Time to Choose Your Inflation Adventure with Velocity and Money

We have CPI coming up in a few days, but M2 came out recently and it is worth commenting about, so let me drop some thoughts about the state of money and velocity right now and the context we are operating in.

M2 grew 0.88% in February, causing the y/y change to rise to 4.88% (quarterly, however, it is 6.65% annualized). I saw somebody recently observe that money growth was about 6ish back before COVID, so this level is not very worrisome to that pundit. I think that’s wrong – not that this level is worrisome in the big picture, but the trend is bad and the current level is actually not consistent with low and stable inflation as it was prior to the late twenty-‘teens.

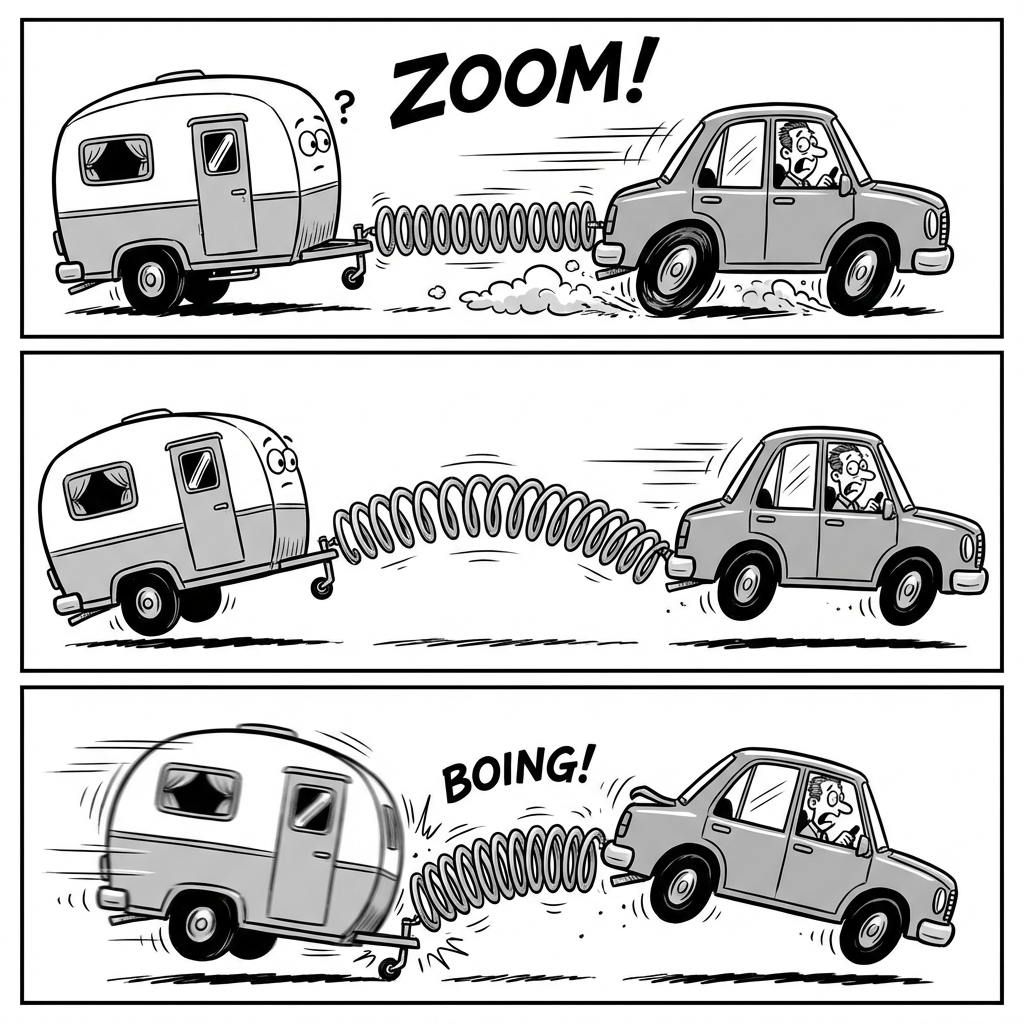

Before we get to that, let’s review the state of play for money velocity. Remember when velocity plunged early in COVID, and people said inflation wouldn’t happen because the transmission mechanism was broken? That comment was so funny it made me blow milk out of my nose, even though I wasn’t drinking milk. It was entirely an artifact of the different time frames over which the money supply was changing, compared to the time frames required for prices and output to change. MV=PQ, and M was changing suddenly. Since GDP can’t suddenly change 20%, money velocity became the capacitor that held the excess charge which slowly bled into prices. In my podcast, and occasionally in this blog, the image I shared was of a car rapidly accelerating away from a trailer hitched to it by a spring. At first, inertia keeps the trailer from traveling as fast as the car, and the spring stretches. Once the car stops accelerating, though, the spring compresses and the trailer catches up. The illustration below is courtesy of Lovart.ai.

So where are we? Here is the US monetary system over the 2019-2025 period showing total growth from December 2019. The x-axis shows the total percentage growth in money as a percentage of real output (M/Q). The y-axis shows the total change in the price level. Now, I have to point out that when I was talking about this, in 2021 or 2022, we were very far away from the diagonal line showing where the two changes are equal. And I said we would be going back to the line, and we went back to the line. People really ought to listen to me more.

The other way to look at this is that velocity is back almost to where it was prior to COVID.

So is there any problem here? Velocity is back to where it was, but if it’s stable and money is growing at 4.9% y/y, then P+Q grows at 4.9%, so 2% inflation with 3% growth…sounds pretty good.

This is where we review the “but 6% worked!” argument.

You can see from the chart that yes, since the late 1990s M2 grew at 5-10% and we never had much of an inflation problem. Why now? Well, during that period velocity was steadily declining – and that is the only way that you can sustain 6% money growth with 3% real economic growth and get 2% inflation. The question, then, was why velocity was declining. Remember, some people think this is a trend, because they don’t really understand what drives velocity. During that period, interest rates steadily declined. This was also a period of increasing globalization and a demographic dividend (more workers relative to the aged). Now, whether the interest rates declined because of those trends because both trends were disinflationary, or if interest rates declined because of a dovish Fed and they only got lucky because of those trends…I don’t know. But the point is that the largest driver of lower money velocity during that period was lower interest rates.

And interest rates are now approximately fair. Some people think they’re too low with inflation too hot, some people think they’re too high with economic growth seeming to slow, but let’s just say they’re not 300bps wrong at this point. Here is our velocity model. With lots of crazy volatility, it has velocity pretty close to on-target. Here’s the problem: the last time prior to COVID were as high as they are now (I’m looking at 5y Treasuries), it was also prior to the Global Financial Crisis and the regime of interest rate repression. Back in 2007, 5y rates were this high, and money velocity was about 2.0, some 40% higher than here. What is holding velocity down right now in our model is a very high level of economic policy uncertainty, which causes people to hold more cash than they otherwise would given the level of interest rates. Thanks to the war between the President and his allies on one side, and the minority party on the other side, not to mention the Iran war, there is a lot of uncertainty right now and that is causing people to conserve cash.

It won’t always be that way, but with M2 growing near 5%…it really needs to be that way. By the way, the money growth situation is a bit worse than it looks, too: there has in the last couple years been a fairly dramatic rise in the amount of non-M2 money that is growing in defi/crypto space. Bitcoin isn’t money, but stablecoins are very much like money. The scale of the Stablecoin money supply is small compared to the ‘off-chain’ money supply, but it is starting to get large enough to matter. Anyway, we know the sign of that growth, and it’s a big fat plus.

So no, 6% is not a stable rate of money growth going forward from here. This is not the early 2000s. It is not the 1990s. If we could manage to just have 6% growth, then we’re probably going to end up being in the mid-to-high-3s on inflation, and that’s tolerable. But if that’s the midpoint of money growth, then mid-to-high-3s is the midpoint on inflation with some periods a little below that and some periods a little above that.

Economies adapt, and an economy can work fine at 4-5% inflation or even higher as long as it is stable. But 4% inflation feels different than 2% inflation, and the economy will work differently in that sort of regime. Businesses will be more likely to pass through cost increases rather than absorb what they think are short-term variations (see “How Expecting Inflation Un-anchors Manufacturers’ Pricing Strategy”). Equilibrium equity prices are lower. Menu costs and search costs go up. And so on. We may already be seeing some of these long-term structural changes. The Fed just published a FEDS Notes entitled “Is the Inflation Process in Advanced Economies Different After the Pandemic?” The short answer? Yes it is. The question is, are we on track to get the inflation process back to the way it used to be? And the answer there appears at this juncture to be: no.

Inflation in One Easy Lesson

For Christmas, my daughter gave me the pamphlet “Inflation in One Easy Lesson,” by Harry Scherman. (Yes, I am that typecast that my daughter gives me inflation memorabilia for Christmas!) It was written during World War II, and distributed by the Council for Democracy. It is so delightfully simple and direct, and makes the main point so obvious, that I want to share it. It also happens to be, given the current war against Iran, somewhat timely. Here is the cover:

I scanned the whole pamphlet into a pdf, after ascertaining with some confidence that the pamphlet is no longer under copyright as there is no sign the copyright was renewed after the initial period of protection. If you believe yourself to hold a copyright on this material, please contact me at inflationguy@enduringinvestments.com and I will remove the post.

Here is the 22-page pamphlet. Frankly the pictures are wonderful by themselves, even without the text!

Inflation Guy’s CPI Summary (February 2026)

It’s going to be hard to get too jazzed about today’s CPI report. Because it is entirely a pre-Iran-war number, it won’t have any of the energy spike that will make next month’s figure so exciting/alarming. Now, ordinarily I’d say that this will be the last ‘clean’ number without those influences, but this number isn’t in any sense clean because there are still echoes of the shutdown in it. Still, the fun part of those echoes will be in April’s number when the rent figures will have a one month spike as the October OER sample (all zeroes by assumption) drops out of the calculation. And that month will have Iran in it also. So buckle up for the next couple of months.

For February’s figure, though, the expectations were for +0.26% on headline inflation and +0.24% on core. Right around 3%, and not representing a return to the Fed’s target, but not too far off – except for the fact that it looked like they were on the upswing even before the Iran thing. Will anyone care?

Now, the US CPI swaps curve does have the influence of the war in it. But I present it here because it’s interesting. It isn’t surprising that it is inverted, with the near-term inflation higher due to energy, but the long end lower? That looks odd. But I’ll circle back to this later as it is actually a good reminder.

Also interesting, by the way, is the following chart of 5-year inflation swaps in several theaters. It is interesting that despite the wild ride in energy, US 5y CPI swaps haven’t moved very much – and certainly less than elsewhere. That’s partly because the US is less sensitive to oil prices than some other economies but also because the dollar has tended to be positively correlated with oil prices, dampening the direct pass through. It still looks like a lot to me, though. This is a 5-year tenor so also surprising that it moves that much with spot energy being the main source of volatility.

With those preliminaries, let’s look at the actual data.

The forecasts were pretty good: actual headline CPI was +0.267% while core was +0.216%.

The Apparel price spike is odd, but these happen from time to time and it’s a small category. The rise in Medical Care, which was mostly Hospital Services, was mildly discomfiting but on the other hand shelter was soft.

Core services and core goods both softened y/y. Core goods is at +1% y/y. The downward hook is expected, but the real question is whether it settles at +0.5% or -0.5%. I’m betting 0.5%. Still, it’s good news.

The singular surprise/miss was in Primary Rents. Owners’ Equivalent Rent was +0.22% m/m, about the same as last month and drifting lower y/y (although that will change in a couple of months when the OER sample rolls out the October zeroes). But Rent of Primary Residence was +0.13% m/m.

Clearly the trend is lower, but the sharp break (probably retraced somewhat next month) is quite surprising given the upward cost pressures on landlords. I suspect there are some big compositional changes here – rents possibly under pressure in big cities where reverse immigration flows are relieving pressure on the housing stock, and possibly some effect from NYC’s outmigration as well. I will have to dive into the details to see. But not right now.

Lodging Away from Home was +1%. This has been recovering from the dip last year but hotel prices are still below the post-COVID “gotta get away” highs. It’s a decent bet that we will see new highs here in 2026.

Airfares were also up, +1.4% m/m. Keep an eye on this. With energy prices going up, this is a fairly direct passthrough. Not this month, which is for February, but if jet fuel prices remain elevated then airfares will go up (and that ‘looks’ like core inflation even though it really isn’t).

The red dot is end-of-February numbers. But currently, Jet Fuel is at $3.49…it was at $4.11 just a couple of days ago. This will show up in airfares next month.

Let’s look at ‘supercore’, core services ex-shelter. Last month, supercore was +0.59% m/m; this month it’s “only” +0.35% m/m. Right now, on a y/y basis, Core Services ex-Rents is 2.94%, but that will jump next month as we are rolling off a very weak figure from last March. That’s when we had Airfares -5.27%, Lodging Away from Home -3.54%, and Car and Truck Rental -2.66%. That’s all dropping off, so next month we will see a rise in y/y supercore even if the m/m figures are soft. And they won’t be.

The distribution of price changes overall this month is interesting. There were a number of categories that rose less than 1% on an annualized m/m basis, but most of them not by very much. (The red text indicates the change is based on my estimate of the seasonality rather than the way the Cleveland Fed does this.)

There were also a lot of upper-tail categories, but the upper tails are longer. Of course, Median CPI (I don’t trust my estimate this month but I think it will be soft, probably less than 0.2%) doesn’t care how long the tails are. That’s the point of median.

So normally, median is comfortably above mean CPI because for a long time we have been in a disinflationary regime where tails were longer to the downside (aka negative skewness). This month that might not be true. I’ve written about this in the past: in inflationary cycles, long tails are to the upside so mean tends to be above median. But this is just one month and I’m not going to read too much into it yet.

On Fed policy: given what has happened in March, the February numbers aren’t going to be very meaningful. But the market seems to be misunderstanding the importance of the energy spike, treating it as an inflationary impulse that makes the Fed’s job difficult given weak employment data. That’s wrong. A rise in CPI that is caused by energy is not the sort of inflation the Fed leans against. That’s because energy is mean-reverting, but also very anti-growth. Remember that earlier I noted that the CPI curve was inverted but also the longer tenors were lower than a month ago? That’s probably because the inflation market is pricing a recession (which isn’t disinflationary, but the market believes it is). Anyway, if the Fed tightened into an energy price spike, they’d be making a recession worse. That was a big part of the 1970s Fed errors. The Fed knows about those errors, and so an energy price spike is more likely to produce a Fed ease in context with weak employment data, than a tightening. This isn’t stagflation, if core continues to decline. It’s stag, but headline CPI heading higher is not inflation if core/median remains tame.

(To be sure: I don’t think core and median are going to remain contained and in fact I think they are already starting the process of rolling back to the mid-to-high 3s. The Enduring Investments Inflation Diffusion Index is confidently moving higher.)

(But the Fed doesn’t believe that. We could well end up talking about stagflation properly but people will still get confused with the headline spike. Sigh.)

Here’s another important implication: given what has happened in March, the February numbers aren’t going to mean much for policy, so people will move on quickly from this especially as they were close to expectations. But, the NSA increase this month was +0.47%, so that is what matters for USDi. In March, USDi will increase 0.37% (4.5% annualized). In April, it will increase +0.47% (5.8% annualized). And here’s the thing: right now the inflation swaps market is pricing March CPI at +0.91% NSA…if that happens, then the May USDi increase will be at an 11% annualized rate…

The bottom line for this report is that February’s number is going to be swiftly forgotten. The next few are going to be very exciting, and not in a good way!

Profiting From Zero Duration Inflation

One of the nice features of the USDi digital currency is that its path is known with certainty well in advance. The price of USDi is determined by the interpolated CPI index value compared with the value on the reference day (315.605). So, for example, we know that today’s[1] USDi value is 1.02681 because today’s CPI index value is 324.06614, and we know that because we know how to interpolate between the CPI prints from 3 months ago (324.122) and 2 months ago (324.054).

Importantly, those numbers we are interpolating between are the Non-seasonally-adjusted CPI figures from December (released in January) and January (released in February). And that interpolation methodology is exactly the methodology that TIPS use.[2]

You will notice that the CPI from 2 months ago is lower than the CPI from 3 months ago. That means that prices actually fell, before seasonal adjustment, which means that USDi actually declined slightly over the course of the month. It was even worse in January, because the November CPI was – as I have noted before – complete garbage due to the fact that BLS procedures led them to assume zero inflation for a lot of the missing October data. In the chart below, you can see the sharp correction during which USDi actually declined during January (and slightly further, in February).

Now, because we can ‘see the future’ due to the interpolation mechanism, we know exactly where USDi will trade each day in March. That’s also indicated on the chart. So we know that in March, USDi will rise at a 4.53% annualized pace. One-month t-bills are 3.6% right now. You do the math.

It gets better: the same BLS procedures that led to the terrible November number lead to self-correction, so the CPI Index will catch up over time. The biggest part of that catch-up is due to the rotation of the rent sample over 6 months, so while we do not know exactly what CPI will print at for February, March, April, and May, we have a good confidence that it will be above trend. We can see that from the CPI “fixings” market where those particular CPI prints trade. The market price is the market price, and sometimes wrong, but based on what trades in the market right now we can anticipate (orange line above) that USDi will climb at an annualized rate of 5.63% in April and 5.53% in May before slipping back to a still-better-than-bills 4.17% in June.

What does any of this have to do with duration?

Well, you may read this and say to yourself “I can get the same benefit if I just buy short TIPS bonds.” But no, you can’t. That’s because when you buy a TIPS bond, the principal amount rises with inflation but you still have to deal with price. It turns out that TIPS traders are very aware that their accretion (what we call the uplift in principal) is going to be higher than TBill rates over the next few months, and so the current price of TIPS bonds fully discount this. The July 2026 TIPS, which will mature at the CPI index value of July 15th (which is interpolated between April’s CPI and May’s CPI, so it includes all of those rebound months), trades at a price of 100-13…and remember, it matures at 100. So you’ll gain the accretion, but lose on price. I’ll save you the math: that price means the real yield of that bond is about -1%, which is convenient since the CPI between now and then is going to be something around 1% higher than the Tbill yield.

Every day that passes, as the principal value of the TIPS bond accretes, the price will decline. The only way you can profit versus fixed-rate Treasuries is if you are smarter than the market, and your forecast of CPI is better than what is already embedded in the price of the bond.

USDi has a price, but it is completely insensitive to yields which means you do not have to pay a premium to buy it now (nor did you get a discount back in December knowing the bad January numbers were coming). You can buy USDi today knowing that you will earn those exciting forthcoming CPI prints, without sacrificing principal.[3] You can buy USDi against USDC on Uniswap, or simply go to https://usdicoin.com/mint.

I’ve told you before how interesting USDi is since it’s the zero-duration instrument. Here is another concrete example.

[1] I say “today’s” because I am illustrating all of this with daily interpolation, but in practice USDi interpolates every block or “hash,” which is just a few seconds in length.

[2] …except for the fact that TIPS interpolate daily and USDi almost continuously.

[3] Of course, this is not investment advice. Although it sure sounds like it. Do your homework!

Inflation Guy’s CPI Summary (January 2026)

Let’s start by setting the context for today’s CPI number.

A couple of months ago, we missed a CPI because of the shutdown. The BLS simply didn’t have any data to calculate the October 2025 CPI. That wasn’t the real problem. The real problem was that the BLS’s handbook of methods more or less forced it, in calculating the November CPI index, to assume unchanged prices for October for some large categories – in particular, rents. This caused a large, illusory decline in y/y inflation figures. Importantly, this was also temporary – there has been some catch-up but the big one comes in a few months when the OER rent survey rotation will cause a large offsetting jump in that category, exactly six months after the illusory dip. Until then, inflation numbers will be more difficult to interpret and the year-over-year numbers will be simply wrong. So when you read that today’s figure resulted in the “smallest y/y change in core inflation since 2021, and consistent with the Fed reaching its target” – that’s just wrong. The true core y/y number is roughly 0.25%-0.3% higher than what printed today. The CPI ‘fixings’ market is currently pricing headline CPI y/y to rise to 2.82% four months from now, and that isn’t because of a coming rebound in energy prices.

I guess what I am saying is this:

Ladies and gentlemen, please take your seats. We will be experiencing some mild turbulence.

January, in general, is already a difficult month in CPI land because of the tendency for vendors of products and services to offer discounts in December and then implement annual price increases in January. But those price increases are not systematic, which means they are difficult to seasonally-adjust for. Ergo, January misses are rather the norm.

So with that context, the consensus estimates for today’s number were for +0.27% m/m on the headline CPI, and +0.31% on core. Some prognosticators were quite a bit higher than that – I think Barclays expected +0.39% on core CPI. The question was basically whether there is still any tariff increase that needs to be passed through; if so then January is a good time to do it. That didn’t really happen. The actual print was +0.17% on headline and +0.30% on core.

The miss on headline happened because while gasoline prices actually rose in January, the average price in January was lower than the average price in December – because in December, gasoline prices dropped sharply. While Jan 31 gas versus Dec 31 gas was $2.87 vs $2.833 (source AAA), January 1 vs December 1 was $2.83 vs $2.998. So, even though gasoline prices rose over the course of January compared to the end of December, that’s now how the BLS samples prices.

Be that as it may, core inflation was pretty close to target. One way to look at it is that y/y Core CPI, at 2.5%, is the lowest since March 2021. Another way to look at it is that the m/m Core was the third highest in the last year, and annualizes to 3.6%. So is it ‘mission accomplished’ for the Fed? Erm, nothing in the chart below tells me inflation is trending gently back to 2%. You?

The core number was actually flattered by a large drop in used car prices, -1.84% m/m. Used car prices actually rose in January, but less than the seasonal norm so that resulted in the large drop and that caused a meaningful drag. (Let’s not get in the habit of just dropping everything that doesn’t fit the narrative, though.) Anyway, core goods as a whole dropped to 1.1% y/y from 1.4%, while core services eased to 2.9% y/y from 3.0%.

While core goods fell more than expected because of that Used Cars number, it’s not surprising that it is moderating some. The question isn’t whether core goods prices will keep accelerating to 3% or 4%; the question is whether it stays positive, or slips back to the negative range it inhabited for many years. That’s an important story even though core goods is only 20% of the CPI. Until now it has been a ‘tariffs’ story, but going forward it’s an ‘onshoring’ story. My contention is that we should not expect a return to the persistent goods deflation that flattered CPI for a generation thanks to offshoring of manufacturing to low-labor-cost countries, because the flow is reversing. That is the story to watch, but it isn’t January 2026’s story.

While we are talking about autos, I’ll note that New Cars showed a small increase. I wonder (and I don’t have a strong forecast here) what the changes in car sales composition now that electric vehicles are no longer being pushed by the executive branch. Obviously non-electric cars are cheaper, so if we had a real-time measure of the average sales price of a car it would probably fall as consumers go back to buying cars they want instead of cars that look cheaper because of tax breaks. I don’t know though how much actual sales will change (auto production will certainly change as carmakers no longer have to check the box by making a certain number of cars that were hard to sell), and I don’t know how detailed the BLS survey is and whether it takes into account fleet composition. I guess we know that if there’s any effect, the sign should be negative. I suspect it is a small effect.

Turning to rents, as we do: Owners Equivalent Rent was +0.22% versus +0.31% last month. Rent of Primary Residence was +0.25% vs +0.27% last month. The chart below shows the m/m changes in OER… except that it does not show the 0 for October. There’s clearly a deceleration here, but my model says it should be flattening out right about at this level. Also not January 2026’s story, but it will be 2026’s story.

There was a small decline, -0.15% m/m, in Medicinal Drugs. Some folks had been eagerly waiting for that to show a large drop, thanks partly to the Trump Administration’s efforts to force drug manufacturers to align prices in the US market with prices in the ex-US market. There is not yet any discernable trend. Potentially more impactful is the Trump RX initiative, which by bringing transparency and cutting out the middleman in the really-effed-up consumer pharmaceuticals pipeline (dominated by three big wholesalers and three big pharmacy benefit managers, each of which is highly opaque about pricing) could well cause a significant decline in consumer-paid drug prices. But…remember that when those drugs are paid for by the insurance company, it isn’t a consumer expense and only shows up indirectly in the CPI. Yeah, that makes my head spin also. Bottom line: pharmaceutical prices are likely to decline some for consumers, but we just aren’t really sure where that will show up in the CPI and how soon it will happen.

The best news in the report today is the continued deceleration in core-services-ex-rents (‘Supercore’), which decelerated even with Airfares being +6.5% m/m.

Psych! You fell victim to one of the classic blunders! This is again a y/y figure that is flattered by the lack of October data. On a m/m basis, supercore had the biggest jump in a year, +0.59% (SA). Still, I think this is decelerating along with median wages deceleration. Of course, all of that data is messy right now as well, but the spread of median wages over median inflation remains right around 1%.

There is some early evidence that the downward slide in wages might be leveling off; if it does, that will limit how fast supercore can moderate. There are also some cost pressures in insurance markets that are probably going to show up in the next 6 months or so. But that’s not January 2026’s story.

The story in January 2026 is that the waters remain muddied by the government-shutdown-induced gap. The current y/y figures are all flattered by that event, and exaggerate how good the inflation picture is. That’s how the Administration can trumpet victory while the reality on the ground is that inflation is not converging to trend.

I’m working on the assumption that the Fed knows this, and the combination of core inflation that seems steady around 3.5% (abstracting from the shutdown gap), better-than-expected labor market indicators, and a distinct animus among current Fed leadership towards the President means that there’s no reason to expect an adjustment in overnight rates any time soon. Frankly, I think the argument is better for a rate increase than a rate decrease. On the other hand, rents do appear to be continuing to decelerate even if we ignore the October gap. My model says that isn’t going to continue, and even if I’m wrong I’m likely to be closer than the folks calling for deflation in housing. And moderation in Supercore is encouraging, even if – again – I don’t think that continues to the point the Fed needs it to be. Core goods inflation appears to have peaked, and the question is whether we go back to core goods deflation or not.

In each of these cases, my modeling suggests that the current level of median inflation of around 3.5% (ex-gap) is likely to end up being an equilibrium-ish level. But it isn’t ridiculous to look at the current trends and see good news on inflation. Either way, there’s not a Fed ease coming imminently. But if those trends continue until Warsh is confirmed and becomes Fed Chairman, there could be a rate cut later in the year.

But that’s not January 2026’s story.

My Quick, Early Opinion About the Warsh Nomination

Before I tell you what I think about Trump’s nominee for Fed Chairman, Kevin Warsh, I should first confess to the fact that my opinion of Chairman Powell has changed several times since he was first nominated. That’s a user-beware warning about my thoughts below, but it’s not just about me. I’ve watched the Fed since about 1990 – I wrote a book leaning against the perception of Chairman Greenspan as some kind of “Maestro” – but what happens when individuals meet institutions is that both are changed. The classic example is that Presidents always govern closer to the middle than their campaign rhetoric, but it is a general rule.

In Powell’s case, I was initially very optimistic. Powell was a non-economist, the first such to have led the Fed since G. William Millers’ brief tenure prior to Volcker. “Maybe,” I thought, “Powell will be less likely to automatically buy into the assumptions of the poorly-performing models the Fed has used for the last few decades, and move away from them. My opinion fairly quickly shifted once he became Chairman and made it abundantly clear that he had basically learned everything he needed to know about monetary policy from the existing staff at the Fed. Total regulatory capture, in other words. And he moved too slowly when COVID hit and it was very obvious that inflation was going to spike given the government’s efforts to keep demand strong with lots of money, while supply had collapsed. He was totally Team Transitory, and totally wrong.

But then, the Fed actually started raising rates, and raised them far more than I thought that a traditionally-dovish institution was going to. My opinion of Powell rose again. Yes, it was exactly inverted to the right approach – instead of raising rates and letting the balance sheet stay large, he should have kept rates low and slashed the balance sheet – but he at least thought he was being hawkish. My opinion of him took a final turn lower, when his Fed made nakedly-political interest rate moves in the runup to the 2024 election.

In the end, I rank Powell well above the disastrous Yellen and the disconnected-from-the-real-world Bernanke, but below Greenspan. Indeed, while I don’t think Greenspan was any part of a “Maestro,” and he changed the Fed in some incredibly damaging ways (making it far too transparent)…I feel kind of bad in retrospect for my book since his three successors have all been worse.

Anyway, that is a long prologue but let’s face it, we have far more information about Powell than we do about Warsh. I want it to be a warning, though, about the fact that whatever I/we think today about Warsh, we should let his future actions inform our opinions!

So here’s what I think…and I am only telling you because some of you asked:

I think Trump could have done a lot worse than Warsh. While the President regularly confounds his critics by making solid decisions when they expect the ravings of a madman, this one surprised me too. For all his railing about how interest rates should be lower, and the Fed was moving too slowly, etcetera, he ended up choosing someone who is certainly on the hawkish side of the ledger…certainly with respect to the other people supposedly being considered.

Now, Trump isn’t wrong when he says the Fed did not manage the inflation spike or its aftermath very well. As I’ve said for a long, long time, managing inflation is about managing the money supply – and interest rates have nothing to do with inflation. I don’t think Trump is being this nuanced, but it’s the right answer: shrink the balance sheet, rein in money growth in other ways…and lower interest rates, because one thing we do know is that money velocity is influenced by interest rates. That’s how you get a non-inflationary boom, and it would be funny if Trump got there by accident. (Or…is it?)

But this is the way Warsh is supposedly leaning: near-term dovish, but hawkish on the balance sheet. Also important, as I alluded to earlier when talking about how the Fed has become more and more transparent: allegedly Warsh tends towards less communication about policy. If you want to de-lever the dangerously levered global financial system, a great place to start would be to decrease the predictability of monetary policy. More visibility = more risk taken, which increases systemic risk.

One of the things I hope for Warsh is that he ignores Bill Dudley’s advice, given today in a Bloomberg column. Dudley’s #1 piece of advice was “first, he has to win the confidence of his colleagues at the Fed. Although the chair directs the Fed’s staff and sets the agenda at each meeting of the policymaking Federal Open Market Committee, ultimately he has just one of 12 votes. To truly wield power, he’ll have to earn respect. He’s made this more difficult with his persistent criticism that the central bank needs “regime change” and that he might need to “break some heads.””

The incoming Chairman should completely ignore that. It’s nonsense and Dudley knows that. The power to set the agenda is the only power that matters – no Fed Chair has ever been even remotely close to being outvoted, and that’s partly because no Chair would ever call a vote he could lose. Dudley, and all Fed careerists, want to make sure the vast staff at the Eccles Building matters, and that the bureaucracy continues to be what actually sets policy. This is exactly what the President is complaining about, and he is not wrong!

The Fed doesn’t need to be “ended,” but it needs to be a lot more opaque and a lot more introspective about the historical incidence of Fed actions that caused harm versus those that caused good. It needs to be tighter on the balance sheet; overnight interest rates are roughly neutral but don’t really matter that much. At first blush, from my perspective, Warsh falls on the right side of those divides. Casting back to my earlier warning that I am willing and able to have my mind changed on this score as we learn more about the Warsh Fed, I will say at this point that I am pleasantly surprised.

The Dollar – Best House on a Bad Block

I’m here to draw your attention to something alarming happening in currencies at the moment. Here is a picture of the US Dollar, which has lost a huge amount of value in the past year.

Now, before certain ones of you get all excited and say that this proves Trump is ruining the dollar and forcing foreigners to vamoose out of the United States, take a look at the Euro.

I’m not going to tease you too much with this. The first chart is just the dollar in terms of ounces of gold; the second is the Euro in terms of ounces of silver. Don’t worry, longtime readers: I’m not about to go all gold-bug on you. I could have done those charts with almost any currency against a wide variety of commodities: the Bloomberg Commodity Index is up 23% since mid-August, and +12% since the end of the year. So this isn’t just a precious metals story, and it isn’t just a dollar story. It’s a fiat currency vs ‘stuff’ story.

The recent breathless coverage of the melt-up in precious metals seemed to me to miss the bigger point of what it means. It’s awesome if you’re long precious metals. But the abrupt turn vertical is – or should be – alarming. But nothing looks alarming when it’s pointed higher.

Treasury Secretary Bessent, as I write this, just came out and stated that the United States has a strong dollar policy and has not intervened (at least not yet) to push the dollar lower against the yen. That’s all very nice but I don’t worry a lot about the level of the dollar against other currencies in the medium term and here’s why.

Let’s look at the monetary pipes, which to me imply an increase in the dollar and/or a sharp increase in long-term interest rates regardless of what happens to overnight policy rates. (Many people are concerned about long-term rates because of some vague sense that we are borrowing too much or because everyone is going to sell their US bonds – to buy what with the dollars they receive, no one seems to mention – but there is a mechanical/accounting relationship could cause that outcome).

To this end, the illustration below (Source: Enduring Investments[1]) is a helpful visual guide. For this analysis we are interested in the flows of the dollar system, more than its stock. And the important flows are – or have been – pretty stable. The US has for a long time run a substantial budget deficit, which means the government needs to source dollars by borrowing them. The three sources of those dollars have historically been foreign investors, the Fed, and domestic savers. Foreign investors have extra dollars because the trade deficit means that Americans send more dollars to foreign producers than foreign consumers send to US producers, and those extra dollars are invested in the US into government bonds (spigot on the lower left) or otherwise invested in markets or direct investment (spigot on the lower right). The Fed balance sheet, over the last decade or so, has often been a supplier of dollars to the system when it has been expanding more often than not. Finally, there are domestic savers who buy Treasury bonds among other things (but consider that when they’re buying US stocks, for example, the dollars are just sloshing from one domestic saver to another – that’s why there’s no flow shown for domestic savers buying US stocks). Those three ‘suppliers of dollars’ are the top hoses filling up the barrel of dollars in the illustration below.

Those flows tend to reach stasis via automatic stabilizers. For example, if the government is draining more money (with a big budget deficit) than is being supplied elsewhere, then either interest rates rise to induce domestic savers to provide more money, or the trade deficit expands. My concern is that automatic stabilizers tend to take time to stabilize, and currently there are some big changes. See the next illustration and focus on the differences compared with the prior one.

The cessation of the expansion of the Fed’s balance sheet has been happening for a while, and the balance sheet has even been shrinking a little. But the Trump Administration’s trade policies have caused two major changes: first, the trade deficit has been shrinking sharply (see charts below, source Bloomberg; the first shows the net trade balance monthly and the second shows the recent trends of declining imports and rising exports).

Some of this may be ‘payback’ for the surge in imports at the beginning of the year by importers trying to beat the imposition of tariffs, but there seems little question now that the trade deficit really is closing substantially. At the same time, foreign companies have been tripping all over each other to start making substantial investments into the US. In the second ‘barrel of money’ chart above, note the spigot at the lower right is really gushing, and two of the hoses supplying dollars have slowed to a trickle or stopped.

If that’s a fair representation, then what are the implications? If those trends persist, then the demand for dollars is going to outweigh the supply of dollars, leading to two outcomes. One of those is that in order to induce more dollars to fund the federal deficit, interest rates will have to rise. The Fed can control the policy rate, but in order to keep long-term rates down the Committee may eventually be forced to start up their hose again – intervening to buy Treasuries in the market to prevent long rates from rising, and expanding the balance sheet. The market stabilizer here would be for interest rates to rise and induce more domestic savings; if for policy reasons the Fed doesn’t want that then they’ll have to add more money themselves, with inflationary consequences. (It’s inflationary either way, but if interest rates rise it’s only indirectly inflationary in that higher interest rates also increase money velocity).

The other implication is that the dollar would strengthen on foreign exchange markets, since if foreigners are going to invest in the US in financial markets (or with direct investment, building new plants and so forth) they will need dollars to do so and the trade deficit is no longer providing a surplus of those dollars. It’s likely also that, with fewer dollars being sent abroad, domestic stock and bond markets would struggle more than they have been. A stronger dollar would be disinflationary at the margin, helping to hold down core goods prices, but this effect is fairly small…especially in the broader context I’ve mentioned, which is that all fiat currencies right now are getting smashed versus real stuff.

These are the implications of the recent large changes in financial flows. There are potential offsets available. If the trade deficit declines and the federal budget deficit declines also, it diminishes upward pressure on interest rates since domestic savers do not have to be incentivized to provide as much of the dollars in deficit. You can infer this from the barrel illustrations as well: if the federal budget moves towards balance, it lessens the net change in the system.

And there had been some positive signs on that score. The tariff revenue has been large, and some of the spending priorities of the prior Administration have been de-emphasized. These are positive developments which could lessen the pressure on the dollar and interest rates…except that the Trump Administration has been mooting the idea of ‘tariff dividend checks,’ increased defense spending, buying Greenland, and other significant spending initiatives.

It is also possible, even probable, that the Fed or Congress could change banking liquidity regulations in such a way that banks are forced to hold more Treasuries, which would add an additional hose to the top of the barrel. However, the more assets that banks are required to hold, worsening the return on assets of traditional banks, the more banking functions will start to move to non-bank entities or into crypto, increasing the money supply while decreasing the Fed’s control of it.

The upshot of all of these changes is that – based on the flows as we see them now, which could change – I believe we are going to see a significantly steeper yield curve and a significantly stronger dollar over the next few years.

Having said all of that, let me circle back to the start of this note – while the USD is not likely to collapse against other currencies, the movement against commodities (not to mention equities) and other real assets is disturbing. The US money supply has been accelerating recently; M2 is only +4.6% in the last 12 months, but that’s near (or may even be above) the maximum rate that is sustainable without causing inflation in a country that is deglobalizing and in demographic reverse. I am not bullish on gold and silver at these levels, and am more cautious on commodities than I have been in a while. But while I am a dollar bull against other currencies, I am a bear of fiat currencies against real assets generally…and I am concerned that the recent waterfall-like behavior of fiat presages a re-acceleration of CPI-style inflation. Commodities feed broadly into prices, but so do wages and lots of other things that are measured in terms of dollars. If the problem is fiat, and not gold and silver themselves, then it’s a bullish signal for inflation.

[1] These images were generated using AI image generation tools to create an illustrative representation for explanatory purposes.

They’re Starting to Come Around on Rent Inflation

For a couple of years, I have been relentlessly defending my forward inflation forecasts against a sizeable group of people who looked at various high-frequency rent indicators and concluded that rents were going to be imminently in deflation. (For most of the last year many of those same people thought tariffs would be a large and immediate effect increasing inflation. Fortunately for them, being wrong on both counts, at least the errors offset somewhat.)

This battle began in early 2023, shortly after the publication of new indices by the Federal Reserve Bank of Cleveland, supported by a paper entitled “Disentangling Rent Index Differences: Data, Methods, and Scope” by Adams, Lowenstein, and Verbrugge. Those authors parsed the BLS rent microdata to separate out the new tenants, and created a “New Tenant Repeat Rent” (NTRR) Index that supposedly served as a leading indicator of what all rents were going to do. Naturally, NTRR had peaked early and was heading down sharply, which reinforced the observation from things like Zillow, Apartment list, etc that new rents in the aftermath of the post-eviction-moratorium catch-up were declining.[1]

The San Francisco Fed also published a piece in mid-2023, entitled “Where is Shelter Inflation Headed,” by Kmetz, Louis, and Mondragon. Don’t get me wrong, I love it when people try to create better models of inflation processes. But this was another one that made just terrible forecasts, because (as in the former case) it was put together by econometricians who didn’t understand the actual underlying process and thought they could just torture the truth out of the data. They included this wonderful (and subsequently damning, because the Internet remembers everything) chart.

Accompanying that chart was the helpful clarifying statement, in case you didn’t get the import: “Our baseline forecast suggests that year-over-year shelter inflation will continue to slow through late 2024 and may even turn negative by mid-2024.”

In case you were curious, it didn’t turn negative; in mid-2024 it was a bit above 5%.

So back then is when I had to start defending a fairly simple premise: the behavior of landlords when they offer rents to new renters does not necessarily mirror what they offer to renewing renters. In fact, I could be even more strident – landlords could not offer lower rents to everyone, even if they offered them to new renters. That’s because a landlord needs to cover his costs or he won’t be a landlord for long. And in 2023, the costs for a landlord were still rising very rapidly – labor, energy, insurance, taxes, maintenance, and so on. My model – first presented in Enduring Investments’ Quarterly Inflation Outlook in August 2023 – suggested that rents were going to decelerate, but much more slowly than others were forecasting. I had them as low as 3% by mid-2024 before flattening out, and even that turned out to be too aggressive on the disinflation side.

By now, regular readers are familiar with this model and familiar with the fact that it still is calling for Rent of Primary Residence to hang around the current 3% level for quite a while yet. Want ‘em lower? Lower landlord costs.

But this article isn’t meant (only) to pat myself on the back. I also want to recognize when someone gets it right and the great inflation analysts at Barclays recently published an article entitled “Apples and oranges in the CPI basket: Why market rent gauges mislead on shelter,” by Millar, Sriram, Giannoni, and Johanson. It is marvelous article, and you have access to Barclays Live and care about this topic you should read it. While they don’t build a cost-plus model like I did, they got to many of the core reasons why looking at new-renter indices is bound to be misleading. My favorite charts from the piece are below (I also had these in my recent CPI report).

What my model does is tell you why that had to be the case: landlords can’t just lower rents on their whole renter base if their costs are increasing. The only exception to that would be if there had been significant overbuilding such that there was a surplus of apartments over the demand from renters. In some places, especially those currently experiencing a negative immigration shock, that may be the case (although those places happen to also be the ones experiencing large increases in insurance costs, so it’s not quite that easy). But nationwide, there is not a surfeit of apartments for rent. Ergo, no rent deflation. And it’s going to stay that way for a while.

One final note here, about the recent Trump announcement that the Administration desires less institutional ownership of single family homes and apartments. I say ‘desires,’ even though that isn’t how it was phrased, since there appears to be no obvious way that the Administration can force this. They are reportedly looking into whether antitrust regulations can be used to keep institutions from accumulating very large portfolios of shelter units, but this looks like (at best) a task for the legislature, not the executive. But let’s consider quickly what the effect would be if Trump got his way in this regard.[2] Institutions which own homes and apartments don’t hold them off the market. That would be terrible carry. They rent them, just as landlords do. If you forced institutions to divest single-family homes, it would simply move supply from the rental market to the owned-home market. That would probably drive home prices a little lower, relative to the prior baseline, but increase rent growth at the margin. This doesn’t seem productive!

[1] I talked about NTRR in a July 2023 episode of my podcast: Ep.74: Inflation Folk Remedies

[2] Honestly, I don’t think he really means to do this. Some amount of what the President says – especially the impossible things – are intended for consumption by voters. I could be wrong on this. Mr. Trump does have a way of making things happen that didn’t seem possible initially, but in this case there’s probably not much he can do and anyway it wouldn’t have a big impact anyway.

Inflation Guy’s CPI Summary (December 2025)

Let’s start this month by remembering the absolute dumpster-fire that was last month’s CPI. The number for November was patently ridiculous on its face, and it took mere minutes to realize that the BLS was showing 2-month changes for what were essentially one-month changes:

“Because what it looks like is that for many series the BLS didn’t calculate a two-month change based on the current price level – it looks like, especially for housing, they assumed October’s change was zero so that the two-month change reported for this month was actually a one-month change spread over two months. For example, even with the low Owners’ Equivalent Rent print in September, the y/y figure was 3.76%, so about 0.31% per month. The BLS tells us that the two-month change in OER was +0.27%. That looks more than a little suspicious to me.”

That in fact was what had happened. The BLS has clearly spelled-out procedures for what happens when they cannot collect a price. If they can collect the price for other similar items, they impute the data for the uncollected price by ‘adjacent cell imputation.’ Happens all the time, and has happened more since there have been fewer data collectors, and that has upset a lot of people…but it’s no big deal. What happens less often is that the BLS can collect no similar price, or they don’t have a statistically-significant sample; in that case the BLS procedures call for the prior price to be carried forward and then the price gets naturally corrected the next time it can be gathered. I’ll talk more about this in a week or two, but if the item was generally rising in price that unchanged estimate for monthly price change will be a little low in the first month and a little high in the second month. If the item was generally getting cheaper, you’ll be a little high and then a little low when you catch up. But that’s better than taking a wild unscientific guess.

But normally, that happens for tiny categories. In this case, since no prices were collected, the BLS realized that its procedures called for carryforward pricing. After the data were released, they were very transparent about the fact that this caused understatement in the CPI, and that while most categories will be corrected by normal sampling in a month or two, the rent and OER samples will take about six months to correct because of the way those samples use overlapping six-month survey panels. You don’t need to worry about the fine details here, but to realize that the October number is missing, the November number is garbage, and the year/year numbers won’t be “right” for a while.

Ergo, take everything in today’s number, and all the charts, with a grain of salt.

A little side note is that the BLS was able to collect some data for November, when there was historical data available, so some of the series are complete. And some series have a dash (“-“) for November. Bloomberg simply omits October for those series. The practical consequence is that this is a massive mess for anyone who has built spreadsheets based on fairly normal assumptions about data structure! And it will be for a while. Anyway, on to today’s number.

Over the last month, inflation markets have been little changed.

They’re actually even more unchanged than that looks like, because the apparent rise in short-term inflation expectations is a quirk of the fact that every day, the window covered by a 1-year swap rolls forward one day, and as it turns out the day that it loses on the front end is a day when the NSA CPI was declining sharply thanks to the garbage report we just mentioned. So, the new 1-year swap has less of that garbage dragging the y/y rate down, and so it rises slightly. The net result is that inflation expectations at the front end are not really rising.

The expectations for the December CPI were for +0.31% on the seasonally-adjusted headline, with +0.32% on Core. These are even more guessy guesses than normal, since economists had to figure which categories might jump back and by how much. The actual CPI came in at +0.307% (SA) on headline CPI, and +0.239% on Core CPI. We will ignore the y/y rates for now. If we take those numbers at face value, it would annualize to 2.9% on Core CPI and 3.75% on headline CPI. That doesn’t seem wildly off, with the obvious caveat that annualizing a one-month change is stupid. Sorry.

Now, the Median CPI is going to be a snap-back sort of month. I think. The median category appears to me to be one of the regional OERs, so the actual number will depend on the seasonal adjustment the Cleveland Fed applies to that subindex. And I don’t know what the Cleveland Fed did for their last data point so they may be jumping off differently than I did. But any way you slice it, we’re going to be around 0.30-0.35% for median.

This is right about where the trend was prior to September. A word on September: while it is convenient to think that September was the ‘last good data point’ we had before the shutdown, remember that month had an outlier Owners’ Equivalent Rent number (0.14%, vs a series of 0.28%-0.40% that happened in the year prior to that) that we expected to rebound in the next month. We never saw the rebound. Median CPI was also affected by that, and so the last truly normal number was August. The upshot of it is that there may be some continued deceleration in median CPI, but it isn’t clear at all.

Core goods as of this month were +1.42% y/y. They look to be leveling off a bit, and it may be that the bump from tariffs (which, contrary to economic theory but in keeping with the way it really works, got bled into prices over a period of time rather than all at once) is petering out. Too early to tell, and part of this leveling out is due to soft Used Cars data in this month’s release. Core Services, mostly housing, continues to decelerate but see all of the caveats about rents.

And yes, rents went back to doing what they had been doing. Primary Rents were +0.26% m/m, and Owners’ Equivalent Rent was +0.31% m/m. So, yeah: that dip in OER in September was a mirage, and we’re still running at 3-4% in rents although the one-month BLS blip makes it appear that we’re still decelerating. I am not sure that’s really true.

Speaking of rents, Barclays put out a great piece earlier this week. It’s called “Apples and oranges in the CPI basket: Why market rent gauges mislead on shelter,” and if you have access to it you should read it. If you do not have access to it, you can just read my articles from the last few years. Seriously, though – it’s a very good piece and I’ll talk about it more in a week or so. But here are two of my favorite exhibits from their writeup.

Since 90% or so of rents are continuing rents, and all of the high-frequency rent indicators are recording new rents…can you see why there’s a problem?

That’s why a few years ago I migrated my model for rents to be based on a bottom-up estimate of what landlord costs were doing. Here is that model with the updated Primary Rents.

Normally, the Enduring Model has more lead time, but since part of it relies on PPI data that haven’t been released since September (and which is coming out tomorrow), the look forward is shorter than normal. Still, it says the same thing I’m saying above and approximately what Barclays is now saying – 3% on rents is about where it should be. It is not likely to decline sharply from here. And that means that getting CPI to 2% is going to depend on a collapse in goods prices or core services ex-rents, neither of which I see happening soon.

Although I should point out that core services ex-rents, aka Supercore, has been looking better of late.

As with everything else, we need to wait and see how this evolves once we get a few more months of decent data. I expect core services ex-rents to continue to decelerate a little, but that’s mainly because of Health Insurance (which fell -1.1% last month, and because of the way the Health Insurance estimate changes only once per year and gets smeared over 12 months this should work out to a drag of about 1bp/month on Core CPI). Outside of Health Insurance, the downward pressure on core services ex-rents is lessening.

And really, that’s the summary of the number: some of the effects from bad stuff (e.g. tariffs, which were never as big a deal as people treated them) are wearing off but some of the positive trends (e.g. the deceleration in rents) have also mostly run their course. The Enduring Investments Inflation Diffusion Index shows that there’s a bit of an upward trend in the distribution of accelerations/decelerations.

All of which points to the same thing I’ve been saying for a while, and that’s that once the spike was over we knew inflation would drop but it was likely to settle in the high 3s/low 4s (since amended to mid-to-high 3s). The tailwinds on inflation have turned into headwinds, so monetary policy overall needs to be tighter than it otherwise would be. The Fed doesn’t see it that way yet, and new additions to the Board of Governors are definitely more likely to be dovish than hawkish. Not only that, the federal government is also adding liquidity…or will be, if the President convinces Fannie Mae and Freddie Mac to buy $200bln in mortgages. A Federal Reserve which appreciated the inflation risks would be preparing to drain away that liquidity, no matter what it was going to do on interest rates. There’s no sign of that.

As a result: I think it’s reasonable to expect dovish outcomes from the Fed from here, although Chairman Powell will doubtless try to stick it in the eye of the President (and the American people get caught in the crossfire) before his term is up. That differs from the Fed of the last 30 years only in degree. They are going to be too loose, and there’s a good risk that inflation heads higher from here (not to 9%, mind you, but getting the sign right will matter).

Which Rates Are Converging?

In early 2020, global nominal interest rates converged around zero, with the US (at the 10-year maturity point) under 1% and the EU slightly negative. The monetary spigots were on, and central banks coordinated to squirt liquidity everywhere they could. Since that time, as monetary policy has diverged somewhat, nominal interest rates have diverged. Notably, Japanese rates remained lower than other developed country rates, but in general the picture spread out a bit.

What is interesting, though, is that this behavior of nominal rates obscures what is really happening ‘under the hood’ so to speak. Recall that nominal rates are (approximately) the sum of real rates – the cost of money – and compensation for expected inflation. Thanks to the CPI swaps market and/or the inflation-indexed bond market, we can break nominal rates into these two components. The evolution of those two components tells very different stories depending on the country or region. For the purposes of this article, I’m considering the US, EU, Japan, and the UK. Obviously the UK is the smallest economic unit there but they have the oldest inflation-linked bond market so they’re a crowd favorite.

In 2020, the UK had the highest implied inflation of this set, and the lowest real rates. In the UK, long-term real rates have been persistently very much lower than in the rest of the developed world, mainly because pension fund demand caused long-term linkers to be outrageously expensive.[1] On the other end of the curve, investors in Japanese inflation have persistently priced near-deflation so that in 2020 Japan had the lowest implied inflation and the highest real rates. So, even though Japan and the UK had very similar 10-year nominal rates, the composition of those real rates was wildly different. Note that in the second chart below, I am representing real rates as the spread between LIBOR/SOFR rates and the CPI swap rates, rather than looking at the inflation bond yields.[2]

Collectively, what these charts say is that inflation expectations across many disparate economies are converging, and right now that convergence looks like it’s headed to roughly where the US is at 2.5% (adjusting for differences in index composition). On the other hand, the cost of money is not noticeably converging, although real rates are gradually rising across many economies. Real interest rates are supposed to roughly reflect equilibrium economic growth, so the picture seems to be of gradually strengthening long-term equilibrium growth expectations across the US, EU, Japan, and UK, with the US having the strongest expected growth and Japan the weakest. Notably, the UK real rate has moved above the EU’s rate, which seems to make sense to me given the hot mess Europe is right now.

I don’t think this has any hot money trading implications. But I do think it’s useful to understand that while nominal rates remain different across economies, that’s becoming more and more due to differences in real rates and less and less due to differences in expected inflation rates. Of course, you can also see that the average cost of money globally is rising. Eventually, that could cause issues for other asset classes.

[1] Naturally, there are also some differences in the inflation definitions from one country to the next, and differences in what index is used for inflation swaps, which can account for some of these differences and explain why they never will, nor should, fully converge. I am abstracting from these differences; just look at the overall trend rather than try to read too much into the absolute differences, which may have good economic reasons.

[2] One reason I am doing so is that the JGBi bonds, unlike the inflation bonds in the US, UK, and Europe, do not have a deflation floor so that when inflation is very low, the real yields on those bonds naturally diverge because of the value of the embedded deflation floor. Which isn’t what we’re trying to look at. [ADDENDUM – A reader pointed out that I am very old. What I call the “new JGBis” do in fact have the deflation floor. The “new ones” have been issued since…2013. So this turns out to not be a very good reason supporting the way I’m doing this. Man, time flies.]