sourced from China which makes it hard to completely switch supply to domestic suppliers. But these are short-run or in some case medium-run disruptions as supply chains shift. As domestic or lesser-tariffed countries replace the highly-tariffed suppliers, the supplies will respond and prices will come back down – not all the way to where they were, but it will feel like deflation in some cases because we mentally refer to the most-recent price, not to the year-ago price.

But either way, the tariffs are a jump-discontinuity, a one-time effect. The uncertainty, less so but that will fade (as an aside, and as I’ve noted previously, the high uncertainty had the effect in Q1 of causing money velocity to decline very slightly for the first time in a couple of years). By the end of the year, things will be much more settled and inflation will be stabilizing again…but the story continues to be that inflation will stabilize in the high 3s, low 4s, not at 2%. This probably means the Fed will not be easing much, although if there is a significant slowdown not caused from net trade – the Q1 drag was significantly from the surge in imports due to front-running tariffs – the Fed will ease even if inflation hasn’t come down. They’ll point to tariffs being transitory, although I sincerely doubt they will use that word! And they’ll be right, but they’ll also be wrong. Money supply growth is still too fast to accommodate 2% inflation especially in a deglobalizing world.

We’ll talk more about all of these things in columns here and in my podcasts over the next few months. But today I am still very preoccupied with getting USDi[1] launched, getting investors involved, talking to crypto ecosystem providers, etc. And I want to address one question I get routinely these days – not just about USDi, which exactly tracks CPI but adds nothing on top, but about the underlying investment strategy that I’ve been running/marketing for 3.5 years. The question is, “why should I buy something that returns CPI when inflation is at 3% and I can buy Tbills and earn 4.25%?” Here are two important pieces of the answer – and they’re just as important to investors who operate wholly in the traditional finance world as it is to people operating in the crypto world.

The first part of the answer is that while Tbills are above inflation now, that is not exactly guaranteed. In fact, for the last quarter-century it has been fairly unusual.

Sure, if you go back to the 1980s and early 1990s, when inflation was high and coming down and the Fed was following inflation down, you can find a lengthy period when Tbill rates were above inflation. Is the current period, with inflation where it is, comparable to the period when inflation was descending from double-digits and the FOMC was dominated by hawks? Do you think Trump will replace Chairman Powell and other Fed governors whose terms expire, with hawks? It doesn’t seem that way to me. I think it’s important to realize that is the bet you’re making, if you hold short cash instruments as an inflation hedge.

The second part of the answer is that holding a cash instrument does not protect you during an inflation spike because the Fed cannot respond fast enough, and a cash instrument in nominal space does not protect you from a dollar crisis. Almost nothing does, in fact, as stocks and bonds both do poorly in those cases as do ‘inflation hedge’ products based on equities or bonds. Here is a chart of the recent inflation spike. How well did your Tbills, or short-duration bonds (VTIP) or long-duration inflation bonds (TIP), keep up? Did they ever catch up?

To me, any allocation to low-risk securities that is meant to serve as a volatility buffer for a portfolio, but does not hold inflation beta, is completely missing the value of that beta in certain scenarios where very little else is helpful. When inflation spikes, stocks and bonds become correlated (down). You can (and should) add commodity allocations to your portfolio, but those consume part of your risk budget and push out the equities, hedge funds, private equity, and other higher risk asset classes. If you can get the inflation beta from a very low-risk part of your portfolio, you ought.

The foregoing is, transparently, partly self-serving. But the products I’ve been involved with developing have never been developed because they produce big fees or are easy to sell.[2] I’ve developed them because they’re useful to investors. And, parenthetically, I do think that the worker is worthy of his wages.

If you want to find out more about USDi, I urge you to visit the home page https://usdicoin.com, where you can see the current value of the coin increasing minute-by-minute with inflation. If you’re a denizen of the crypto world, then you might also be interested in joining the Telegram read-only group for the USDiCoin, available at https://t.me/USDi_Coin. That group is where we will make announcements about the coin, post the price of the coin periodically (at least daily; automation in process), post the monthly reports confirming the collateralization of the coin, announce new market-makers and markets…and also post some inflation-related charts, such as I used to do on Twitter on CPI morning, when Twitter allowed such automation. If you’re at all interested in inflation and/or the inflation-linked coin, hop on.

[1] If you don’t know what USDi is yet, read my prior article https://inflationguy.blog/2025/04/15/announcing-usdi-inflation-linked-cash/

[2] Understatement of the century.

Announcing USDi…Inflation-Linked Cash

As many of you know, one of my goals in life – for decades – has been to expand the inflation-linked investing ecosystem to other structures (e.g. options), other legs of the liquidity triad (e.g. cash, swaps, futures), other more-specific inflation (e.g. medical care), and in every other way I could. Barclays originally moved me into the US CPI Derivatives seat not because they thought I’d be a tremendous trader (there was nothing to trade) but because they thought I’d be a good evangelist for the product. I’d like to think they were right. Certainly, I’ve been a durable one.

Over the years, through my time at Barclays and Natixis and Enduring, I’ve developed a lot of structured products – some which traded or were issued, but a lot that died on the drawing board or for lack of customer demand – and trading/hedging methods, funds, models, etc. But nothing, I think, is as impactful as what we’re announcing today. Because what we (at USDi Partners) are announcing is likely to be considered a security, I have to be somewhat careful about how I discuss this product. So, I am just going to post the press release, and let it speak for itself for now…although I would be remiss if I did not also refer to Elizabeth Stanton’s excellent article on Bloomberg (subscription required).

***

USDi Partners Notes Launch of the USDi Coin, the First US Currency to Permanently Preserve Purchasing Power

Basking Ridge, NJ – April 15, 2025

USDi Partners today launched its first cryptocurrency project, which will allow investors to hold an asset that is permanently linked to the purchasing power a US Dollar had in December 2024.

The coin (an ERC-20 token on the Ethereum blockchain) will be available to accredited investors from market making firms that have passed USDi Partners’ AML/KYC process and are able to mint or burn the token directly. Once an investor buys a USDi coin with ‘normal’ dollars, the value of that coin will rise every day on the basis of the increase in the Not-Seasonally-Adjusted US Consumer Price Index for Urban Consumers, calculated and released by the US Bureau of Labor Statistics, which is the same index on which trillions of dollars’ worth of U.S. TIPS bonds are based.

A Coin that Always Buys What a Dollar Buys Today

Holding the USDi Coin will effectively be the same as holding a dollar whose purchasing power rises as the cost of goods and services increases. If the US CPI index rises 10% from the launch date, the value of a USDi Coin will be $1.10 in terms of the current dollar, so that the investor’s purchasing power is undiminished. “The idea for USDi was inspired by the Chilean Unidad de Fomento (UF), a non-circulating currency that since 1967 has been indexed to the price level in Chile. The UF is often used as the basis for contracts in Chile, allowing counterparts to agree on terms without worrying about how inflation will change the significance of the sums exchanged,” explained Michael Ashton, Co-Founder of USDi Partners. “But, unlike the UF, the USDi Coin will actually circulate.”

The USDi Coin is collateralized by reserves that are managed by an inflation-hedging specialist to keep up with inflation in both the short- and long-term. The Coin itself, however, will not fluctuate on the basis of investment returns but will always track US CPI exactly. (Because of the public release schedule of the CPI, the value of the USDi Coin on any given day will always be known from 2-6 weeks in advance.)

The CPI index on which the USDi Coin is based is calculated according to a publicly-available handbook of methods and released publicly, along with hundreds of subcomponents and regional indices, on the website of the Bureau of Labor Statistics. This makes it ideal for Phase 2 of the USDi project.

Finally, Medical Inflation (and Other Things) Will Be Investible

In Phase 2, the USDi Coin will become splittable, so that an owner of a USDi Coin will be able to divide it into subcomponents that track the inflation rate of individual parts of the consumption basket, and trade them separately. For example, upon the launch of Phase 2 it will be possible for the first time ever to invest in Medical Care CPI directly. This is an innovation beyond just crypto, says Andy Fately, Managing Partner and Co-Founder of USDi Partners. “What you have never been able to do before, but will when we launch Phase 2, is to buy a collateralized coin to track Medical Care or College Tuition inflation explicitly. This hasn’t even been done in the Trad Fi world, but the low frictions of the crypto world make it the ideal venue for this breakthrough.”